You might also like

- Exempt Vat RatesDocument8 pagesExempt Vat RatesRaghu AgNo ratings yet

- Supermarket Fun Activities Games Picture Dictionaries - 38602Document37 pagesSupermarket Fun Activities Games Picture Dictionaries - 38602Jan Albert AndagNo ratings yet

- Business Ideas to Make a Million Dollars or Some Money SometimeFrom EverandBusiness Ideas to Make a Million Dollars or Some Money SometimeNo ratings yet

- Bridgeport CT Guide To RecyclingDocument2 pagesBridgeport CT Guide To RecyclingBridgeportCTNo ratings yet

- Homemade: 707 Products to Make Yourself to Save Money and the EarthFrom EverandHomemade: 707 Products to Make Yourself to Save Money and the EarthNo ratings yet

- Greenstar Joint Recycling LeafletDocument2 pagesGreenstar Joint Recycling LeafletluckymulNo ratings yet

- Low-Fat Cake, Cheesecake, and Cookie Recipes: Eat Less Fat Now Without Sacrificing Flavor!From EverandLow-Fat Cake, Cheesecake, and Cookie Recipes: Eat Less Fat Now Without Sacrificing Flavor!No ratings yet

- Wish List of Items For Soldier Care PackagesDocument4 pagesWish List of Items For Soldier Care PackagesMichelle TaylorNo ratings yet

- Lesson 1 - GroceryDocument3 pagesLesson 1 - GrocerysamNo ratings yet

- The Complete Guide to Making Cheese, Butter, and Yogurt at Home: Everything You Need to Know Explained SimplyFrom EverandThe Complete Guide to Making Cheese, Butter, and Yogurt at Home: Everything You Need to Know Explained SimplyRating: 5 out of 5 stars5/5 (1)

- List of Items Under The Slab RateDocument17 pagesList of Items Under The Slab Ratebabbleproducts00No ratings yet

- NAFDAC Import GuidelinesDocument3 pagesNAFDAC Import Guidelinesmalibu-ngNo ratings yet

- WIC Authorized Food List Shopping Guide: April 5, 2010Document11 pagesWIC Authorized Food List Shopping Guide: April 5, 2010Tommy CarterNo ratings yet

- Shopping GuideDocument21 pagesShopping GuideKurt HendricksonNo ratings yet

- Homemade: How-to Make Hundreds of Everyday Products Fast, Fresh, and More NaturallyFrom EverandHomemade: How-to Make Hundreds of Everyday Products Fast, Fresh, and More NaturallyRating: 4.5 out of 5 stars4.5/5 (12)

- Food Guide For A Low Iodine DietDocument1 pageFood Guide For A Low Iodine Dietrekeshsidhu8822No ratings yet

- Low-Cholesterol Cookies: 85+ Easy-to-Follow Recipes with Nutrition InformationFrom EverandLow-Cholesterol Cookies: 85+ Easy-to-Follow Recipes with Nutrition InformationNo ratings yet

- 2022 Florida Back-To-School Sales Tax Holiday - External FAQs - ConsumersDocument10 pages2022 Florida Back-To-School Sales Tax Holiday - External FAQs - ConsumersMelissa R.No ratings yet

- Module 12 Hazmat and Restricted Items 1Document4 pagesModule 12 Hazmat and Restricted Items 1possesstrimaNo ratings yet

- Low-Fat Cookies: 85+ Easy-to-Follow Recipes with Nutrition InformationFrom EverandLow-Fat Cookies: 85+ Easy-to-Follow Recipes with Nutrition InformationNo ratings yet

- TL Power Point Obj 8.0-8.02 Part OneDocument21 pagesTL Power Point Obj 8.0-8.02 Part OneMistekee MaramagNo ratings yet

- Kitchenless Cooking: Unique Techniques for Cooking Large and Thrifty in a Small SpaceFrom EverandKitchenless Cooking: Unique Techniques for Cooking Large and Thrifty in a Small SpaceNo ratings yet

- Taste of Home Affordable Eats: 237 All Time Favorites that Won't Break the BankFrom EverandTaste of Home Affordable Eats: 237 All Time Favorites that Won't Break the BankRating: 5 out of 5 stars5/5 (1)

- The I Love Trader Joe's Vegetarian Cookbook: 150 Delicious and Healthy Recipes Using Foods from the World's Greatest Grocery StoreFrom EverandThe I Love Trader Joe's Vegetarian Cookbook: 150 Delicious and Healthy Recipes Using Foods from the World's Greatest Grocery StoreNo ratings yet

- Betty Crocker Cookbook, 12th Edition: Everything You Need to Know to Cook from ScratchFrom EverandBetty Crocker Cookbook, 12th Edition: Everything You Need to Know to Cook from ScratchRating: 4 out of 5 stars4/5 (262)

- Low-Sodium Cookies: 85+ Easy-to-Follow Recipes with Nutrition InformationFrom EverandLow-Sodium Cookies: 85+ Easy-to-Follow Recipes with Nutrition InformationNo ratings yet

- Reader's Digest Extraordinary Uses for Ordinary Things New EditionFrom EverandReader's Digest Extraordinary Uses for Ordinary Things New EditionReader's DigestNo ratings yet

- Retail EnglishDocument46 pagesRetail Englishsuprnd100% (2)

- The I Love Trader Joe's Plant-Based Cookbook: 150 Delicious Vegetarian and Vegan Recipes Using Foods from the World's Greatest Grocery StoreFrom EverandThe I Love Trader Joe's Plant-Based Cookbook: 150 Delicious Vegetarian and Vegan Recipes Using Foods from the World's Greatest Grocery StoreNo ratings yet

- The Everything Classic Recipes Book: 300 All-time Favorites Perfect for BeginnersFrom EverandThe Everything Classic Recipes Book: 300 All-time Favorites Perfect for BeginnersNo ratings yet

- Recycling InfoDocument2 pagesRecycling Infoapi-259246990No ratings yet

- Guide To Halal FoodsDocument4 pagesGuide To Halal FoodsFastabiqul KhairatNo ratings yet

- Reclaim The LunchboxDocument12 pagesReclaim The LunchboxS TANCREDNo ratings yet

- 1,001 Country Home Tips & Tricks: Household Hints for Cleaning, Gardening, Cooking, Sewing, and MoreFrom Everand1,001 Country Home Tips & Tricks: Household Hints for Cleaning, Gardening, Cooking, Sewing, and MoreRating: 5 out of 5 stars5/5 (1)

- The Green Aisle's Healthy Indulgence: More Than 75 Guilt-Free, All-Natural Recipes to Help You Lose Weight and Feel GreatFrom EverandThe Green Aisle's Healthy Indulgence: More Than 75 Guilt-Free, All-Natural Recipes to Help You Lose Weight and Feel GreatNo ratings yet

- WIC 34 Texas WIC Shopping Guide BrochureDocument11 pagesWIC 34 Texas WIC Shopping Guide BrochurerodneyNo ratings yet

- Buy Price Shopping ListDocument1 pageBuy Price Shopping ListPeanut d. DestroyerNo ratings yet

- Buy Price Shopping List under $40Document1 pageBuy Price Shopping List under $40Huckle Berry FinnNo ratings yet

- Business PlanDocument53 pagesBusiness PlanKelvin Jay Sebastian Sapla100% (1)

- California Food Tax LawDocument28 pagesCalifornia Food Tax Lawram0nes14No ratings yet

- Talas CatalogDocument256 pagesTalas CataloglimlerianNo ratings yet

- 2015 - 2016 Oklahoma School Testing Program (OSTP) Results: Oklahoma Core Curriculum Tests (OCCT)Document9 pages2015 - 2016 Oklahoma School Testing Program (OSTP) Results: Oklahoma Core Curriculum Tests (OCCT)Keaton FoxNo ratings yet

- State Supreme Court RulingsDocument42 pagesState Supreme Court RulingsKeaton FoxNo ratings yet

- OK Oil and Gas Tax Policy 2016 FinalDocument62 pagesOK Oil and Gas Tax Policy 2016 FinalKeaton FoxNo ratings yet

- Ruiz v. City of BethanyDocument27 pagesRuiz v. City of BethanyKeaton FoxNo ratings yet

- Oklahoma Known Earthquake FaultsDocument1 pageOklahoma Known Earthquake FaultsKeaton FoxNo ratings yet

- Chesapeake 2nd Quarter 2016Document25 pagesChesapeake 2nd Quarter 2016Keaton FoxNo ratings yet

- Luther/Wellston OCC GuidanceDocument7 pagesLuther/Wellston OCC GuidanceKeaton FoxNo ratings yet

- 2016 OSSBA Teacher Shortage ReportDocument9 pages2016 OSSBA Teacher Shortage ReportKeaton FoxNo ratings yet

- Norman Depot Text FileDocument2 pagesNorman Depot Text FileKeaton FoxNo ratings yet

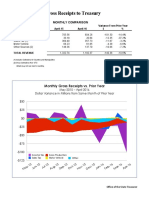

- GRT Aug 2016 ChartsDocument3 pagesGRT Aug 2016 ChartsKeaton FoxNo ratings yet

- Fort Stockton v. SandridgeDocument20 pagesFort Stockton v. SandridgeKeaton FoxNo ratings yet

- GRT Jul 2016 ChartsDocument3 pagesGRT Jul 2016 ChartsKeaton FoxNo ratings yet

- 2016-07-12 City Council Conference PacketDocument76 pages2016-07-12 City Council Conference PacketKeaton FoxNo ratings yet

- Fallin Exec Order DronesDocument1 pageFallin Exec Order DronesKeaton FoxNo ratings yet

- Ok 2016 Incentive ListDocument16 pagesOk 2016 Incentive ListKeaton FoxNo ratings yet

- Crime in Oklahoma, 2015Document143 pagesCrime in Oklahoma, 2015Keaton FoxNo ratings yet

- Court of Appeals in Stuteville V PridexDocument45 pagesCourt of Appeals in Stuteville V PridexKeaton FoxNo ratings yet

- FBI Documents On Joel Henry Hinrichs, IIIDocument37 pagesFBI Documents On Joel Henry Hinrichs, IIIKeaton Fox100% (1)

- Norman Stormwater ProposalDocument8 pagesNorman Stormwater ProposalKeaton FoxNo ratings yet

- HB2931 EnrDocument4 pagesHB2931 EnrKeaton FoxNo ratings yet

- HB2599 EnrDocument5 pagesHB2599 EnrKeaton FoxNo ratings yet

- Norman Police Report On Akolda ManyangDocument1 pageNorman Police Report On Akolda ManyangKeaton FoxNo ratings yet

- Duggan v. One Gas, Inc.Document3 pagesDuggan v. One Gas, Inc.Keaton FoxNo ratings yet

- HB3167 EnrDocument7 pagesHB3167 EnrKeaton FoxNo ratings yet

- Agenda May 9 2016Document2 pagesAgenda May 9 2016Keaton FoxNo ratings yet

- GRT April 2016 ChartsDocument3 pagesGRT April 2016 ChartsKeaton FoxNo ratings yet

- AGENDA Special May 9 2016Document1 pageAGENDA Special May 9 2016Keaton FoxNo ratings yet

- Oklahoma Unemployment March 2016Document5 pagesOklahoma Unemployment March 2016Keaton FoxNo ratings yet

- Norman "Destin Landing" PUD NarrativeDocument39 pagesNorman "Destin Landing" PUD NarrativeKeaton FoxNo ratings yet

- 2021 Edelman Trust Barometer Press ReleaseDocument3 pages2021 Edelman Trust Barometer Press ReleaseMuhammad IkhsanNo ratings yet

- DX DiagDocument31 pagesDX DiagJose Trix CamposNo ratings yet

- Accor vs Airbnb: Business Models in Digital EconomyDocument4 pagesAccor vs Airbnb: Business Models in Digital EconomyAkash PayunNo ratings yet

- Appendix 9A: Standard Specifications For Electrical DesignDocument5 pagesAppendix 9A: Standard Specifications For Electrical Designzaheer ahamedNo ratings yet

- Detect Single-Phase Issues with Negative Sequence RelayDocument7 pagesDetect Single-Phase Issues with Negative Sequence RelayluhusapaNo ratings yet

- Delem: Installation Manual V3Document73 pagesDelem: Installation Manual V3Marcus ChuaNo ratings yet

- March 29, 2013 Strathmore TimesDocument31 pagesMarch 29, 2013 Strathmore TimesStrathmore TimesNo ratings yet

- Keys and Couplings: Definitions and Useful InformationDocument10 pagesKeys and Couplings: Definitions and Useful InformationRobert Michael CorpusNo ratings yet

- Ex 1-3 Without OutputDocument12 pagesEx 1-3 Without OutputKoushikNo ratings yet

- How To Google Like A Pro-10 Tips For More Effective GooglingDocument10 pagesHow To Google Like A Pro-10 Tips For More Effective GooglingMinh Dang HoangNo ratings yet

- G.R. No. 122039 May 31, 2000 VICENTE CALALAS, Petitioner, Court of Appeals, Eliza Jujeurche Sunga and Francisco Salva, RespondentsDocument56 pagesG.R. No. 122039 May 31, 2000 VICENTE CALALAS, Petitioner, Court of Appeals, Eliza Jujeurche Sunga and Francisco Salva, RespondentsJayson AbabaNo ratings yet

- New Markets For Smallholders in India - Exclusion, Policy and Mechanisms Author(s) - SUKHPAL SINGHDocument11 pagesNew Markets For Smallholders in India - Exclusion, Policy and Mechanisms Author(s) - SUKHPAL SINGHRegNo ratings yet

- 231025+ +JBS+3Q23+Earnings+Preview VFDocument3 pages231025+ +JBS+3Q23+Earnings+Preview VFgicokobayashiNo ratings yet

- Csit 101 Assignment1Document3 pagesCsit 101 Assignment1api-266677293No ratings yet

- Market & Industry Analysis CheckDocument2 pagesMarket & Industry Analysis CheckAndhika FarrasNo ratings yet

- Power Steering Rack Components and Auto Suppliers Reference GuideDocument12 pagesPower Steering Rack Components and Auto Suppliers Reference GuideJonathan JoelNo ratings yet

- CCW Armored Composite OMNICABLEDocument2 pagesCCW Armored Composite OMNICABLELuis DGNo ratings yet

- Finesse Service ManualDocument34 pagesFinesse Service ManualLuis Sivira100% (1)

- Online and Payment SecurityDocument14 pagesOnline and Payment SecurityVanezz UchihaNo ratings yet

- BS 00011-2015Document24 pagesBS 00011-2015fazyroshan100% (1)

- Papi AdbDocument50 pagesPapi AdbSilvio Figueiredo0% (1)

- Gustilo Vs Gustilo IIIDocument1 pageGustilo Vs Gustilo IIIMoon BeamsNo ratings yet

- Auditing For Managers - The Ultimate Risk Management ToolDocument369 pagesAuditing For Managers - The Ultimate Risk Management ToolJason SpringerNo ratings yet

- Machine Problem 6 Securing Cloud Services in The IoTDocument4 pagesMachine Problem 6 Securing Cloud Services in The IoTJohn Karlo KinkitoNo ratings yet

- Superelement Modeling-Based Dynamic Analysis of Vehicle Body StructuresDocument7 pagesSuperelement Modeling-Based Dynamic Analysis of Vehicle Body StructuresDavid C HouserNo ratings yet

- Cryptography Seminar - Types, Algorithms & AttacksDocument18 pagesCryptography Seminar - Types, Algorithms & AttacksHari HaranNo ratings yet

- Soft SkillsDocument117 pagesSoft Skillskiran100% (1)

- Brochure of H1 Series Compact InverterDocument10 pagesBrochure of H1 Series Compact InverterEnzo LizziNo ratings yet

- Tutorial 2 EOPDocument3 pagesTutorial 2 EOPammarNo ratings yet

- MockupDocument1 pageMockupJonathan Parra100% (1)