You might also like

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- First Division (G.R. No. 163504, August 05, 2015)Document12 pagesFirst Division (G.R. No. 163504, August 05, 2015)JB AndesNo ratings yet

- People v. de LeonDocument3 pagesPeople v. de LeonLuis LopezNo ratings yet

- Website Planning Template ForDocument10 pagesWebsite Planning Template ForDeepak Veer100% (2)

- Sub TopicDocument1 pageSub TopicApril AcompaniadoNo ratings yet

- Singapore Post LTD.: Recurrent Service Failures: The Singapore Postal MarketDocument10 pagesSingapore Post LTD.: Recurrent Service Failures: The Singapore Postal MarketJishnu M RavindraNo ratings yet

- Studiu de Caz - Lean SCM TescoDocument2 pagesStudiu de Caz - Lean SCM TescoMircea-Nesu CiprianNo ratings yet

- CV Muhammad Imran Riaz 1 P A G e MobiSerDocument3 pagesCV Muhammad Imran Riaz 1 P A G e MobiSerAmna Khan YousafzaiNo ratings yet

- GDS Knowledge - InternDocument6 pagesGDS Knowledge - InternAbhishekNo ratings yet

- Mid Term Defense Updated SlidesDocument31 pagesMid Term Defense Updated SlidesRojash ShahiNo ratings yet

- Ogl 481 - Project Management Article - Ogl 320 Project Management Module 7 PaperDocument1 pageOgl 481 - Project Management Article - Ogl 320 Project Management Module 7 Paperapi-513938901No ratings yet

- Mobile Games and Academic Performance of University StudentsDocument7 pagesMobile Games and Academic Performance of University StudentsMarianita Jane P. BatinNo ratings yet

- Sample EssaDocument2 pagesSample Essakismat kunwarNo ratings yet

- Definition, Scope, and Purpose: Administrative LawDocument5 pagesDefinition, Scope, and Purpose: Administrative LawIanLightPajaroNo ratings yet

- Enem Enem Enem: Me Deu Um Beijo e Virou PoesiaDocument34 pagesEnem Enem Enem: Me Deu Um Beijo e Virou PoesiaMaristella GalvãoNo ratings yet

- Half Moon Bay State Beach Campground MapDocument2 pagesHalf Moon Bay State Beach Campground MapCalifornia State Parks100% (1)

- Century Labour Market Change Mar2003Document12 pagesCentury Labour Market Change Mar2003Fatim NiangNo ratings yet

- AckkkkkkkDocument10 pagesAckkkkkkkFarnaz BharwaniNo ratings yet

- U2 - Keith Haring Comprehension QuestionsDocument3 pagesU2 - Keith Haring Comprehension QuestionsSteve GOopNo ratings yet

- Pass Format From Police StationDocument1 pagePass Format From Police StationThe Indian Express83% (6)

- 908e03-Pdf-Eng Security BreachDocument12 pages908e03-Pdf-Eng Security Breachluis alfredo lachira coveñasNo ratings yet

- TimelineDocument2 pagesTimelinefranchesca latido100% (3)

- Detailed Lesson Plan in Science VDocument6 pagesDetailed Lesson Plan in Science VMae LleovitNo ratings yet

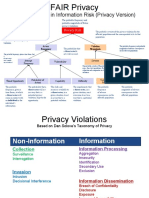

- Factor Analysis in Information Risk (Privacy Version)Document8 pagesFactor Analysis in Information Risk (Privacy Version)Otgonbayar TsengelNo ratings yet

- Village (NAME) Gram Panchayat (Name)Document135 pagesVillage (NAME) Gram Panchayat (Name)AmanNo ratings yet

- Edgar Payne - Composition of Outdoor Painting PDFDocument187 pagesEdgar Payne - Composition of Outdoor Painting PDFihavenoimagination92% (90)

- Translation Review What Is TranslationDocument5 pagesTranslation Review What Is TranslationJinNo ratings yet

- Corrective and Preventive Action - WikipediaDocument20 pagesCorrective and Preventive Action - WikipediaFkNo ratings yet

- IELTS Advantage Speaking and Listening SkillsDocument122 pagesIELTS Advantage Speaking and Listening SkillsAlba Lucía Corrales Reina100% (8)

- BATSA Press Release May1, 2020Document3 pagesBATSA Press Release May1, 2020CelesteLouwNo ratings yet

- John Hankinson AffidavitDocument16 pagesJohn Hankinson AffidavitRtrForumNo ratings yet