You might also like

- Power Markets and Economics: Energy Costs, Trading, EmissionsFrom EverandPower Markets and Economics: Energy Costs, Trading, EmissionsNo ratings yet

- .+Energy+and+Other+gross+profit AfterDocument41 pages.+Energy+and+Other+gross+profit AfterAkash ChauhanNo ratings yet

- Taxation and Tax Policies in the Middle East: Butterworths Studies in International Political EconomyFrom EverandTaxation and Tax Policies in the Middle East: Butterworths Studies in International Political EconomyRating: 5 out of 5 stars5/5 (1)

- 6.+Energy+and+Other+revenue BeforeDocument37 pages6.+Energy+and+Other+revenue BeforeThe SturdyTubersNo ratings yet

- 2.+average+of+price+models BeforeDocument23 pages2.+average+of+price+models BeforeMuskan AroraNo ratings yet

- 6.+Energy+and+Other+Revenue AfterDocument37 pages6.+Energy+and+Other+Revenue AftervictoriaNo ratings yet

- 8.+opex BeforeDocument45 pages8.+opex BeforeThe SturdyTubersNo ratings yet

- CAGRDocument7 pagesCAGRAsis NayakNo ratings yet

- TVS Motors Live Project Final 2Document39 pagesTVS Motors Live Project Final 2ritususmitakarNo ratings yet

- Performance of Infosys For The Third Quarter Ended December 31Document33 pagesPerformance of Infosys For The Third Quarter Ended December 31ubmba06No ratings yet

- Hero-MotoCorp - Annual ReportDocument40 pagesHero-MotoCorp - Annual ReportAdarsh DhakaNo ratings yet

- Sun Pharma's financial performance analysisDocument6 pagesSun Pharma's financial performance analysisBerkshire Hathway coldNo ratings yet

- Tesla Company AnalysisDocument83 pagesTesla Company AnalysisStevenTsaiNo ratings yet

- Glenmark Life Sciences Limited (GLS) : Q2-FY22 Result UpdateDocument9 pagesGlenmark Life Sciences Limited (GLS) : Q2-FY22 Result UpdateAkatsuki DNo ratings yet

- Hgs Q4 & Full Year Fy2018 Financials & Fact Sheet: Hinduja Global Solutions LimitedDocument6 pagesHgs Q4 & Full Year Fy2018 Financials & Fact Sheet: Hinduja Global Solutions LimitedChirag LaxmanNo ratings yet

- KPIs Bharti Airtel 04022020Document13 pagesKPIs Bharti Airtel 04022020laksikaNo ratings yet

- Gone Rural Historical Financials Reveal Growth Over TimeDocument31 pagesGone Rural Historical Financials Reveal Growth Over TimeHumphrey OsaigbeNo ratings yet

- Tesla FinModelDocument58 pagesTesla FinModelPrabhdeep DadyalNo ratings yet

- SGR Calculation Taking Base FY 2019Document38 pagesSGR Calculation Taking Base FY 2019Arif.hossen 30No ratings yet

- Reliance Press Release-JuneDocument9 pagesReliance Press Release-Junenakarani39No ratings yet

- Q4FY20 Earning UpdateDocument28 pagesQ4FY20 Earning UpdateSumit SharmaNo ratings yet

- Phiroze Jeejeebhoy Towers Dalal Street Mumbai - 400 001.: BSE Limited National Stock Exchange of India LimitedDocument6 pagesPhiroze Jeejeebhoy Towers Dalal Street Mumbai - 400 001.: BSE Limited National Stock Exchange of India LimitedJITHIN KRISHNAN MNo ratings yet

- DCF 2 CompletedDocument4 pagesDCF 2 CompletedPragathi T NNo ratings yet

- Mett International Pty LTD Financial Forecast 3 Year SummaryDocument134 pagesMett International Pty LTD Financial Forecast 3 Year SummaryJamilexNo ratings yet

- Total Revenue: Income StatementDocument4 pagesTotal Revenue: Income Statementmonica asifNo ratings yet

- Bajaj Auto Project TestDocument61 pagesBajaj Auto Project TestSauhard Sachan0% (1)

- Annual Report 2015 EN 2 PDFDocument132 pagesAnnual Report 2015 EN 2 PDFQusai BassamNo ratings yet

- Quarterly Report on Financial Results and OperationsDocument21 pagesQuarterly Report on Financial Results and OperationsSuresh KumarNo ratings yet

- Financial PerformanceDocument16 pagesFinancial PerformanceADEEL SAITHNo ratings yet

- (A) Nature of Business of Cepatwawasan Group BerhadDocument16 pages(A) Nature of Business of Cepatwawasan Group BerhadTan Rou YingNo ratings yet

- AQ - 20230226212627 - Aquila SA EN Consolidated Financial Results Preliminary 2022Document6 pagesAQ - 20230226212627 - Aquila SA EN Consolidated Financial Results Preliminary 2022teoxysNo ratings yet

- IRCON International 2QFY20 Result Review 14-11-19Document7 pagesIRCON International 2QFY20 Result Review 14-11-19Santosh HiredesaiNo ratings yet

- SGR Calculation Taking Base FY 2019Document17 pagesSGR Calculation Taking Base FY 2019Arif.hossen 30No ratings yet

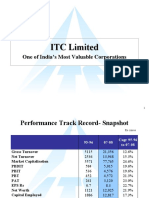

- ITC LimitedDocument46 pagesITC Limitedsarvani4frensNo ratings yet

- $tsla: RevenueDocument15 pages$tsla: RevenuePrabhdeep DadyalNo ratings yet

- Result Update Presentation - Q2 FY18: NOVEMBER 09, 2017Document11 pagesResult Update Presentation - Q2 FY18: NOVEMBER 09, 2017Mohit PariharNo ratings yet

- Almarai's Quality and GrowthDocument128 pagesAlmarai's Quality and GrowthHassen AbidiNo ratings yet

- Generali YE20 Supplementary Financial InformationDocument31 pagesGenerali YE20 Supplementary Financial InformationMislav GudeljNo ratings yet

- Financial (Rs Million) Mar-19 Mar-18 Mar-17 Mar-16 Mar-15 Y-O-Y Change (%) Y-O-Y Change (%)Document17 pagesFinancial (Rs Million) Mar-19 Mar-18 Mar-17 Mar-16 Mar-15 Y-O-Y Change (%) Y-O-Y Change (%)Berkshire Hathway coldNo ratings yet

- Earnings Update: InterGlobe Aviation Reports Q3 FY22 ResultsDocument14 pagesEarnings Update: InterGlobe Aviation Reports Q3 FY22 ResultsyousraNo ratings yet

- Brief About The Co Brands Competitive Positioning of The Co / Advantages Tracking Points Financials Incl Shareholding Pattern Valuation Rational SwotDocument42 pagesBrief About The Co Brands Competitive Positioning of The Co / Advantages Tracking Points Financials Incl Shareholding Pattern Valuation Rational SwotMitesh PatilNo ratings yet

- Analyst Presentation (Mar 10)Document32 pagesAnalyst Presentation (Mar 10)agarwalomNo ratings yet

- Tesla Income Statement and Financial Ratios 2016Document5 pagesTesla Income Statement and Financial Ratios 2016Mary JoyNo ratings yet

- Itc Limited: One of India'S Most Valuable CorporationsDocument50 pagesItc Limited: One of India'S Most Valuable CorporationsManas DasNo ratings yet

- Coca-Cola and Best Buy Income Statements and Financial ProjectionsDocument9 pagesCoca-Cola and Best Buy Income Statements and Financial ProjectionsEvelDerizkyNo ratings yet

- Symphony - DCF Valuation - Group6Document17 pagesSymphony - DCF Valuation - Group6Faheem ShanavasNo ratings yet

- GMR Financial Overview-Q2 FY11Document44 pagesGMR Financial Overview-Q2 FY11anilgupta_1No ratings yet

- Solution - Eicher Motors LTDDocument28 pagesSolution - Eicher Motors LTDvasudevNo ratings yet

- ACC EPS and Valuation ReportDocument25 pagesACC EPS and Valuation ReportprathamNo ratings yet

- TVS Motor Company: CMP: INR549 TP: INR548Document12 pagesTVS Motor Company: CMP: INR549 TP: INR548anujonwebNo ratings yet

- Pidilite Industries Income StatementDocument4 pagesPidilite Industries Income StatementRehan TyagiNo ratings yet

- BHEL Valuation of CompanyDocument23 pagesBHEL Valuation of CompanyVishalNo ratings yet

- Financial Ratios of Home Depot and Lowe'sDocument30 pagesFinancial Ratios of Home Depot and Lowe'sM UmarNo ratings yet

- EVA ExampleDocument27 pagesEVA Examplewelcome2jungleNo ratings yet

- PG - P&L: P&G Income StatementDocument3 pagesPG - P&L: P&G Income StatementMi TvNo ratings yet

- Tata MotorsDocument5 pagesTata Motorsinsurana73No ratings yet

- Particulars (INR in Crores) FY2015A FY2016A FY2017A FY2018ADocument6 pagesParticulars (INR in Crores) FY2015A FY2016A FY2017A FY2018AHamzah HakeemNo ratings yet

- Cocoaland Holdings 2Q19 resultsDocument14 pagesCocoaland Holdings 2Q19 resultsSajeetha MadhavanNo ratings yet

- Financial (Rs Million) Mar-19 Mar-18 Mar-17 Mar-16 Mar-15 Y-O-Y Change (%) Y-O-Y Change (%)Document1 pageFinancial (Rs Million) Mar-19 Mar-18 Mar-17 Mar-16 Mar-15 Y-O-Y Change (%) Y-O-Y Change (%)tarun lahotiNo ratings yet

- 1.summary Financial Analysis EILDocument9 pages1.summary Financial Analysis EILrahulNo ratings yet

- Functions & Formulae: Consci Consultnacy PVT LTDDocument11 pagesFunctions & Formulae: Consci Consultnacy PVT LTDDeepak ShuklaNo ratings yet

- Mahabharata RetoldDocument431 pagesMahabharata RetoldKetki PuranikNo ratings yet

- HTML Cheat Sheet GuideDocument1 pageHTML Cheat Sheet GuidePavan GvsNo ratings yet

- Micro Finance Industry in IndiaDocument5 pagesMicro Finance Industry in IndiaKetki PuranikNo ratings yet

- Drucker's Legacy for Future ManagementDocument4 pagesDrucker's Legacy for Future ManagementKetki PuranikNo ratings yet

- Colors and CommDocument30 pagesColors and CommKetki PuranikNo ratings yet

- Performance Appraisals 684Document14 pagesPerformance Appraisals 684mbahr01100% (2)

- Induction MatrixDocument47 pagesInduction MatrixKetki PuranikNo ratings yet

- The Hound of BaskervillesDocument67 pagesThe Hound of BaskervillesKetki PuranikNo ratings yet

- Dharamtar InfrastructureDocument7 pagesDharamtar InfrastructuresawshivNo ratings yet

- The Vario: Master of all tradesDocument44 pagesThe Vario: Master of all tradesJerry_TiberlakeNo ratings yet

- Assessement of Perception Reaction Parameters On Akure Owo Highway in Ondo State NigeriaDocument21 pagesAssessement of Perception Reaction Parameters On Akure Owo Highway in Ondo State NigeriaAliu AdekunleNo ratings yet

- E 410Document9 pagesE 410rahatNo ratings yet

- H-100 Ebrochure 2011Document8 pagesH-100 Ebrochure 2011AliAlFodehNo ratings yet

- GSPL - Company Profile @bangalore Office-1Document7 pagesGSPL - Company Profile @bangalore Office-1Eagle BangaloreNo ratings yet

- Ielts Writing Task 1 Maps & ProcessDocument42 pagesIelts Writing Task 1 Maps & ProcessLinh KhánhNo ratings yet

- MCHW Vol 1 1000 - Web PDFDocument51 pagesMCHW Vol 1 1000 - Web PDFalejandraoy9No ratings yet

- Presented By:-: Shoaib Ahmad Khan Sanjay Patel Shipra Asthana Parmesh BarethDocument19 pagesPresented By:-: Shoaib Ahmad Khan Sanjay Patel Shipra Asthana Parmesh BarethNilabjo Kanti PaulNo ratings yet

- Big CreekDocument106 pagesBig CreekRewati RamanNo ratings yet

- Perception Toward Tata Nano QuestionnaireDocument4 pagesPerception Toward Tata Nano Questionnairemdmust123No ratings yet

- Transaction history for toll accountDocument2 pagesTransaction history for toll accountRussellGreenleeNo ratings yet

- Elpm2 5hptengDocument6 pagesElpm2 5hptengNaren BhandarkarNo ratings yet

- CV of Alfredo Jr. Arios Claro 7 June 2017rcyDocument20 pagesCV of Alfredo Jr. Arios Claro 7 June 2017rcyalfredoNo ratings yet

- Transmission Stall Testing Procedure ExplainedDocument3 pagesTransmission Stall Testing Procedure Explainednamduong368No ratings yet

- (H) HornDocument4 pages(H) HornJosé Miguel GonzálezNo ratings yet

- Driver Drowsiness Detection With Audio-Visual WarningDocument7 pagesDriver Drowsiness Detection With Audio-Visual WarningIJIRSTNo ratings yet

- Advertisement For Shortlisting 21 Nov 2021.doc 2113Document8 pagesAdvertisement For Shortlisting 21 Nov 2021.doc 2113cainNo ratings yet

- Massey Ferguson 4370Document4 pagesMassey Ferguson 4370Breyner CortesNo ratings yet

- Safety Assists Technologies ExplainedDocument10 pagesSafety Assists Technologies ExplainedLorenz BanadaNo ratings yet

- Learner's Driving Permit in The U.S.Document3 pagesLearner's Driving Permit in The U.S.Bergen County Top Driving SchoolNo ratings yet

- 854 Iahe WW MJB Gad 001 R2 594X2000Document1 page854 Iahe WW MJB Gad 001 R2 594X2000KA25 ConsultantNo ratings yet

- LiDAR Classification and PLS-CADD Feature CodesDocument1 pageLiDAR Classification and PLS-CADD Feature CodesZdravko VidakovicNo ratings yet

- Maserati Granturismo MCDocument52 pagesMaserati Granturismo MCmazworkNo ratings yet

- 2 Components of The Transportation SystemDocument41 pages2 Components of The Transportation SystemJoshua Melegrito PeraltaNo ratings yet

- Bridge 1Document3 pagesBridge 1binanceNo ratings yet

- Pat303 Highway and Traffic Technology Laboratory WorksheetDocument14 pagesPat303 Highway and Traffic Technology Laboratory WorksheetDickson LingNo ratings yet

- Big Bend Ranch Biking Guide PDFDocument68 pagesBig Bend Ranch Biking Guide PDFacrobinsonNo ratings yet

- Responsive Document - CREW: National Park Service: Regarding Efforts by Wall Street Investors To Influence Agency Regulations: 7/25/2011 - FY 2011 Marked For Web RedactedDocument52 pagesResponsive Document - CREW: National Park Service: Regarding Efforts by Wall Street Investors To Influence Agency Regulations: 7/25/2011 - FY 2011 Marked For Web RedactedCREWNo ratings yet

- Interchange Best Practice Guide QRGDocument42 pagesInterchange Best Practice Guide QRGGordon LeeNo ratings yet