You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Hardsurface Modeling Blender PDFDocument1 pageHardsurface Modeling Blender PDFNoMoreNo ratings yet

- Standard Notes To Form No. 3CD (Revised 2019) CleanDocument8 pagesStandard Notes To Form No. 3CD (Revised 2019) CleanRahul LaddhaNo ratings yet

- Marina™ SID - SRB OASDocument2 pagesMarina™ SID - SRB OASCANSIO IBATANNo ratings yet

- Vamsi Krishna Velaga - ITDocument1 pageVamsi Krishna Velaga - ITvamsiNo ratings yet

- CRC-ACE Income TaxationDocument127 pagesCRC-ACE Income TaxationMark Christian Cutanda VillapandoNo ratings yet

- Multiples Choice Questions With AnswersDocument60 pagesMultiples Choice Questions With AnswersVaibhav Rusia100% (2)

- Innoprint Inti Perkasa, PT - PO00122117Document1 pageInnoprint Inti Perkasa, PT - PO00122117mario gultomNo ratings yet

- Invoice PDFDocument1 pageInvoice PDFbiswaNo ratings yet

- Payment and Settlement Systems Act 2007Document20 pagesPayment and Settlement Systems Act 2007atulsohan6453No ratings yet

- BIR Transfer of SharesDocument8 pagesBIR Transfer of Sharesjaddls100% (1)

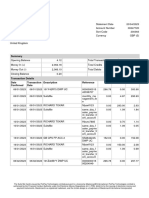

- Account StatementDocument10 pagesAccount StatementVinod KumarNo ratings yet

- PM Reyes Notes On Taxation Ii: Local Taxation: 1. General Principles, Definitions, and LimitationsDocument9 pagesPM Reyes Notes On Taxation Ii: Local Taxation: 1. General Principles, Definitions, and LimitationsMich FelloneNo ratings yet

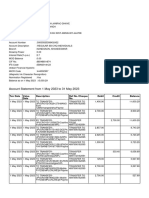

- Account Statement From 1 May 2023 To 31 May 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument10 pagesAccount Statement From 1 May 2023 To 31 May 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit Balanceavinashdeshmukh7027No ratings yet

- Monopoly Deed Cards PDFDocument12 pagesMonopoly Deed Cards PDFErfanNo ratings yet

- Unit 5 Financial Planning and Tax ManagementDocument18 pagesUnit 5 Financial Planning and Tax ManagementnoroNo ratings yet

- Brent Sept 13 - Radisson Blu Hotel, Hamburg AirportDocument2 pagesBrent Sept 13 - Radisson Blu Hotel, Hamburg Airportvaibhav rockingNo ratings yet

- Launch Jasper ReportDocument2 pagesLaunch Jasper ReportZelalem RegasaNo ratings yet

- cs11-2021 (AIDC)Document2 pagescs11-2021 (AIDC)Vogue LogisticsNo ratings yet

- Indebtedness Assumed Exceeds Tax Basis of Property SoldDocument3 pagesIndebtedness Assumed Exceeds Tax Basis of Property SoldJemalyn De Guzman TuringanNo ratings yet

- Butterfly Rapid 750 W Juicer Mixer Grinder (4 Jars, Black) : Grand Total 2464.00Document1 pageButterfly Rapid 750 W Juicer Mixer Grinder (4 Jars, Black) : Grand Total 2464.00Abhijit Kumar SinghNo ratings yet

- Megerle Custom Cabinet Co Uses The Job Order Cost SystemDocument3 pagesMegerle Custom Cabinet Co Uses The Job Order Cost SystemAmit Pandey0% (1)

- Transfer PricingDocument98 pagesTransfer PricingMAHESH JAINNo ratings yet

- Form 16 PDFDocument3 pagesForm 16 PDFkk_mishaNo ratings yet

- Statement 2023 01 06 2023 04 20Document2 pagesStatement 2023 01 06 2023 04 20Avtar SNo ratings yet

- Report TransactionsretyrDocument5 pagesReport TransactionsretyrPitirut Anca DanielaNo ratings yet

- SPIT Abella SamplexDocument5 pagesSPIT Abella SamplexJasperAllenBarrientosNo ratings yet

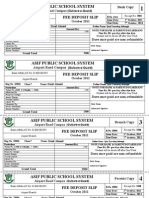

- Asif Public School System: Fee Deposit SlipDocument1 pageAsif Public School System: Fee Deposit SlipIrfan YousafNo ratings yet

- Sold By: Tech-Connect Retail Private Limited, Invoice NumberDocument2 pagesSold By: Tech-Connect Retail Private Limited, Invoice NumberanvithaNo ratings yet

- PDF - ChallanList - 10 - 7 - 2021 12 - 00 - 00 AMDocument1 pagePDF - ChallanList - 10 - 7 - 2021 12 - 00 - 00 AM11 R N Roshikha 9 CNo ratings yet