You might also like

- Food Outlook: Biannual Report on Global Food Markets May 2019From EverandFood Outlook: Biannual Report on Global Food Markets May 2019No ratings yet

- Food Outlook: Biannual Report on Global Food Markets: June 2020From EverandFood Outlook: Biannual Report on Global Food Markets: June 2020No ratings yet

- India's $105M Cotton Textile Exports to Nigeria Have Growth PotentialDocument80 pagesIndia's $105M Cotton Textile Exports to Nigeria Have Growth PotentialLoveth KonniaNo ratings yet

- Value Chain Analysis of Organic Cotton Sub Sector in TanzaniaDocument15 pagesValue Chain Analysis of Organic Cotton Sub Sector in TanzaniaOchieng JustusNo ratings yet

- Zimbabwe Cotton Sector Value Chain AnalysisDocument43 pagesZimbabwe Cotton Sector Value Chain AnalysisHavanyaniNo ratings yet

- Agriculture Law: RS21712Document6 pagesAgriculture Law: RS21712AgricultureCaseLawNo ratings yet

- Jute Matters WebDocument60 pagesJute Matters WebAsraar AhmedNo ratings yet

- Organic Cotton CultivationDocument11 pagesOrganic Cotton CultivationSambitPriyadarshiNo ratings yet

- The Cotton Industry in The Philippines: ' Country StatementDocument8 pagesThe Cotton Industry in The Philippines: ' Country StatementJocelle AlcantaraNo ratings yet

- Philippine Abaca Industry Roadmap 2018 2022Document129 pagesPhilippine Abaca Industry Roadmap 2018 2022Jet Evasco100% (2)

- Produce Poultry FeedDocument26 pagesProduce Poultry FeedMOHIT KHATWANINo ratings yet

- Ethiopia Cotton Production Annual - Addis Ababa - Ethiopia - 5-29-2019Document8 pagesEthiopia Cotton Production Annual - Addis Ababa - Ethiopia - 5-29-2019DemelashNo ratings yet

- Dossier Annex II.4Document39 pagesDossier Annex II.4Ganesh PMNo ratings yet

- Jute Diversified ProductDocument39 pagesJute Diversified ProductIffat Ara AhmedNo ratings yet

- F L C P C I U: ARM Evel Otton Roduction Onstraints N GandaDocument32 pagesF L C P C I U: ARM Evel Otton Roduction Onstraints N GandaIsaka IsseNo ratings yet

- Regional Workshop On Trade Capacity Building & Private Sector DevelopmentDocument31 pagesRegional Workshop On Trade Capacity Building & Private Sector Developmentsrhq786No ratings yet

- Textile Industry Growth in PakistanDocument41 pagesTextile Industry Growth in PakistanHuma AliNo ratings yet

- Textile PDFDocument31 pagesTextile PDFsweetshah2No ratings yet

- Textile Industry of PakistanDocument12 pagesTextile Industry of PakistanTayyab Yaqoob QaziNo ratings yet

- Quantitative and Qualitative Requirements of Cotton For IndustryDocument4 pagesQuantitative and Qualitative Requirements of Cotton For IndustrySabesh MuniaswamiNo ratings yet

- Pakistan's Textile Industry: A Backbone of the EconomyDocument59 pagesPakistan's Textile Industry: A Backbone of the EconomyFaiEz AmEen KhanNo ratings yet

- Cotton Hand BookDocument75 pagesCotton Hand BookEdnet KenyaNo ratings yet

- Ethiopian Tanners Association - Current Problems of The Leather Industry - 2000Document6 pagesEthiopian Tanners Association - Current Problems of The Leather Industry - 2000greenefutures100% (1)

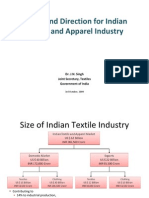

- Status and DirectionDocument28 pagesStatus and Directionmlganesh666No ratings yet

- Abaca-Production and ManagementDocument4 pagesAbaca-Production and Managementkenn1o10% (1)

- Coconut Coir Value Chain AnalysisDocument35 pagesCoconut Coir Value Chain AnalysisMarian E Boquiren83% (6)

- Chapter 1Document67 pagesChapter 1satseehraNo ratings yet

- Https WWW IhsDocument5 pagesHttps WWW IhsrishikeshmandawadNo ratings yet

- Research Report On Spinning Sector of Bangladesh-InitiationDocument24 pagesResearch Report On Spinning Sector of Bangladesh-InitiationjohnsumonNo ratings yet

- Garments Sector - PACRA Research - Dec20 - 1607595607Document20 pagesGarments Sector - PACRA Research - Dec20 - 1607595607MUHAMMAD HAMZANo ratings yet

- Cotton: Trends in Global Production, Trade and PolicyDocument14 pagesCotton: Trends in Global Production, Trade and PolicyInternational Centre for Trade and Sustainable DevelopmentNo ratings yet

- Textiles Sector - Achievement ReportDocument12 pagesTextiles Sector - Achievement ReportAnkitaNo ratings yet

- Nigeria Dairy MarketDocument15 pagesNigeria Dairy Marketdangler310% (1)

- Cotton by SaurabhDocument19 pagesCotton by SaurabhsaurabhNo ratings yet

- Spinning Project Profile FinalDocument23 pagesSpinning Project Profile FinalFaizan Motiwala67% (3)

- Cotton GinningDocument4 pagesCotton Ginningb4i_i4bNo ratings yet

- Cotton Fibre Quality Research Needs in IndiaDocument11 pagesCotton Fibre Quality Research Needs in IndiaprabhjotseehraNo ratings yet

- Abaca VCA (REGION 5) PDFDocument65 pagesAbaca VCA (REGION 5) PDFAks Somvanshi67% (3)

- Pakistan Cotton Production and TCP's Price Stabilization RoleDocument9 pagesPakistan Cotton Production and TCP's Price Stabilization RoleaowaisNo ratings yet

- Call For Support Woven For Raw MaterialDocument10 pagesCall For Support Woven For Raw MaterialSamwovenNo ratings yet

- Elite Fabs Deva - MsDocument51 pagesElite Fabs Deva - MsDevaragulNo ratings yet

- Indian Textile Industry: October 2006Document22 pagesIndian Textile Industry: October 2006Vikram Bhati100% (1)

- Economics of Corn Farming FinalDocument67 pagesEconomics of Corn Farming FinalOliver TalipNo ratings yet

- Atl - Textile IndustryDocument4 pagesAtl - Textile IndustryIa LoureenNo ratings yet

- The Philippine Coconut Industry: Performance, Issues and RecommendationsDocument8 pagesThe Philippine Coconut Industry: Performance, Issues and RecommendationsMhean Cortez Absulio100% (1)

- Commodity ReportDocument8 pagesCommodity Reporthamna MalikNo ratings yet

- Status of Global Paper IndustryDocument23 pagesStatus of Global Paper IndustryarjunanpnNo ratings yet

- Research On GTPDocument24 pagesResearch On GTPRosemary AsiamahNo ratings yet

- Activity 2 - Industry StationerDocument7 pagesActivity 2 - Industry StationerKrizza Camelle CalipusanNo ratings yet

- Finding The Moral Fiber: Why Reform Is Urgently Needed For A Fair Cotton TradeDocument48 pagesFinding The Moral Fiber: Why Reform Is Urgently Needed For A Fair Cotton TradeOxfamNo ratings yet

- Los Grobo G.grobocopatelDocument31 pagesLos Grobo G.grobocopatelJames Smart100% (1)

- Internship Report On Gohar TextileDocument107 pagesInternship Report On Gohar Textilesiaapa60% (5)

- Milling, Pet Food and Animal Feed: Sub-Sector Skills PlanDocument46 pagesMilling, Pet Food and Animal Feed: Sub-Sector Skills PlanElisaNo ratings yet

- TNI Agrarian Justice Programme Examines Trends in Brazil's Sugarcane IndustryDocument24 pagesTNI Agrarian Justice Programme Examines Trends in Brazil's Sugarcane IndustryHimanshu MogheNo ratings yet

- Cote D Ivoire Agricultural Sector UpdateDocument75 pagesCote D Ivoire Agricultural Sector UpdateSan SouciNo ratings yet

- Agriculture Law: RS20896Document6 pagesAgriculture Law: RS20896AgricultureCaseLawNo ratings yet

- Problems and Prospects of Exporting Jute From BangladeshDocument25 pagesProblems and Prospects of Exporting Jute From BangladeshNurul Absar RashedNo ratings yet

- Textile Industry BackgroundDocument26 pagesTextile Industry BackgroundPunit Francis100% (1)

- Food Outlook: Biannual Report on Global Food Markets: June 2022From EverandFood Outlook: Biannual Report on Global Food Markets: June 2022No ratings yet

- Food Outlook: Biannual Report on Global Food Markets: November 2022From EverandFood Outlook: Biannual Report on Global Food Markets: November 2022No ratings yet

- En Cima Market StudyDocument67 pagesEn Cima Market Studyapi-3838281100% (2)

- Technical Appraisal Table of ContentsDocument5 pagesTechnical Appraisal Table of Contentsapi-3838281No ratings yet

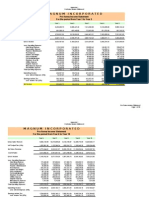

- Magnum Financial FinalDocument27 pagesMagnum Financial Finalapi-3838281No ratings yet

- Magnum Final Finally FsDocument30 pagesMagnum Final Finally Fsapi-3838281No ratings yet

- Technical Appraisal FinalDocument67 pagesTechnical Appraisal Finalapi-3838281No ratings yet

- Power Point - Market Demand ComputationDocument9 pagesPower Point - Market Demand Computationapi-3838281100% (1)

- En Cima Appendix - 3Document1 pageEn Cima Appendix - 3api-3838281No ratings yet

- En Cima Appendix - 5Document5 pagesEn Cima Appendix - 5api-3838281No ratings yet

- En Cima Appendix - 4Document2 pagesEn Cima Appendix - 4api-3838281No ratings yet

- Power PointDocument7 pagesPower Pointapi-3838281No ratings yet

- Power Point TechnicalDocument9 pagesPower Point Technicalapi-3838281No ratings yet

- Technical AppraisalDocument64 pagesTechnical Appraisalapi-3838281No ratings yet

- En Cima Appendix - 2Document2 pagesEn Cima Appendix - 2api-3838281No ratings yet

- Power Point - MarketingDocument11 pagesPower Point - Marketingapi-3838281No ratings yet

- Pant SaloonDocument27 pagesPant Saloonapi-3838281No ratings yet

- My Part For Report FinalDocument4 pagesMy Part For Report Finalapi-3838281No ratings yet

- Denim Sewing GuidelinesDocument3 pagesDenim Sewing Guidelinesapi-3838281No ratings yet

- My Part For ReportDocument5 pagesMy Part For Reportapi-3838281No ratings yet

- Viktor JeansDocument2 pagesViktor Jeansapi-3838281No ratings yet

- WE'RE NOT Sweatshops - Garments Exporters Worry About Int'l ImageDocument2 pagesWE'RE NOT Sweatshops - Garments Exporters Worry About Int'l Imageapi-3838281No ratings yet

- Org Structure - HR Matters - Daily OpernsDocument10 pagesOrg Structure - HR Matters - Daily Opernsapi-3838281No ratings yet

- Pattern For Org StructureDocument8 pagesPattern For Org Structureapi-3838281No ratings yet

- Operating CostsDocument13 pagesOperating Costsapi-3838281No ratings yet

- The Philippine Garments IndustryDocument4 pagesThe Philippine Garments Industryapi-3838281100% (3)

- RectoDocument2 pagesRectoapi-3838281No ratings yet

- RRJ JeansDocument1 pageRRJ Jeansapi-3838281100% (1)

- Plains and PrintsDocument2 pagesPlains and Printsapi-3838281100% (3)

- Philippines Cotton and Products Annual 2004Document3 pagesPhilippines Cotton and Products Annual 2004api-3838281No ratings yet

- PIF2006Document57 pagesPIF2006api-3838281No ratings yet

- June Garments Exports Adjust To PriceDocument2 pagesJune Garments Exports Adjust To Priceapi-3838281No ratings yet

- Quality Management in Digital ImagingDocument71 pagesQuality Management in Digital ImagingKampus Atro Bali0% (1)

- Level 3 Repair PBA Parts LayoutDocument32 pagesLevel 3 Repair PBA Parts LayoutabivecueNo ratings yet

- Honda Wave Parts Manual enDocument61 pagesHonda Wave Parts Manual enMurat Kaykun86% (94)

- Petty Cash Vouchers:: Accountability Accounted ForDocument3 pagesPetty Cash Vouchers:: Accountability Accounted ForCrizhae OconNo ratings yet

- 2014 mlc703 AssignmentDocument6 pages2014 mlc703 AssignmentToral ShahNo ratings yet

- Music 7: Music of Lowlands of LuzonDocument14 pagesMusic 7: Music of Lowlands of LuzonGhia Cressida HernandezNo ratings yet

- Us Virgin Island WWWWDocument166 pagesUs Virgin Island WWWWErickvannNo ratings yet

- The European Journal of Applied Economics - Vol. 16 #2Document180 pagesThe European Journal of Applied Economics - Vol. 16 #2Aleksandar MihajlovićNo ratings yet

- C6030 BrochureDocument2 pagesC6030 Brochureibraheem aboyadakNo ratings yet

- Manual Analizador Fluoruro HachDocument92 pagesManual Analizador Fluoruro HachAitor de IsusiNo ratings yet

- FINAL A-ENHANCED MODULES TO IMPROVE LEARNERS - EditedDocument22 pagesFINAL A-ENHANCED MODULES TO IMPROVE LEARNERS - EditedMary Cielo PadilloNo ratings yet

- ITU SURVEY ON RADIO SPECTRUM MANAGEMENT 17 01 07 Final PDFDocument280 pagesITU SURVEY ON RADIO SPECTRUM MANAGEMENT 17 01 07 Final PDFMohamed AliNo ratings yet

- PandPofCC (8th Edition)Document629 pagesPandPofCC (8th Edition)Carlos Alberto CaicedoNo ratings yet

- Polyol polyether+NCO Isupur PDFDocument27 pagesPolyol polyether+NCO Isupur PDFswapon kumar shillNo ratings yet

- Riddles For KidsDocument15 pagesRiddles For KidsAmin Reza100% (8)

- Rohit Patil Black BookDocument19 pagesRohit Patil Black BookNaresh KhutikarNo ratings yet

- Orc & Goblins VII - 2000pts - New ABDocument1 pageOrc & Goblins VII - 2000pts - New ABDave KnattNo ratings yet

- Propiedades Grado 50 A572Document2 pagesPropiedades Grado 50 A572daniel moreno jassoNo ratings yet

- Lifespan Development Canadian 6th Edition Boyd Test BankDocument57 pagesLifespan Development Canadian 6th Edition Boyd Test Bankshamekascoles2528zNo ratings yet

- CR Vs MarubeniDocument15 pagesCR Vs MarubeniSudan TambiacNo ratings yet

- Briana SmithDocument3 pagesBriana SmithAbdul Rafay Ali KhanNo ratings yet

- FS2004 - The Aircraft - CFG FileDocument5 pagesFS2004 - The Aircraft - CFG FiletumbNo ratings yet

- Exercises2 SolutionsDocument7 pagesExercises2 Solutionspedroagv08No ratings yet

- Guiding Childrens Social Development and Learning 8th Edition Kostelnik Test BankDocument16 pagesGuiding Childrens Social Development and Learning 8th Edition Kostelnik Test Bankoglepogy5kobgk100% (27)

- Agricultural Engineering Comprehensive Board Exam Reviewer: Agricultural Processing, Structures, and Allied SubjectsDocument84 pagesAgricultural Engineering Comprehensive Board Exam Reviewer: Agricultural Processing, Structures, and Allied SubjectsRachel vNo ratings yet

- International Certificate in WealthDocument388 pagesInternational Certificate in Wealthabhishek210585100% (2)

- How Psychology Has Changed Over TimeDocument2 pagesHow Psychology Has Changed Over TimeMaedot HaddisNo ratings yet

- Estimation of Working CapitalDocument12 pagesEstimation of Working CapitalsnehalgaikwadNo ratings yet

- BIBLIO Eric SwyngedowDocument34 pagesBIBLIO Eric Swyngedowadriank1975291No ratings yet

- 2-Port Antenna Frequency Range Dual Polarization HPBW Adjust. Electr. DTDocument5 pages2-Port Antenna Frequency Range Dual Polarization HPBW Adjust. Electr. DTIbrahim JaberNo ratings yet