You might also like

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- 04b Economic Risk Capital (2011)Document13 pages04b Economic Risk Capital (2011)apluNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Single Name Credit DerivativesDocument32 pagesSingle Name Credit DerivativesapluNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Allowance For Risk in Market Consistent Embedded Value (MCEV)Document12 pagesAllowance For Risk in Market Consistent Embedded Value (MCEV)apluNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- CFO-Forum MCEV Basis For Conclusions April 2016Document40 pagesCFO-Forum MCEV Basis For Conclusions April 2016apluNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Eev Disclosures PDFDocument6 pagesEev Disclosures PDFapluNo ratings yet

- ForecastingPortfolioVaR 02Document42 pagesForecastingPortfolioVaR 02apluNo ratings yet

- CFO-Forum EEV Principles and Guidance April 2016Document22 pagesCFO-Forum EEV Principles and Guidance April 2016apluNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Bank Liquidity Policy StatementDocument19 pagesBank Liquidity Policy StatementapluNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Liquidity Risk ALM Policy - ALCODocument28 pagesLiquidity Risk ALM Policy - ALCOaplu100% (1)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- CFO-Forum MCEV Principles and Guidance April 2016Document31 pagesCFO-Forum MCEV Principles and Guidance April 2016apluNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- A Bond Market Primer For New IssuersDocument4 pagesA Bond Market Primer For New IssuersapluNo ratings yet

- Incorporating Liquidity Risk Into Funds Transfer PricingDocument30 pagesIncorporating Liquidity Risk Into Funds Transfer PricingapluNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- TAS Data Transfer Files SpecsDocument55 pagesTAS Data Transfer Files SpecsapluNo ratings yet

- Assets & Liabilities Management AT The Union Co-Operative Bank LTDDocument21 pagesAssets & Liabilities Management AT The Union Co-Operative Bank LTDapluNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- TKM CH 18Document103 pagesTKM CH 18apluNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Locking The BoxDocument1 pageLocking The BoxapluNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Pros and Cons of EVA 013-08Document6 pagesPros and Cons of EVA 013-08apluNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Mamis Last LetterDocument10 pagesMamis Last LetterTBP_Think_Tank100% (3)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- UntitledDocument3 pagesUntitledapi-234474152No ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- RE 01 11 Pre Sold Condo Units SolutionsDocument5 pagesRE 01 11 Pre Sold Condo Units SolutionsAnonymous bf1cFDuepPNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Transfer Pricing II: Rajan Baa 3257Document15 pagesTransfer Pricing II: Rajan Baa 3257Rajan BaaNo ratings yet

- South Asia TechDocument6 pagesSouth Asia TechA M FaisalNo ratings yet

- CISI Exam Booking Instructions-1Document4 pagesCISI Exam Booking Instructions-1simon.dk.designerNo ratings yet

- Relevance of Questions From Past Level III Essay Exams: Use IFT Prep To Ace The Level III ExamDocument3 pagesRelevance of Questions From Past Level III Essay Exams: Use IFT Prep To Ace The Level III ExamHasan KhanNo ratings yet

- Engineering Economy1Document13 pagesEngineering Economy1Roselyn MatienzoNo ratings yet

- Beauhurst Crowdfunding Index Q1 2017Document5 pagesBeauhurst Crowdfunding Index Q1 2017CrowdfundInsiderNo ratings yet

- Audit of Property, Plant and Equipment: Auditing ProblemsDocument5 pagesAudit of Property, Plant and Equipment: Auditing ProblemsLei PangilinanNo ratings yet

- UPSA 2019 Tutorial Questions Fs WITH ANSWERSDocument14 pagesUPSA 2019 Tutorial Questions Fs WITH ANSWERSLaud ListowellNo ratings yet

- Solutions For End-of-Chapter Questions and Problems: Chapter TenDocument29 pagesSolutions For End-of-Chapter Questions and Problems: Chapter Tenester jofreyNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- InstaSummary Report of Mantra Softech (India) Private Limited - 30-06-2020Document10 pagesInstaSummary Report of Mantra Softech (India) Private Limited - 30-06-2020RajiNo ratings yet

- Welcome To Momentum Trading SetupDocument12 pagesWelcome To Momentum Trading SetupSunny Deshmukh0% (1)

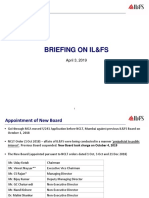

- ILFS Briefing (April 2019)Document15 pagesILFS Briefing (April 2019)Richard DierdreNo ratings yet

- Akuntansi 11Document3 pagesAkuntansi 11Zhida PratamaNo ratings yet

- HDFC Amc PDFDocument8 pagesHDFC Amc PDFRahul JaiswalNo ratings yet

- EPF Circular On Pension For Full Salary 23.3.17Document11 pagesEPF Circular On Pension For Full Salary 23.3.17Vishal IngleNo ratings yet

- Dispute FormDocument1 pageDispute Formuzair muhdNo ratings yet

- Week 012-Presentation Key Concepts of Simple and Compound Interests, and Simple and General Annuities - Part 002Document18 pagesWeek 012-Presentation Key Concepts of Simple and Compound Interests, and Simple and General Annuities - Part 002Alleona EmbolodeNo ratings yet

- A 2021MBA010 NiraliOswal Case Scenarios RBCDocument3 pagesA 2021MBA010 NiraliOswal Case Scenarios RBCmohammedsuhaim abdul gafoorNo ratings yet

- NIB Annual Report 2015Document216 pagesNIB Annual Report 2015Asif RafiNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- IA2 Chapter 20 ActivitiesDocument13 pagesIA2 Chapter 20 ActivitiesShaina TorraineNo ratings yet

- Exam 1 - Econ 380 - Fall 2016 - KEYDocument4 pagesExam 1 - Econ 380 - Fall 2016 - KEYAlexNo ratings yet

- Pifra Business Finance ProjectDocument17 pagesPifra Business Finance ProjectWaqas AhmedNo ratings yet

- CV Rudi Pasaribu UpdateDocument5 pagesCV Rudi Pasaribu UpdateDitto Dwi PurnamaNo ratings yet

- CH 08Document51 pagesCH 08Daniel NababanNo ratings yet

- Annuity DueDocument2 pagesAnnuity DueJsbebe jskdbsj50% (2)

- Business Plan For FloristDocument26 pagesBusiness Plan For Floristmohammed hajiademNo ratings yet

- NEW DT Bullet (MCQ'S) by CA Saumil Manglani - CS Exec June 22 & Dec 22 ExamsDocument168 pagesNEW DT Bullet (MCQ'S) by CA Saumil Manglani - CS Exec June 22 & Dec 22 ExamsAkash MalikNo ratings yet

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 4.5 out of 5 stars4.5/5 (14)

- John D. Rockefeller on Making Money: Advice and Words of Wisdom on Building and Sharing WealthFrom EverandJohn D. Rockefeller on Making Money: Advice and Words of Wisdom on Building and Sharing WealthRating: 4 out of 5 stars4/5 (20)