You might also like

- Fertilizer Sector: FFC Result PreviewDocument1 pageFertilizer Sector: FFC Result PreviewMuhammad Sarfraz AbbasiNo ratings yet

- Fertilizer Sector: FFBL Result PreviewDocument1 pageFertilizer Sector: FFBL Result PreviewMuhammad Sarfraz AbbasiNo ratings yet

- Cement Sector: Dispatches Slow Down ContinuesDocument1 pageCement Sector: Dispatches Slow Down ContinuesMuhammad Sarfraz AbbasiNo ratings yet

- Fertilizer Sector: FFBL Result PreviewDocument1 pageFertilizer Sector: FFBL Result PreviewMuhammad Sarfraz AbbasiNo ratings yet

- Fertilizer Sector: FFBL - A Good BUYDocument1 pageFertilizer Sector: FFBL - A Good BUYMuhammad Sarfraz AbbasiNo ratings yet

- Cement Sector: ACPL Result PreviewDocument1 pageCement Sector: ACPL Result PreviewMuhammad Sarfraz AbbasiNo ratings yet

- 08 Dec 2010Document1 page08 Dec 2010Muhammad Sarfraz AbbasiNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Lack of Modern Technology in Agriculture System in PakistanDocument4 pagesLack of Modern Technology in Agriculture System in PakistanBahiNo ratings yet

- BBG LEED EBOM-PresentationDocument27 pagesBBG LEED EBOM-PresentationJosephNo ratings yet

- Unit 1. Fundamentals of Managerial Economics (Chapter 1)Document50 pagesUnit 1. Fundamentals of Managerial Economics (Chapter 1)Felimar CalaNo ratings yet

- The Political Economy of Communication (Second Edition)Document2 pagesThe Political Economy of Communication (Second Edition)Trop JeengNo ratings yet

- Impact of The Construction Waste On The Cost of The Project: Sawant Surendra B., Hedaoo Manoj, Kumthekar MadhavDocument3 pagesImpact of The Construction Waste On The Cost of The Project: Sawant Surendra B., Hedaoo Manoj, Kumthekar MadhavJay ar TenorioNo ratings yet

- SBI Clerk Prelims Previous Year Paper 2018Document14 pagesSBI Clerk Prelims Previous Year Paper 2018Caroline JuliyatNo ratings yet

- New Smart Samriddhi Brochure 09.03.2021Document12 pagesNew Smart Samriddhi Brochure 09.03.2021GAJALAKSHMI LNo ratings yet

- MBBS MO OptionsDocument46 pagesMBBS MO Optionskrishna madkeNo ratings yet

- Participatory Governance - ReportDocument12 pagesParticipatory Governance - ReportAslamKhayerNo ratings yet

- ChartsDocument4 pagesChartsMyriam GGoNo ratings yet

- Partnership Dissolution Lecture NotesDocument7 pagesPartnership Dissolution Lecture NotesGene Marie PotencianoNo ratings yet

- A Comparative Evaluation Between National and International Trade and Explain The Concept of Geographical Indication and ItDocument15 pagesA Comparative Evaluation Between National and International Trade and Explain The Concept of Geographical Indication and ItPhalguni Mutha100% (1)

- Dornbusch Overshooting ModelDocument17 pagesDornbusch Overshooting Modelka2010cheungNo ratings yet

- Anand Vihar Railway Stn. RedevelopementDocument14 pagesAnand Vihar Railway Stn. RedevelopementPratyush Daju0% (1)

- 15dec2022102121 ShipperDocument1 page15dec2022102121 ShipperDISPATCH GROUPNo ratings yet

- Chapter 6Document32 pagesChapter 6John Rick DayondonNo ratings yet

- Installment Sales - PretestDocument2 pagesInstallment Sales - PretestCattleyaNo ratings yet

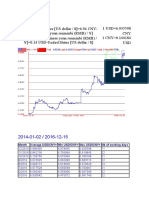

- Month Average USD/CNY Min USD/CNY Max USD/CNY NB of Working DaysDocument3 pagesMonth Average USD/CNY Min USD/CNY Max USD/CNY NB of Working DaysZahid RizvyNo ratings yet

- Fdi Inflows Into India and Their Impact On Select Economic Variables Using Multiple Regression ModelDocument15 pagesFdi Inflows Into India and Their Impact On Select Economic Variables Using Multiple Regression ModelAnonymous CwJeBCAXpNo ratings yet

- Pye, D.-1968-The Nature and Art of WorkmanshipDocument22 pagesPye, D.-1968-The Nature and Art of WorkmanshipecoaletNo ratings yet

- DPWH Natl Sewerage Septage MGMT ProgramDocument15 pagesDPWH Natl Sewerage Septage MGMT Programclint castilloNo ratings yet

- Bill 1.1Document2 pagesBill 1.1Александр ТимофеевNo ratings yet

- (MP) Platinum Ex Factory Price ListDocument1 page(MP) Platinum Ex Factory Price ListSaurabh JainNo ratings yet

- TUT. 1 Regional Integration (Essay)Document2 pagesTUT. 1 Regional Integration (Essay)darren downerNo ratings yet

- E417Syllabus 19Document2 pagesE417Syllabus 19kashmiraNo ratings yet

- Position PaperDocument2 pagesPosition PaperMaria Marielle BucksNo ratings yet

- Veit Tunel 1Document7 pagesVeit Tunel 1Bladimir SolizNo ratings yet

- Apply Online Pradhan Mantri Awas Yojana (PMAY) Gramin (Application Form 2017) Using Pmaymis - Housing For All 2022 Scheme - PM Jan Dhan Yojana PDFDocument103 pagesApply Online Pradhan Mantri Awas Yojana (PMAY) Gramin (Application Form 2017) Using Pmaymis - Housing For All 2022 Scheme - PM Jan Dhan Yojana PDFAnonymous dxsNnL6S8h0% (1)

- 2 - Buss Plan - Farm - Mst19pagesDocument19 pages2 - Buss Plan - Farm - Mst19pagesRaihan RahmanNo ratings yet

- The United States Edition of Marketing Management, 14e. 1-1Document133 pagesThe United States Edition of Marketing Management, 14e. 1-1Tauhid Ahmed BappyNo ratings yet