You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Extrajudicial Settlement of Estate With Special Power of Attorney To Sell or To Enter Into Develpoment Agreement-1Document5 pagesExtrajudicial Settlement of Estate With Special Power of Attorney To Sell or To Enter Into Develpoment Agreement-1Lucille Teves78% (23)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- CEC Catalogue FinalDocument40 pagesCEC Catalogue FinalRahul MandeliaNo ratings yet

- INTERNET STANDARDSDocument18 pagesINTERNET STANDARDSDawn HaneyNo ratings yet

- PN 19B Late Fee WaiverDocument2 pagesPN 19B Late Fee WaiverRahul MandeliaNo ratings yet

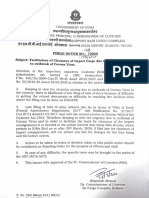

- Public Notice 7 of 2020Document2 pagesPublic Notice 7 of 2020Rahul MandeliaNo ratings yet

- Is.3459.2004 0 PDFDocument12 pagesIs.3459.2004 0 PDFRahul MandeliaNo ratings yet

- Catalogue Exact ToolDocument11 pagesCatalogue Exact ToolRahul MandeliaNo ratings yet

- Sawing Productivity June2017Document24 pagesSawing Productivity June2017Rahul Mandelia100% (1)

- INTERNET STANDARDSDocument18 pagesINTERNET STANDARDSDawn HaneyNo ratings yet

- Technopak E-Tailing Outlook 2014-Final PDFDocument28 pagesTechnopak E-Tailing Outlook 2014-Final PDFRahul MandeliaNo ratings yet

- Special Bandsaw Blade Jointing Kit: R%t.'iiDocument1 pageSpecial Bandsaw Blade Jointing Kit: R%t.'iiRahul MandeliaNo ratings yet

- Excise MFGDocument1 pageExcise MFGRahul MandeliaNo ratings yet

- Angelo RomaniDocument1 pageAngelo RomaniRahul MandeliaNo ratings yet

- Tissue-Paper IndustryDocument2 pagesTissue-Paper IndustryRahul Mandelia100% (1)

- Principles of Shear SlittingDocument26 pagesPrinciples of Shear SlittingMaureen Baird100% (1)

- Hakansson New BroucherDocument15 pagesHakansson New BroucherRahul MandeliaNo ratings yet

- Principles of Shear SlittingDocument26 pagesPrinciples of Shear SlittingMaureen Baird100% (1)

- Tokyo Diamond CatalogueDocument8 pagesTokyo Diamond CatalogueRahul MandeliaNo ratings yet

- Accumax Product CatlogDocument4 pagesAccumax Product CatlogRahul MandeliaNo ratings yet

- Apex Shears - Metal Cutting Circular SawsDocument2 pagesApex Shears - Metal Cutting Circular SawsRahul MandeliaNo ratings yet

- Hakansson New BroucherDocument15 pagesHakansson New BroucherRahul MandeliaNo ratings yet

- Tokyo Diamond CatalogueDocument8 pagesTokyo Diamond CatalogueRahul MandeliaNo ratings yet

- Diamond Saw CatlogDocument4 pagesDiamond Saw CatlogRahul MandeliaNo ratings yet

- Technology S-Curve (Tyres)Document1 pageTechnology S-Curve (Tyres)Rahul MandeliaNo ratings yet

- Ramos ReportDocument9 pagesRamos ReportOnaysha YuNo ratings yet

- Green HolidaysDocument5 pagesGreen HolidaysLenapsNo ratings yet

- Chapter 21 AppDocument2 pagesChapter 21 AppMaria TeresaNo ratings yet

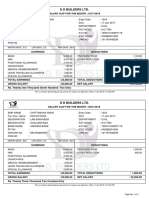

- Pay - Slip Oct. & Nov. 19Document1 pagePay - Slip Oct. & Nov. 19Atul Kumar MishraNo ratings yet

- The End of Japanese-Style ManagementDocument24 pagesThe End of Japanese-Style ManagementThanh Tung NguyenNo ratings yet

- Cbo Score of The Aca - FinalDocument364 pagesCbo Score of The Aca - FinalruttegurNo ratings yet

- Managing DifferencesDocument15 pagesManaging DifferencesAnonymous mAB7MfNo ratings yet

- Common Rationality CentipedeDocument4 pagesCommon Rationality Centipedesyzyx2003No ratings yet

- Forecasting PDFDocument87 pagesForecasting PDFSimple SoulNo ratings yet

- Business Model Analysis of Wal Mart and SearsDocument3 pagesBusiness Model Analysis of Wal Mart and SearsAndres IbonNo ratings yet

- Legal NoticeDocument7 pagesLegal NoticeRishyak BanavaraNo ratings yet

- Reference BikashDocument15 pagesReference Bikashroman0% (1)

- Indian Railways Project ReportDocument27 pagesIndian Railways Project Reportvabsy4533% (3)

- PresentationDocument21 pagesPresentationFaisal MahamudNo ratings yet

- Farmers, Miners and The State in Colonial Zimbabwe (Southern Rhodesia), c.1895-1961Document230 pagesFarmers, Miners and The State in Colonial Zimbabwe (Southern Rhodesia), c.1895-1961Peter MukunzaNo ratings yet

- CV Medi Aprianda S, S.TDocument2 pagesCV Medi Aprianda S, S.TMedi Aprianda SiregarNo ratings yet

- Risk Assessment For Grinding Work: Classic Builders and DevelopersDocument3 pagesRisk Assessment For Grinding Work: Classic Builders and DevelopersradeepNo ratings yet

- Trust Receipt Law NotesDocument8 pagesTrust Receipt Law NotesValentine MoralesNo ratings yet

- Market Structure and Game Theory (Part 4)Document7 pagesMarket Structure and Game Theory (Part 4)Srijita GhoshNo ratings yet

- MBA IInd SEM POM Chapter 08 Capacity Planning and Facilities LocationDocument52 pagesMBA IInd SEM POM Chapter 08 Capacity Planning and Facilities LocationPravie100% (2)

- Informative FinalDocument7 pagesInformative FinalJefry GhazalehNo ratings yet

- Placements IIM ADocument8 pagesPlacements IIM Abhanu1991No ratings yet

- Using Operations To Create Value Nama: Muhamad Syaeful Anwar NIM: 432910Document1 pageUsing Operations To Create Value Nama: Muhamad Syaeful Anwar NIM: 432910MuhamadSyaefulAnwarNo ratings yet

- Transfer by Trustees To Beneficiary: Form No. 4Document1 pageTransfer by Trustees To Beneficiary: Form No. 4Sudeep SharmaNo ratings yet

- Coal Bottom Ash As Sand Replacement in ConcreteDocument9 pagesCoal Bottom Ash As Sand Replacement in ConcretexxqNo ratings yet

- Seminar Paper11111Document22 pagesSeminar Paper11111Mulugeta88% (8)

- (Sample) Circular Flow of Incom & ExpenditureDocument12 pages(Sample) Circular Flow of Incom & ExpenditureDiveshDuttNo ratings yet

- Chapter 1Document16 pagesChapter 1abhishek9763No ratings yet

- EdpDocument163 pagesEdpCelina SomaNo ratings yet