You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5795)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Chapter Six: Bond MarketsDocument39 pagesChapter Six: Bond MarketsYash PiyushNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- A Philosophical Analysis On The Dynamics of Utang Na Loob Final ManuscriptDocument33 pagesA Philosophical Analysis On The Dynamics of Utang Na Loob Final ManuscriptALEXANDRA SANAGUSTIN100% (1)

- The Dark Side of Valuation (Slides)Document98 pagesThe Dark Side of Valuation (Slides)Johnathan Fitz KennedyNo ratings yet

- APLMA Single Borrower Single Currency Term Facility Agreement - New Revised Template (AA)Document81 pagesAPLMA Single Borrower Single Currency Term Facility Agreement - New Revised Template (AA)Muhammad Reza Fahriadi100% (3)

- The National Internal Revenue CodeDocument159 pagesThe National Internal Revenue CodeKath SantosNo ratings yet

- Letter of Guarantee by CorporateDocument6 pagesLetter of Guarantee by CorporateTira MagdNo ratings yet

- Case No. 1 Bangko Sentral V Coa G.R. NO. 168964 JANUARY 23, 2006Document2 pagesCase No. 1 Bangko Sentral V Coa G.R. NO. 168964 JANUARY 23, 2006Babes Aubrey DelaCruz AquinoNo ratings yet

- Financial Planning and Forecasting Financial Statements: Answers To Beginning-Of-Chapter QuestionsDocument24 pagesFinancial Planning and Forecasting Financial Statements: Answers To Beginning-Of-Chapter Questionscostel11100% (1)

- Public Fiscal ManagementDocument5 pagesPublic Fiscal ManagementClarizze DailisanNo ratings yet

- Syllabus Credit ManagementDocument2 pagesSyllabus Credit ManagementMd Salah UddinNo ratings yet

- CollateralDocument3 pagesCollateralVeronicaNo ratings yet

- 5 6 7 Management of International Business ActivitiesDocument41 pages5 6 7 Management of International Business ActivitiesQuynh Anh NguyenNo ratings yet

- Obras Pias: Ancient TimesDocument6 pagesObras Pias: Ancient TimesShaina LimNo ratings yet

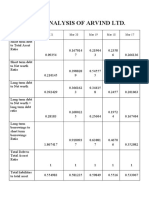

- Ratio Analysis of Arvind LTD.: Ratios Mar 21 Mar 20 Mar 19 Mar 18 Mar 17Document10 pagesRatio Analysis of Arvind LTD.: Ratios Mar 21 Mar 20 Mar 19 Mar 18 Mar 17simranNo ratings yet

- Sri Vijaya Bharati SeedsDocument23 pagesSri Vijaya Bharati SeedssurichimmaniNo ratings yet

- Session 3 - Companies Act - Merger, Amalgamation, Share Capital & DebentureDocument88 pagesSession 3 - Companies Act - Merger, Amalgamation, Share Capital & DebentureVaibhav JainNo ratings yet

- PAPER Muamalah EnglishDocument10 pagesPAPER Muamalah EnglishDeanita ChandrasariNo ratings yet

- Searle Company Ratio Analysis 2010 2011 2012Document63 pagesSearle Company Ratio Analysis 2010 2011 2012Kaleb VargasNo ratings yet

- Indiana Loan Broker AgreementDocument2 pagesIndiana Loan Broker AgreementalokprasadNo ratings yet

- Hockey Player On EBIXDocument20 pagesHockey Player On EBIXvram2000No ratings yet

- Eligibility For Issuance of CPDocument2 pagesEligibility For Issuance of CPsadathnooriNo ratings yet

- Guidelines On ICRR - 11.11.18Document40 pagesGuidelines On ICRR - 11.11.18jahanNo ratings yet

- Numerical Questions 5Document3 pagesNumerical Questions 5nabin bkNo ratings yet

- Cash Flow Statement Problems - Cpaj2007Document7 pagesCash Flow Statement Problems - Cpaj2007Iqra MughalNo ratings yet

- Ham Projects: Vijay M. Mistry Construction PVT LTDDocument12 pagesHam Projects: Vijay M. Mistry Construction PVT LTDJalpesh PitrodaNo ratings yet

- FIN3154-Group Assignment - April 2023-Updated 15 May 2023Document8 pagesFIN3154-Group Assignment - April 2023-Updated 15 May 2023L Thana LetchumiNo ratings yet

- Compound Interest MCQSDocument13 pagesCompound Interest MCQSNiranjan BiswalNo ratings yet

- FSTEP Islamic - Treasury - OperationDocument89 pagesFSTEP Islamic - Treasury - Operationalhoreya100% (1)

- AB CAIIB Paper 1 Module D Credit Management PDFDocument30 pagesAB CAIIB Paper 1 Module D Credit Management PDFRAVINDERNo ratings yet

- Calamity LoanDocument2 pagesCalamity LoanJu LanNo ratings yet