You might also like

- Principles of Group Accounting under IFRSFrom EverandPrinciples of Group Accounting under IFRSRating: 3 out of 5 stars3/5 (1)

- To the Moon Investing: Visually Mapping Your Winning Stock Market PortfolioFrom EverandTo the Moon Investing: Visually Mapping Your Winning Stock Market PortfolioNo ratings yet

- SamigroupDocument9 pagesSamigroupsamidan tubeNo ratings yet

- Budget Format Sales Budget: Cash Collection Total Budgeted SalesDocument6 pagesBudget Format Sales Budget: Cash Collection Total Budgeted Salessernhaow_658673991No ratings yet

- LEVEL 2 Online Quiz - Questions SET ADocument8 pagesLEVEL 2 Online Quiz - Questions SET AVincent Larrie MoldezNo ratings yet

- 4th Assessment STUDENTDocument5 pages4th Assessment STUDENTJOHANNA TORRESNo ratings yet

- Worksheet Master BudgetDocument6 pagesWorksheet Master BudgetRUPIKA R GNo ratings yet

- FINANCIAL MANAGEMENT Assignment 2Document14 pagesFINANCIAL MANAGEMENT Assignment 2dangerous saifNo ratings yet

- Financials of StartupDocument31 pagesFinancials of StartupJanine PadillaNo ratings yet

- Write Down of Inventory To Net Realizable Value3Document4 pagesWrite Down of Inventory To Net Realizable Value3CJ alandy100% (1)

- Supershop Fianal For Balance SheetDocument21 pagesSupershop Fianal For Balance SheetMohammad Osman GoniNo ratings yet

- Example Revised FsDocument17 pagesExample Revised FsJoseph pardillaNo ratings yet

- Class 4 QuestionsDocument24 pagesClass 4 QuestionsKeylia SeniorkklooNo ratings yet

- Material Budget (RS.)Document6 pagesMaterial Budget (RS.)James WisleyNo ratings yet

- Budget and Budgetary ControlDocument8 pagesBudget and Budgetary ControlShadrack KazunguNo ratings yet

- Penyusutan - Peralatan KantorDocument16 pagesPenyusutan - Peralatan KantorSiti Hajar AsmawiahNo ratings yet

- TUTORIAL 8 BudgetDocument7 pagesTUTORIAL 8 Budgetsarahayeesha1No ratings yet

- Group Assignment Business Valuation and AnalysisDocument8 pagesGroup Assignment Business Valuation and Analysischarlesmicky82No ratings yet

- Presentation On Variable and Absorption CostingDocument24 pagesPresentation On Variable and Absorption Costingsmurtazaali84No ratings yet

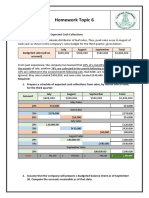

- Homework Topic 6: EXERCISE 8-1 Schedule of Expected Cash CollectionsDocument3 pagesHomework Topic 6: EXERCISE 8-1 Schedule of Expected Cash CollectionskhetamNo ratings yet

- Chapter 13Document11 pagesChapter 13Christine GorospeNo ratings yet

- Manufacturing Company BudgetingDocument10 pagesManufacturing Company BudgetingSajakul SornNo ratings yet

- Master BudgetDocument12 pagesMaster Budgetshi shiiisshhNo ratings yet

- Cover MergedDocument8 pagesCover Mergedclient mailsNo ratings yet

- Unit II - Fund Flow & Cash FlowDocument71 pagesUnit II - Fund Flow & Cash FlowParag PardeshiNo ratings yet

- Chapter 9 2Document34 pagesChapter 9 2Genie MaeNo ratings yet

- Auditing Theories and Problems Answer Key Quiz WEEK 2Document9 pagesAuditing Theories and Problems Answer Key Quiz WEEK 2Van MateoNo ratings yet

- Sept 21 ExercisesDocument12 pagesSept 21 ExercisesPeachyNo ratings yet

- SummaryDocument30 pagesSummaryAkira Marantal Valdez0% (1)

- Tahun Penjualan Harga A B C A B: Y (Estimasi PJL)Document3 pagesTahun Penjualan Harga A B C A B: Y (Estimasi PJL)Ratna KurniawatiNo ratings yet

- Budgeting - Planning: A325 Discussion - March 19, 2012Document8 pagesBudgeting - Planning: A325 Discussion - March 19, 2012alfaNo ratings yet

- Statement of CIDocument4 pagesStatement of CIMarvin CaliwaganNo ratings yet

- ProblemsDocument11 pagesProblemsMohamed RefaayNo ratings yet

- Cost Accounting Assignment #2Document5 pagesCost Accounting Assignment #2BRIANNIE ASRI VIVASNo ratings yet

- Magma Minerals Case StudyDocument6 pagesMagma Minerals Case StudyJoyce De LunaNo ratings yet

- Natural WoodworksDocument15 pagesNatural Woodworksenojosa nhoelNo ratings yet

- 44 - Home Assignment - Project ManagementDocument16 pages44 - Home Assignment - Project Managementroshni muthaNo ratings yet

- Tut Mene AccDocument7 pagesTut Mene Accnatasya angelNo ratings yet

- Financial And/or Quantitative Prior Time Policy Objective: What Is A Budget?Document37 pagesFinancial And/or Quantitative Prior Time Policy Objective: What Is A Budget?vilas raneNo ratings yet

- Finance Projection TemplateDocument14 pagesFinance Projection Templatesherli OrienteNo ratings yet

- Boomstick CorpDocument14 pagesBoomstick CorpDivya GoyalNo ratings yet

- Local Media3459558769538041028Document22 pagesLocal Media3459558769538041028Princes Ann MarcianoNo ratings yet

- Assignment 5Document6 pagesAssignment 5Anupama BiswasNo ratings yet

- SHORT-TERM BUDGETING - Review PDFDocument21 pagesSHORT-TERM BUDGETING - Review PDFAngelica Bautista100% (1)

- Ulod. Describe The Budgeting Framework and Develop A Master BudgetDocument3 pagesUlod. Describe The Budgeting Framework and Develop A Master BudgetJeson MalinaoNo ratings yet

- Projection Plan: Description July % August % SeptemberDocument13 pagesProjection Plan: Description July % August % Septemberfurqon irtaNo ratings yet

- Merchandising Hand OutDocument7 pagesMerchandising Hand OutElla Mae SaludoNo ratings yet

- Tugas 5 - InventoryDocument11 pagesTugas 5 - InventoryMuhammad RochimNo ratings yet

- Kitchen Aid Products, Inc., Manufactures Small Kitchen AppliancesDocument7 pagesKitchen Aid Products, Inc., Manufactures Small Kitchen AppliancesGalina FateevaNo ratings yet

- SCM 2ND SemDocument9 pagesSCM 2ND SemRiki AsahiNo ratings yet

- Capital BudgetingDocument14 pagesCapital BudgetingbhaskkarNo ratings yet

- Chapter Two: Master Budget and Responsibility AccountingDocument25 pagesChapter Two: Master Budget and Responsibility Accountingweyn deguNo ratings yet

- Budget For The Coffee House 2Document13 pagesBudget For The Coffee House 2ngochoangbich2004No ratings yet

- Financial PlanDocument12 pagesFinancial PlanMaita100% (1)

- Class Participation 7 Q 1: (3 Marks) : Trout Company Is Considering Introducing A New Line of Pagers Targeting The PreteenDocument5 pagesClass Participation 7 Q 1: (3 Marks) : Trout Company Is Considering Introducing A New Line of Pagers Targeting The Preteenaj singhNo ratings yet

- Straight ProblemDocument3 pagesStraight ProblemAldrin Liwanag89% (9)

- ACCT500 (16) Answers To Seminar 6Document5 pagesACCT500 (16) Answers To Seminar 6rashid rahmanzada100% (1)

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- The New Global Rulers: The Privatization of Regulation in the World EconomyFrom EverandThe New Global Rulers: The Privatization of Regulation in the World EconomyNo ratings yet

- In Search of The Lost FatherDocument11 pagesIn Search of The Lost FatherParamjit SharmaNo ratings yet

- Types of PsychologyDocument62 pagesTypes of PsychologyParamjit SharmaNo ratings yet

- Beating Tough TargetsDocument43 pagesBeating Tough TargetsParamjit SharmaNo ratings yet

- Motivating ManpowerDocument32 pagesMotivating ManpowerParamjit SharmaNo ratings yet

- Excellence in CommitmentDocument43 pagesExcellence in CommitmentParamjit SharmaNo ratings yet

- Selection & Personality TestsDocument70 pagesSelection & Personality TestsParamjit SharmaNo ratings yet

- Few Tips For Job InterviewDocument11 pagesFew Tips For Job InterviewParamjit SharmaNo ratings yet

- Interpersonal RelationshipDocument57 pagesInterpersonal RelationshipParamjit SharmaNo ratings yet

- Strategic Human Resource ManagementDocument27 pagesStrategic Human Resource ManagementParamjit Sharma67% (3)

- Strategic Management ProcessDocument95 pagesStrategic Management ProcessParamjit SharmaNo ratings yet

- Industrial & Business PsychologyDocument58 pagesIndustrial & Business PsychologyParamjit Sharma100% (1)

- Male Female PsychologyDocument38 pagesMale Female PsychologyParamjit SharmaNo ratings yet

- Mapping Competency of ManpowerDocument28 pagesMapping Competency of ManpowerParamjit Sharma100% (1)

- Training & Development StrategiesDocument15 pagesTraining & Development StrategiesParamjit SharmaNo ratings yet

- Shatabdi Express (A Short Story)Document10 pagesShatabdi Express (A Short Story)Paramjit SharmaNo ratings yet

- Strategic Performance ManagementDocument34 pagesStrategic Performance ManagementParamjit SharmaNo ratings yet

- Managing Stress in AdolescentsDocument42 pagesManaging Stress in AdolescentsParamjit SharmaNo ratings yet

- The Tribute (A Short Story)Document9 pagesThe Tribute (A Short Story)Paramjit SharmaNo ratings yet

- Retrenchment Strategies in HRDocument34 pagesRetrenchment Strategies in HRParamjit Sharma88% (8)

- Atonement (A Short Story)Document9 pagesAtonement (A Short Story)Paramjit SharmaNo ratings yet

- Management Control Systems in Services OrganizationDocument17 pagesManagement Control Systems in Services OrganizationParamjit Sharma100% (2)

- Training Dynamics-Using Modern ToolsDocument34 pagesTraining Dynamics-Using Modern ToolsParamjit SharmaNo ratings yet

- Sparkling Spectacles (A Short Story)Document8 pagesSparkling Spectacles (A Short Story)Paramjit SharmaNo ratings yet

- Responsibility CentresDocument25 pagesResponsibility CentresParamjit Sharma100% (2)

- Goals CongruenceDocument23 pagesGoals CongruenceParamjit Sharma100% (1)

- Training of TrainersDocument26 pagesTraining of TrainersParamjit SharmaNo ratings yet

- Management Control Systems: Paramjit SharmaDocument33 pagesManagement Control Systems: Paramjit SharmaParamjit Sharma0% (1)

- Profit CentresDocument8 pagesProfit CentresParamjit SharmaNo ratings yet

- Strategic Financial ManagementDocument16 pagesStrategic Financial ManagementParamjit SharmaNo ratings yet

- Measuring & Controlling Assets EmployedDocument26 pagesMeasuring & Controlling Assets EmployedParamjit SharmaNo ratings yet