You might also like

- Maximizing Your Wealth: A Comprehensive Guide to Understanding Gross and Net SalaryFrom EverandMaximizing Your Wealth: A Comprehensive Guide to Understanding Gross and Net SalaryNo ratings yet

- Defined Benefit Pension PlanDocument8 pagesDefined Benefit Pension Planhenok AbebeNo ratings yet

- Chapter 2 Lecture Notes.2021Document15 pagesChapter 2 Lecture Notes.2021Hoyin SinNo ratings yet

- Asset Management-Pension FundsDocument9 pagesAsset Management-Pension FundsKen BiiNo ratings yet

- Demas - Task 2Document7 pagesDemas - Task 2DemastaufiqNo ratings yet

- The Beginner's Handbook to Retirement Funds: Investing for a Secure FutureFrom EverandThe Beginner's Handbook to Retirement Funds: Investing for a Secure FutureNo ratings yet

- Acivity Module 4Document2 pagesAcivity Module 4Honey TolentinoNo ratings yet

- Module 7 - Ia2 Final CBLDocument22 pagesModule 7 - Ia2 Final CBLErika EsguerraNo ratings yet

- CH20 PDFDocument81 pagesCH20 PDFelaine aureliaNo ratings yet

- Chapter 15 - Pensions and Other Postretirement BenefitsDocument35 pagesChapter 15 - Pensions and Other Postretirement Benefitselizabeth karinaNo ratings yet

- Pension As A Retirement BenefitDocument9 pagesPension As A Retirement BenefitPrashant SharmaNo ratings yet

- Ias 19 Employee BeneftDocument24 pagesIas 19 Employee Beneftesulawyer2001No ratings yet

- Employee BenefitDocument32 pagesEmployee BenefitnatiNo ratings yet

- Ias 19Document43 pagesIas 19Reever RiverNo ratings yet

- Issues in Financial Accounting 16th Edition Henderson Solutions ManualDocument27 pagesIssues in Financial Accounting 16th Edition Henderson Solutions Manualcomplinofficialjasms100% (26)

- EmployeebenefitsreportDocument172 pagesEmployeebenefitsreportMikaela LacabaNo ratings yet

- Pension Terminology FinalDocument8 pagesPension Terminology FinalEugeneNo ratings yet

- Far28 Employee BenefitsDocument26 pagesFar28 Employee BenefitsCzar John JaudNo ratings yet

- IAS 26 Accounting and Reporting by Retirement Benefit Plans: ScopeDocument5 pagesIAS 26 Accounting and Reporting by Retirement Benefit Plans: ScopevicsNo ratings yet

- Actuarial Glossary PDFDocument18 pagesActuarial Glossary PDFmiguelNo ratings yet

- Ias 19 - Employee Benefits QUESTION 57-17Document9 pagesIas 19 - Employee Benefits QUESTION 57-17Janella Gail ArenasNo ratings yet

- Chapter 17 Ia2 No ProblemsDocument23 pagesChapter 17 Ia2 No ProblemsJM Valonda Villena, CPA, MBANo ratings yet

- Pas-26 FarDocument8 pagesPas-26 FarMarie dela sernaNo ratings yet

- Monika Rehman Roll No 10Document19 pagesMonika Rehman Roll No 10Monika RehmanNo ratings yet

- IAS 26 - Accounting and Reporting by Retirement BenefitDocument18 pagesIAS 26 - Accounting and Reporting by Retirement Benefitiqbal.ais152No ratings yet

- Pension Chap 1 IntroductionDocument5 pagesPension Chap 1 IntroductionJoe KimNo ratings yet

- DOCUMENT J (P)Document4 pagesDOCUMENT J (P)DimakatsoNo ratings yet

- SMChap 013Document49 pagesSMChap 013testbank100% (5)

- Accounting For Pensions and Postretirement BenefitsDocument3 pagesAccounting For Pensions and Postretirement BenefitsDhivena JeonNo ratings yet

- Tax Chapter 13 14th EditionDocument47 pagesTax Chapter 13 14th Editiontrenn175% (4)

- VillanuevaJohnLloydA Module4ActivityDocument2 pagesVillanuevaJohnLloydA Module4ActivityJan JanNo ratings yet

- International Accounting Standard 26 Accounting and Reporting by Retirement Benefit PlansDocument7 pagesInternational Accounting Standard 26 Accounting and Reporting by Retirement Benefit PlansmovelikejaggerNo ratings yet

- IAS 19 - Employee BenefitDocument49 pagesIAS 19 - Employee BenefitShah Kamal100% (2)

- Pas 19Document38 pagesPas 19Justine VeralloNo ratings yet

- Employee Benefit and Pension SchemesDocument35 pagesEmployee Benefit and Pension SchemesPayal Harshil Shah100% (2)

- Employee Benefits: PAS 19 Corpuz, Mary Lorie Anne ODocument38 pagesEmployee Benefits: PAS 19 Corpuz, Mary Lorie Anne OMarylorieanne CorpuzNo ratings yet

- Defined-Contribution and Defined-Benefit PlansDocument1 pageDefined-Contribution and Defined-Benefit PlansTawanda B MatsokotereNo ratings yet

- Salient Features of The Employees Provident Funds and Miscellaneous Provisions Act, 1952Document3 pagesSalient Features of The Employees Provident Funds and Miscellaneous Provisions Act, 1952Fency Jenus67% (3)

- Accounting and Reporting by Retirement Benefit PlansDocument6 pagesAccounting and Reporting by Retirement Benefit PlansTanvir PrantoNo ratings yet

- Foundations of Financial Markets and Institutions 4th Edition Fabozzi Solutions ManualDocument8 pagesFoundations of Financial Markets and Institutions 4th Edition Fabozzi Solutions Manualfinificcodille6d3h100% (22)

- Financial Reporting 1St Edition Loftus Solutions Manual Full Chapter PDFDocument57 pagesFinancial Reporting 1St Edition Loftus Solutions Manual Full Chapter PDFalicebellamyq3yj100% (10)

- Pension Topic One and TwoDocument7 pagesPension Topic One and Twonogarap767No ratings yet

- PAT P13 Notes - Ias 19, 10, Ifrs 11 & Ifrs 12Document14 pagesPAT P13 Notes - Ias 19, 10, Ifrs 11 & Ifrs 12HSFXHFHXNo ratings yet

- Cash Balance PlansDocument11 pagesCash Balance Plansmphillips36111No ratings yet

- TaxDocument4 pagesTaxGia Serilla100% (1)

- Summarizing Chapter 17 Herring Ton The Risk ManagementDocument4 pagesSummarizing Chapter 17 Herring Ton The Risk ManagementMd Shohag AliNo ratings yet

- A Project Report On Employee Benefit Scheme in PVT Sector: CtrlsoftDocument62 pagesA Project Report On Employee Benefit Scheme in PVT Sector: CtrlsoftArjunNo ratings yet

- Chapter 20Document21 pagesChapter 20Diana SantosNo ratings yet

- What Does Plan Sponsor Mean?Document7 pagesWhat Does Plan Sponsor Mean?moeed8393No ratings yet

- IC 83 - Compressed-5Document50 pagesIC 83 - Compressed-5purnachandrashee1No ratings yet

- Business Analyst Job InterviewDocument10 pagesBusiness Analyst Job InterviewNaveen PandeyNo ratings yet

- Provident FundDocument6 pagesProvident Fundalan finianNo ratings yet

- Ias 19Document5 pagesIas 19Tope JohnNo ratings yet

- Unit 03Document9 pagesUnit 03bobo tangaNo ratings yet

- Ias 19 - Employee BenefitsDocument6 pagesIas 19 - Employee BenefitsIfyNo ratings yet

- CH 09Document10 pagesCH 09Md.Rakib MiaNo ratings yet

- Submitted To: Amita Sharma Submitted By: Aditya Kumar Section-A Enrollment No. - 16flicddno1006Document14 pagesSubmitted To: Amita Sharma Submitted By: Aditya Kumar Section-A Enrollment No. - 16flicddno1006Aditya PandeyNo ratings yet

- Figure6 2Document1 pageFigure6 2api-3705877No ratings yet

- Strategic Planning ModelDocument55 pagesStrategic Planning Modelapi-3705877100% (1)

- Figure6 4Document1 pageFigure6 4api-3705877No ratings yet

- Analytical Thinking TrainingDocument58 pagesAnalytical Thinking Trainingcyberhansraj100% (2)

- Performance Management - Start Where You Are, Use What You HaveDocument70 pagesPerformance Management - Start Where You Are, Use What You HaveJuan José G.No ratings yet

- Project Plan: Balanced Scorecard Design and Development PlanDocument15 pagesProject Plan: Balanced Scorecard Design and Development Planrws1000No ratings yet

- Performance Measure Tool KitDocument9 pagesPerformance Measure Tool Kitapi-3705877No ratings yet

- SubrosDocument22 pagesSubrosapi-3705877100% (1)

- Venkata RamanaDocument37 pagesVenkata Ramanaapi-3705877No ratings yet

- 005 An FundingDocument27 pages005 An Fundingapi-3705877No ratings yet

- 48 National Cost Convention, 2007: Inaugural Address On Sustaining The Higher GrowthDocument8 pages48 National Cost Convention, 2007: Inaugural Address On Sustaining The Higher Growthapi-3705877No ratings yet

- The Management Accountant's Role in Today's Retail EnvironmentDocument34 pagesThe Management Accountant's Role in Today's Retail Environmentapi-3705877No ratings yet

- IT & ITES Growth Through Business Excellence: A Presentation at The 48 National Convention ofDocument11 pagesIT & ITES Growth Through Business Excellence: A Presentation at The 48 National Convention ofapi-3705877No ratings yet

- An Ram AnDocument27 pagesAn Ram Anapi-3705877No ratings yet

- Performance Budgeting - Module 5Document25 pagesPerformance Budgeting - Module 5bermazerNo ratings yet

- SAP AAS 1 To 32Document200 pagesSAP AAS 1 To 32api-3705877100% (1)

- Cma App Cao IaDocument1 pageCma App Cao Iaapi-3705877No ratings yet

- Practical Guidance For ManagementDocument153 pagesPractical Guidance For Managementapi-3839197No ratings yet

- As 26 Intangible AssetsDocument26 pagesAs 26 Intangible Assetsapi-3705877No ratings yet

- Unit 3 Unit 5 FinalDocument47 pagesUnit 3 Unit 5 FinalKit Chester Pingkian100% (1)

- Chapter 17Document54 pagesChapter 17wennstyleNo ratings yet

- TeachersDocument23 pagesTeachersMariane Joyce MianoNo ratings yet

- 05 Social Security How Work Affects Your Benefits En-05-10069Document10 pages05 Social Security How Work Affects Your Benefits En-05-10069api-309082881No ratings yet

- Retirement CalculatorDocument7 pagesRetirement CalculatorInside XploreNo ratings yet

- Chapter 5 Employee Benefits Part 1Document7 pagesChapter 5 Employee Benefits Part 1christianNo ratings yet

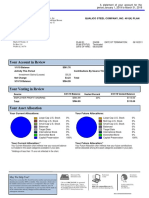

- Your Account in Review: Qualico Steel Company, Inc. 401 (K) PlanDocument3 pagesYour Account in Review: Qualico Steel Company, Inc. 401 (K) PlanmartyNo ratings yet

- Case Digest - Aquino Vs NLRCDocument2 pagesCase Digest - Aquino Vs NLRCZh Rm100% (1)

- The Benefits of An Ageing PopulationDocument9 pagesThe Benefits of An Ageing PopulationYa LiNo ratings yet

- Go Ms No 99 Dt.27!6!18 Replacing Existing Service Register With e Service BookDocument21 pagesGo Ms No 99 Dt.27!6!18 Replacing Existing Service Register With e Service BookAnonymous cRMw8feac8No ratings yet

- Company Profile of HDFC Standard Life: 8/26/2010 Adit SarinDocument26 pagesCompany Profile of HDFC Standard Life: 8/26/2010 Adit SarinadisarinNo ratings yet

- PAz Vs Northern TobaccoDocument2 pagesPAz Vs Northern TobaccoKhristienne BernabeNo ratings yet

- Internship Report: Allied Bank Limited (Abl) GT Road Branch, PeshawarDocument44 pagesInternship Report: Allied Bank Limited (Abl) GT Road Branch, PeshawarFaheem Ejaz100% (1)

- LET Reviewer 2018Document55 pagesLET Reviewer 2018Jovy C. AndresNo ratings yet

- 7PR 0004465 3492ffc01412943 0199Document1 page7PR 0004465 3492ffc01412943 0199pankaj645924No ratings yet

- Financial Planning ReportDocument75 pagesFinancial Planning ReportAruna Ambastha100% (7)

- Letter To Eskom Board MolefeDocument3 pagesLetter To Eskom Board MolefeMatthewLeCordeurNo ratings yet

- Nestle Phils v. NLRC GR 91231, February 4, 1991Document2 pagesNestle Phils v. NLRC GR 91231, February 4, 1991Ellis LagascaNo ratings yet

- Have It All Kris KrohnDocument264 pagesHave It All Kris KrohnLuciano Goya BillottaNo ratings yet

- UKRI Sickness Absence PolicyDocument28 pagesUKRI Sickness Absence PolicyanupkrajakNo ratings yet

- ERIN LEWIS - MARS-Member Annual Retirement Statement - 2023Document2 pagesERIN LEWIS - MARS-Member Annual Retirement Statement - 2023Erin LewisNo ratings yet

- Townsend 1979Document28 pagesTownsend 1979api-534238122No ratings yet

- Retirement Full CaseDocument102 pagesRetirement Full CaseJesimiel CarlosNo ratings yet

- EPS Pension Calculator NewDocument7 pagesEPS Pension Calculator NewpswaminathanNo ratings yet

- 2020-21 State of The North Carolina Teaching ProfessionDocument43 pages2020-21 State of The North Carolina Teaching ProfessionKeung HuiNo ratings yet

- PUPUN00128450000024740 NewDocument3 pagesPUPUN00128450000024740 NewOnkarNo ratings yet

- Revised Punjab Leave Rules 1981 UpdatedDocument39 pagesRevised Punjab Leave Rules 1981 UpdatedMuhammad Sumair83% (6)

- Chpts 1-6 Employee Benefits QuizDocument17 pagesChpts 1-6 Employee Benefits QuizKevin Fernando100% (1)

- The Future For Investors - Siegel - Group 4Document58 pagesThe Future For Investors - Siegel - Group 4SrilakshmiNo ratings yet

- MCQSDocument5 pagesMCQSJiteshNo ratings yet

- Getting to Yes: How to Negotiate Agreement Without Giving InFrom EverandGetting to Yes: How to Negotiate Agreement Without Giving InRating: 4 out of 5 stars4/5 (652)

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)From EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Rating: 4.5 out of 5 stars4.5/5 (14)

- Purchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsFrom EverandPurchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsRating: 5 out of 5 stars5/5 (1)

- The ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!From EverandThe ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!Rating: 4.5 out of 5 stars4.5/5 (14)

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindFrom EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindRating: 5 out of 5 stars5/5 (231)

- How to Measure Anything: Finding the Value of "Intangibles" in BusinessFrom EverandHow to Measure Anything: Finding the Value of "Intangibles" in BusinessRating: 4.5 out of 5 stars4.5/5 (28)

- The Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)From EverandThe Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)Rating: 4 out of 5 stars4/5 (33)

- Accounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsFrom EverandAccounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsRating: 4 out of 5 stars4/5 (7)

- A Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineFrom EverandA Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineNo ratings yet

- The E-Myth Chief Financial Officer: Why Most Small Businesses Run Out of Money and What to Do About ItFrom EverandThe E-Myth Chief Financial Officer: Why Most Small Businesses Run Out of Money and What to Do About ItRating: 4.5 out of 5 stars4.5/5 (14)

- Ratio Analysis Fundamentals: How 17 Financial Ratios Can Allow You to Analyse Any Business on the PlanetFrom EverandRatio Analysis Fundamentals: How 17 Financial Ratios Can Allow You to Analyse Any Business on the PlanetRating: 4.5 out of 5 stars4.5/5 (14)

- Accounting For Small Businesses QuickStart Guide: Understanding Accounting For Your Sole Proprietorship, Startup, & LLCFrom EverandAccounting For Small Businesses QuickStart Guide: Understanding Accounting For Your Sole Proprietorship, Startup, & LLCRating: 5 out of 5 stars5/5 (1)

- How to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)From EverandHow to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)Rating: 4.5 out of 5 stars4.5/5 (5)

- Overcoming Underearning(TM): A Simple Guide to a Richer LifeFrom EverandOvercoming Underearning(TM): A Simple Guide to a Richer LifeRating: 4 out of 5 stars4/5 (21)

- The Intelligent Investor, Rev. Ed: The Definitive Book on Value InvestingFrom EverandThe Intelligent Investor, Rev. Ed: The Definitive Book on Value InvestingRating: 4.5 out of 5 stars4.5/5 (760)

- Financial Accounting For Dummies: 2nd EditionFrom EverandFinancial Accounting For Dummies: 2nd EditionRating: 5 out of 5 stars5/5 (10)

- Finance Basics (HBR 20-Minute Manager Series)From EverandFinance Basics (HBR 20-Minute Manager Series)Rating: 4.5 out of 5 stars4.5/5 (32)

- Start, Study and Pass The CPA Exam FAST - Proven 8 Step CPA Exam Study PlaybookFrom EverandStart, Study and Pass The CPA Exam FAST - Proven 8 Step CPA Exam Study PlaybookRating: 5 out of 5 stars5/5 (4)

- Attention Pays: How to Drive Profitability, Productivity, and AccountabilityFrom EverandAttention Pays: How to Drive Profitability, Productivity, and AccountabilityNo ratings yet

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesFrom EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesNo ratings yet

- Your Amazing Itty Bitty(R) Personal Bookkeeping BookFrom EverandYour Amazing Itty Bitty(R) Personal Bookkeeping BookNo ratings yet

- Accounting Principles: Learn The Simple and Effective Methods of Basic Accounting And Bookkeeping Using This comprehensive Guide for Beginners(quick-books,made simple,easy,managerial,finance)From EverandAccounting Principles: Learn The Simple and Effective Methods of Basic Accounting And Bookkeeping Using This comprehensive Guide for Beginners(quick-books,made simple,easy,managerial,finance)Rating: 4.5 out of 5 stars4.5/5 (5)

- The Credit Formula: The Guide To Building and Rebuilding Lendable CreditFrom EverandThe Credit Formula: The Guide To Building and Rebuilding Lendable CreditRating: 5 out of 5 stars5/5 (1)