You might also like

- IRS f982 Goes With The 1099-CDocument5 pagesIRS f982 Goes With The 1099-Cexousiallc100% (3)

- Irs 2285 ManualDocument15 pagesIrs 2285 ManualMichael BarnesNo ratings yet

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- Taxation First Preboards Answer KeyDocument20 pagesTaxation First Preboards Answer KeyJerma Dela CruzNo ratings yet

- Sidhartha Bank TodayDocument3 pagesSidhartha Bank TodayGaurav MishraNo ratings yet

- Income Analysis WorksheetDocument11 pagesIncome Analysis WorksheetRajasekhar Reddy AnekalluNo ratings yet

- Tax Audit Checklist for Form 3CDDocument36 pagesTax Audit Checklist for Form 3CDKoolmindNo ratings yet

- 1040 Exam Prep: Module II - Basic Tax ConceptsFrom Everand1040 Exam Prep: Module II - Basic Tax ConceptsRating: 1.5 out of 5 stars1.5/5 (2)

- Fiverr Earning SheetDocument1 pageFiverr Earning SheetKagami TaigaNo ratings yet

- Customizing R/3 FI for VAT Processing in 3 StepsDocument8 pagesCustomizing R/3 FI for VAT Processing in 3 StepsJunling Xu100% (2)

- Invoice: Order No.: 52113272 Order Placed On: 02/01/2023Document1 pageInvoice: Order No.: 52113272 Order Placed On: 02/01/2023Alexandru BadanauNo ratings yet

- Tratamentul Total Al CanceruluiDocument71 pagesTratamentul Total Al CanceruluiAntal98% (98)

- Tratamentul Total Al CanceruluiDocument71 pagesTratamentul Total Al CanceruluiAntal98% (98)

- Tratamentul Total Al CanceruluiDocument71 pagesTratamentul Total Al CanceruluiAntal98% (98)

- Tratamentul Total Al CanceruluiDocument71 pagesTratamentul Total Al CanceruluiAntal98% (98)

- Tratamentul Total Al CanceruluiDocument71 pagesTratamentul Total Al CanceruluiAntal98% (98)

- Instructions For Form 2220: Underpayment of Estimated Tax by CorporationsDocument4 pagesInstructions For Form 2220: Underpayment of Estimated Tax by CorporationsIRSNo ratings yet

- Instructions For Form 2220: Underpayment of Estimated Tax by CorporationsDocument4 pagesInstructions For Form 2220: Underpayment of Estimated Tax by CorporationsIRSNo ratings yet

- US Internal Revenue Service: I2220 - 1992Document4 pagesUS Internal Revenue Service: I2220 - 1992IRSNo ratings yet

- US Internal Revenue Service: I2220 - 1996Document4 pagesUS Internal Revenue Service: I2220 - 1996IRSNo ratings yet

- US Internal Revenue Service: f8860 - 2000Document2 pagesUS Internal Revenue Service: f8860 - 2000IRSNo ratings yet

- (Updated July 2010) (2.2.1) Corporation Tax - General BackgroundDocument13 pages(Updated July 2010) (2.2.1) Corporation Tax - General BackgroundjfjkavanaghNo ratings yet

- US Internal Revenue Service: f8860 - 1999Document2 pagesUS Internal Revenue Service: f8860 - 1999IRSNo ratings yet

- US Internal Revenue Service: f8860 - 1998Document2 pagesUS Internal Revenue Service: f8860 - 1998IRSNo ratings yet

- US Internal Revenue Service: f2220 - 1999Document4 pagesUS Internal Revenue Service: f2220 - 1999IRSNo ratings yet

- US Internal Revenue Service: f2210f - 1996Document2 pagesUS Internal Revenue Service: f2210f - 1996IRSNo ratings yet

- US Internal Revenue Service: f2210 - 1996Document3 pagesUS Internal Revenue Service: f2210 - 1996IRSNo ratings yet

- t2sch31 22eDocument12 pagest2sch31 22eiimauditorNo ratings yet

- US Internal Revenue Service: f2210 - 1991Document2 pagesUS Internal Revenue Service: f2210 - 1991IRSNo ratings yet

- Interest Charge On DISC-Related Deferred Tax Liability: Sign HereDocument2 pagesInterest Charge On DISC-Related Deferred Tax Liability: Sign HereInternational Tax Magazine; David Greenberg PhD, MSA, EA, CPA; Tax Group International; 646-705-2910No ratings yet

- ITR AssignmentDocument8 pagesITR AssignmentEkta VermaNo ratings yet

- US Internal Revenue Service: f2210f - 1997Document2 pagesUS Internal Revenue Service: f2210f - 1997IRSNo ratings yet

- Release NotesDocument10 pagesRelease NotesSirc ElocinNo ratings yet

- US Internal Revenue Service: f6198 - 2000Document1 pageUS Internal Revenue Service: f6198 - 2000IRSNo ratings yet

- Instructions For Form 2210: Underpayment of Estimated Tax by Individuals, Estates, and TrustsDocument5 pagesInstructions For Form 2210: Underpayment of Estimated Tax by Individuals, Estates, and TrustsIRSNo ratings yet

- US Internal Revenue Service: f2210f - 1995Document2 pagesUS Internal Revenue Service: f2210f - 1995IRSNo ratings yet

- Instructions For Form 990-C: Farmers' Cooperative Association Income Tax ReturnDocument16 pagesInstructions For Form 990-C: Farmers' Cooperative Association Income Tax ReturnIRSNo ratings yet

- US Internal Revenue Service: I8801Document4 pagesUS Internal Revenue Service: I8801IRSNo ratings yet

- Guide For Preparation of Income Tax Return-ITR1 (SARAL-II) For AY 2010-11Document6 pagesGuide For Preparation of Income Tax Return-ITR1 (SARAL-II) For AY 2010-11amitbabuNo ratings yet

- US Internal Revenue Service: f2220 - 1996Document4 pagesUS Internal Revenue Service: f2220 - 1996IRSNo ratings yet

- US Internal Revenue Service: I1120sm3 - 2005Document18 pagesUS Internal Revenue Service: I1120sm3 - 2005IRSNo ratings yet

- US Internal Revenue Service: f6198 - 1999Document1 pageUS Internal Revenue Service: f6198 - 1999IRSNo ratings yet

- As 221Document24 pagesAs 221Bhaskar BalajiNo ratings yet

- f1040x PDFDocument2 pagesf1040x PDFAlexNo ratings yet

- F 5452Document4 pagesF 5452IRSNo ratings yet

- Chapter 4-Case 1 - CommencementDocument9 pagesChapter 4-Case 1 - CommencementgerlaniamelgacoNo ratings yet

- W4 TaxesDocument35 pagesW4 TaxesVanessa LeeNo ratings yet

- Tax Planning With Reference To New Business - NatureDocument26 pagesTax Planning With Reference To New Business - NatureasifanisNo ratings yet

- Amended U.S. Individual Income Tax Return: Use Part III On The Back To Explain Any ChangesDocument2 pagesAmended U.S. Individual Income Tax Return: Use Part III On The Back To Explain Any ChangesEri TakataNo ratings yet

- Shareholder's Instructions For Schedule K-1 (Form 1120S) : Pager/SgmlDocument8 pagesShareholder's Instructions For Schedule K-1 (Form 1120S) : Pager/SgmlIRSNo ratings yet

- Bir Form 1702Document16 pagesBir Form 1702Christine Ann GamboaNo ratings yet

- US Internal Revenue Service: f2210f - 1999Document2 pagesUS Internal Revenue Service: f2210f - 1999IRSNo ratings yet

- How To Calculate Loan AmountsDocument7 pagesHow To Calculate Loan AmountseramossotoNo ratings yet

- How To File Indian Income Tax Updated ReturnDocument6 pagesHow To File Indian Income Tax Updated ReturnpragativistaarNo ratings yet

- Chap 3 - Company TaxationDocument15 pagesChap 3 - Company Taxationhippop kNo ratings yet

- Instructions For Schedule M-3 (Form 1120S) : Pager/SgmlDocument16 pagesInstructions For Schedule M-3 (Form 1120S) : Pager/SgmlIRSNo ratings yet

- US Internal Revenue Service: I2210 - 1995Document5 pagesUS Internal Revenue Service: I2210 - 1995IRSNo ratings yet

- US Internal Revenue Service: f2210 - 1995Document3 pagesUS Internal Revenue Service: f2210 - 1995IRSNo ratings yet

- Deduction, Collection & Recovery of TaxesDocument143 pagesDeduction, Collection & Recovery of TaxesjyotiNo ratings yet

- Accounting For Taxes On IncomeDocument24 pagesAccounting For Taxes On IncomeDeepti SinghNo ratings yet

- Delloite CIT (A) PDFDocument7 pagesDelloite CIT (A) PDFshashi vermaNo ratings yet

- US Internal Revenue Service: f5884 - 1992Document2 pagesUS Internal Revenue Service: f5884 - 1992IRSNo ratings yet

- Explanatory Notes Formct1Document15 pagesExplanatory Notes Formct1lockon31No ratings yet

- Do You Have To File Form 2210?: Underpayment of Estimated Tax by Individuals, Estates, and TrustsDocument4 pagesDo You Have To File Form 2210?: Underpayment of Estimated Tax by Individuals, Estates, and TrustsZhen ZhangNo ratings yet

- Shareholder's Instructions For Schedule K-1 (Form 1120S) : Pager/SgmlDocument8 pagesShareholder's Instructions For Schedule K-1 (Form 1120S) : Pager/SgmlIRSNo ratings yet

- P 6 1. Business Laws PDFDocument70 pagesP 6 1. Business Laws PDFSruthi RekhaNo ratings yet

- Chapter 8 Tax AdministrationDocument14 pagesChapter 8 Tax AdministrationHazlina Hussein100% (1)

- Instructions For Form 2210: Underpayment of Estimated Tax by Individuals, Estates, and TrustsDocument6 pagesInstructions For Form 2210: Underpayment of Estimated Tax by Individuals, Estates, and TrustsIRSNo ratings yet

- Industrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisFrom EverandIndustrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisNo ratings yet

- 2008 Data DictionaryDocument260 pages2008 Data DictionaryIRSNo ratings yet

- US Internal Revenue Service: 2290rulesty2007v4 0Document6 pagesUS Internal Revenue Service: 2290rulesty2007v4 0IRSNo ratings yet

- 2008 Objectives Report To Congress v2Document153 pages2008 Objectives Report To Congress v2IRSNo ratings yet

- 2008 Credit Card Bulk Provider RequirementsDocument112 pages2008 Credit Card Bulk Provider RequirementsIRSNo ratings yet

- Transaction Report: Zahid AbuDocument4 pagesTransaction Report: Zahid AbuSãbbìŕ RàhmâñNo ratings yet

- Offer: It Part No. Quty PU Price/unit Total Price Description Extra Deduction or Surchar EUR EURDocument3 pagesOffer: It Part No. Quty PU Price/unit Total Price Description Extra Deduction or Surchar EUR EURMichelNo ratings yet

- SB Control Procedure-LatestDocument30 pagesSB Control Procedure-LatestArunachalam KesavanNo ratings yet

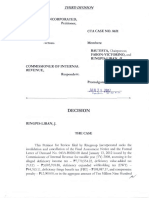

- Tsupreme Ourt: 31/epuhlic of TbeDocument16 pagesTsupreme Ourt: 31/epuhlic of TbeMonocrete Construction Philippines, Inc.No ratings yet

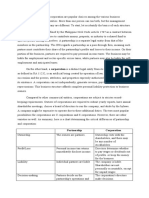

- Partnership Vs CorporationDocument2 pagesPartnership Vs CorporationRosee D.No ratings yet

- Invoice RI3242 From Railwire BroadbandDocument1 pageInvoice RI3242 From Railwire BroadbandArshad BashaNo ratings yet

- MPS 55R118 01583021L 09 2011Document2 pagesMPS 55R118 01583021L 09 2011vinayak_patil72No ratings yet

- Tax PDFDocument13 pagesTax PDFMinie KimNo ratings yet

- Exchange Rate Math Case Spreadsheet: NameDocument7 pagesExchange Rate Math Case Spreadsheet: NameRyan RebesNo ratings yet

- WWW - Carddelivery. Com - Google SearchDocument1 pageWWW - Carddelivery. Com - Google SearchOluwaseyi OwolabiNo ratings yet

- NikeDocument3 pagesNikeAdhiraj MukherjeeNo ratings yet

- Create Better QuotationsDocument3 pagesCreate Better QuotationsProduction TeamNo ratings yet

- Direct TaxationDocument2 pagesDirect TaxationSatyam SharmaNo ratings yet

- Screenshot (177) (20 Files Merged)Document28 pagesScreenshot (177) (20 Files Merged)Frances Marie Z. CieloNo ratings yet

- Ops Amw FRM D en SalesTaxAdjustmentForm AllStatesExceptWA2013Document6 pagesOps Amw FRM D en SalesTaxAdjustmentForm AllStatesExceptWA2013Ma'at MutamuntatNo ratings yet

- Statement of Account: Transaction Date Description Debit Credit Available BalanceDocument4 pagesStatement of Account: Transaction Date Description Debit Credit Available BalanceAk AndroidNo ratings yet

- Advising Payslip 22299223 Asef Ahmed ShimantoDocument1 pageAdvising Payslip 22299223 Asef Ahmed ShimantoShimanto KhanNo ratings yet

- TSD 428522500305 R PosDocument3 pagesTSD 428522500305 R Posvxryg557pfNo ratings yet

- Ritegroup v. CADocument39 pagesRitegroup v. CARenzo Ross Certeza SarteNo ratings yet

- Bank StatementDocument5 pagesBank StatementAshwani KumarNo ratings yet

- Stock Account of Inputs, For Use in or in Relation To The Manufacture of Final Products, Issued For Clearance On Payment of DutyDocument3 pagesStock Account of Inputs, For Use in or in Relation To The Manufacture of Final Products, Issued For Clearance On Payment of Dutykumar45caNo ratings yet

- W-9 Tax FormDocument4 pagesW-9 Tax FormMika DjokaNo ratings yet

- Entrance Counseling Guide For Direct Loan Borrowers: WWW - Dl.ed - GovDocument5 pagesEntrance Counseling Guide For Direct Loan Borrowers: WWW - Dl.ed - Govanon-417085No ratings yet

- Client Prepaid Form: Customer InformationDocument2 pagesClient Prepaid Form: Customer InformationTony GaryNo ratings yet

- COMPLETE PRICE LIST OF FORMALITIES SERVICESDocument14 pagesCOMPLETE PRICE LIST OF FORMALITIES SERVICESA.T Puteri SastrawidjayaNo ratings yet