You might also like

- A Study ON "Working Capital Management" AT Sterlite Technologies LTDDocument55 pagesA Study ON "Working Capital Management" AT Sterlite Technologies LTDZankhana PatelNo ratings yet

- Analysis of Financial StatementsDocument18 pagesAnalysis of Financial StatementsEasymoney Usting100% (1)

- Financial and Managerial Accounting For Mbas 4th Edition Easton Test Bank 191001163059Document32 pagesFinancial and Managerial Accounting For Mbas 4th Edition Easton Test Bank 191001163059josh100% (1)

- THESISDocument56 pagesTHESISbless erika lendroNo ratings yet

- Chapter 5Document37 pagesChapter 5Sherlyn MamacNo ratings yet

- Ar 2011Document112 pagesAr 2011centaurus553587No ratings yet

- Annual Report 2011Document127 pagesAnnual Report 2011Nooreza PeerooNo ratings yet

- Proposed Divestment of 9 Bukit Batok Street 22Document3 pagesProposed Divestment of 9 Bukit Batok Street 22JoshKernNo ratings yet

- Makalah Tentang Asset (Bahasa Inggris)Document5 pagesMakalah Tentang Asset (Bahasa Inggris)Ilham Sukron100% (1)

- A Study On The Financial and Operational Efficiency of Sakthi Finance LimitedDocument88 pagesA Study On The Financial and Operational Efficiency of Sakthi Finance LimitedmaheswariNo ratings yet

- Alset International LimitedDocument13 pagesAlset International LimitedSieng MenghongNo ratings yet

- 顺丰控股:2018年年度报告(英文版) PDFDocument281 pages顺丰控股:2018年年度报告(英文版) PDFHoward DalioNo ratings yet

- Executive Summary ReportDocument26 pagesExecutive Summary Reportsharan ChowdaryNo ratings yet

- CMT Ar 2008Document176 pagesCMT Ar 2008Sassy TanNo ratings yet

- Lion Asiapac Limited: A Wright Investors' Service Research ReportDocument44 pagesLion Asiapac Limited: A Wright Investors' Service Research Reportinsideout123No ratings yet

- Angel Broking ProjectDocument35 pagesAngel Broking ProjectAnand VyasNo ratings yet

- Wealth Management ReportDocument41 pagesWealth Management Reportagrawal.ace9114No ratings yet

- Financial Statement Analysis of Ashok Leyland Limited, IndiaDocument9 pagesFinancial Statement Analysis of Ashok Leyland Limited, IndiaShubham NamdevNo ratings yet

- Annual Report 2010-11 APILDocument140 pagesAnnual Report 2010-11 APILraju4444No ratings yet

- A Synopsis On: Submitted To: Submitted byDocument6 pagesA Synopsis On: Submitted To: Submitted byHimanshu BhutnaNo ratings yet

- Fundamental Analysis of Iron and Steel Industry and Tata Steel (Indiabulls) ...Document77 pagesFundamental Analysis of Iron and Steel Industry and Tata Steel (Indiabulls) ...chao sherpa100% (1)

- Religare Asset Management: June 2012Document37 pagesReligare Asset Management: June 2012Navjyotsingh JagirdarNo ratings yet

- Equity ResearchDocument84 pagesEquity Researchtulasinad123100% (1)

- Factor InvestingDocument16 pagesFactor InvestingRicardo BregaldaNo ratings yet

- Portfolio ManagementDocument43 pagesPortfolio ManagementNiket DattaniNo ratings yet

- Vypracované Témy Na Odbornú Skúšku Z Cudzieho Jazyka - Anglický JazykDocument25 pagesVypracované Témy Na Odbornú Skúšku Z Cudzieho Jazyka - Anglický Jazykvo559emNo ratings yet

- Fortune 2010Document138 pagesFortune 2010Bryan LiNo ratings yet

- AppleDocument75 pagesAppleAbhisek MohantyNo ratings yet

- SPC ArticleDocument3 pagesSPC ArticleThanapoom BoonipatNo ratings yet

- Financial Statement Analysis 2019Document28 pagesFinancial Statement Analysis 2019ALPASLAN TOKERNo ratings yet

- SIFMA Insights:: US Equity Capital Formation PrimerDocument47 pagesSIFMA Insights:: US Equity Capital Formation PrimermayorladNo ratings yet

- Pakistan's First Successful Launch of A Real Estate Investment Trust-Dolmen City (REIT) - (Shariah Compliant Rental REIT Scheme)Document18 pagesPakistan's First Successful Launch of A Real Estate Investment Trust-Dolmen City (REIT) - (Shariah Compliant Rental REIT Scheme)waqar mansoorNo ratings yet

- Op Ales Que Singapore RoundtableDocument25 pagesOp Ales Que Singapore RoundtableOpalesque PublicationsNo ratings yet

- Market Outlook 28th December 2011Document4 pagesMarket Outlook 28th December 2011Angel BrokingNo ratings yet

- Austrade - Investment Management Industry in AustraliaDocument47 pagesAustrade - Investment Management Industry in Australiappt46No ratings yet

- Rea Group Ltd. ReportDocument8 pagesRea Group Ltd. ReportAnkit BhattraiNo ratings yet

- FADocument46 pagesFANishant JainNo ratings yet

- TCS 2010 AnalysisDocument22 pagesTCS 2010 AnalysisDilip KumarNo ratings yet

- Accounting PrincipleDocument22 pagesAccounting PrincipleCrystalPingNo ratings yet

- Strategic Business Reporting - UIA20502J: Unit 3Document22 pagesStrategic Business Reporting - UIA20502J: Unit 3MohanrajNo ratings yet

- Thesis Ratio AnalysisDocument8 pagesThesis Ratio Analysisclaudiabrowndurham100% (2)

- Stanlib Fahari I-Reit Note 04112015 PDFDocument3 pagesStanlib Fahari I-Reit Note 04112015 PDFGeorgeNo ratings yet

- Investment Management Industry in AustraliaDocument48 pagesInvestment Management Industry in AustraliaStephen John-Michael EmmanuelNo ratings yet

- International Financial ManagementDocument20 pagesInternational Financial ManagementKnt Nallasamy GounderNo ratings yet

- Real Estate Investment Trust (Reit)Document15 pagesReal Estate Investment Trust (Reit)Norain Md TarmiziNo ratings yet

- Ascend Hedge Fund Investment Due Diligence Report 0811redactedDocument17 pagesAscend Hedge Fund Investment Due Diligence Report 0811redactedJoshua ElkingtonNo ratings yet

- RenataDocument48 pagesRenataTheAgents107No ratings yet

- Apex Tannery Limited: Submitted To: Md. Hashibul HassanDocument18 pagesApex Tannery Limited: Submitted To: Md. Hashibul Hassananon_294717796No ratings yet

- Introduction To Financial Statements - Views On News From EquitymasterDocument4 pagesIntroduction To Financial Statements - Views On News From EquitymasterPrakash JoshiNo ratings yet

- Assignment 2: Company Name: Tata Consultancy ServicesDocument15 pagesAssignment 2: Company Name: Tata Consultancy ServicesPooja talrejaNo ratings yet

- Spice Jet Consultancy ReportDocument27 pagesSpice Jet Consultancy ReportNitin Lahoti100% (1)

- Finibrain Sip ReportDocument36 pagesFinibrain Sip Reportaruna puppalaNo ratings yet

- Financial Analysis of Singer (Sri Lanka) PLC For The Financial Years From 2012-2016Document22 pagesFinancial Analysis of Singer (Sri Lanka) PLC For The Financial Years From 2012-2016Shyamila RathnayakaNo ratings yet

- Original Research Paper Commerce: A Study On Financial Performance Analysis of Indian Tobacco Corporation LimitedDocument4 pagesOriginal Research Paper Commerce: A Study On Financial Performance Analysis of Indian Tobacco Corporation Limitedemmanual cheeranNo ratings yet

- A Project Report On Ratio Analysis at Il&Fs Invest Smart Mba Project FinanceDocument88 pagesA Project Report On Ratio Analysis at Il&Fs Invest Smart Mba Project Financesatish pawarNo ratings yet

- Finance ProjectDocument58 pagesFinance ProjectVijaya ThoratNo ratings yet

- Draft Treasury & Investment Manual of AsasahDocument39 pagesDraft Treasury & Investment Manual of AsasahMuhammad MinhajNo ratings yet

- A Project Report On Analysis of Stock Price Movement at ANAGRAM STOCK BROKING LTDDocument60 pagesA Project Report On Analysis of Stock Price Movement at ANAGRAM STOCK BROKING LTDBabasab Patil (Karrisatte)0% (1)

- Market Outlook 4th January 2012Document3 pagesMarket Outlook 4th January 2012Angel BrokingNo ratings yet

- Kotak International REIT FOF: India's First Global REIT Fund of FundDocument27 pagesKotak International REIT FOF: India's First Global REIT Fund of FundVinit ShahNo ratings yet

- Determinant Factors of Profitability in Malaysia's Real Estate Investment Trusts (M-REITS)Document14 pagesDeterminant Factors of Profitability in Malaysia's Real Estate Investment Trusts (M-REITS)LeeZhenXiangNo ratings yet

- Associated British FoodsDocument16 pagesAssociated British FoodsMohd Shahbaz Husain100% (1)

- Guide to Management Accounting Inventory turnover for managersFrom EverandGuide to Management Accounting Inventory turnover for managersNo ratings yet

- Rss02 LeadDocument6 pagesRss02 Leadhi_chrisleeNo ratings yet

- RSS01 LearnDocument3 pagesRSS01 Learnhi_chrisleeNo ratings yet

- 3 Powerful Stock Strategies For BeginnersDocument11 pages3 Powerful Stock Strategies For Beginnershi_chrislee100% (2)

- Tapping Into Ultimate Success by Jack Canfield and Pamela Bruner ExcerptDocument35 pagesTapping Into Ultimate Success by Jack Canfield and Pamela Bruner Excerpthi_chrislee75% (8)

- Army Institute of Business Administration (AIBA) : Term Paper OnDocument30 pagesArmy Institute of Business Administration (AIBA) : Term Paper OnFahimNo ratings yet

- Abbott Laboratories (ABT)Document8 pagesAbbott Laboratories (ABT)Riffat Al ImamNo ratings yet

- Profitability Ratios: Strategic Financial Management - SFM (S5) Topic: Financial Ratio AnalysisDocument8 pagesProfitability Ratios: Strategic Financial Management - SFM (S5) Topic: Financial Ratio AnalysisAhmed RazaNo ratings yet

- Value Based ManagementDocument9 pagesValue Based ManagementSivaSankarKatariNo ratings yet

- HGHGKJDocument66 pagesHGHGKJHuyenDaoNo ratings yet

- Financial Analysis Services For Small and Mid-Sized CompaniesDocument4 pagesFinancial Analysis Services For Small and Mid-Sized Companiesbarakkat72No ratings yet

- Fin433 ReportDocument30 pagesFin433 ReportShàhríàrõ Dã Ràkínskì100% (1)

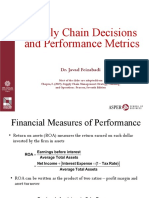

- 3-Supply Chain Decisions and Performance Metrics (A)Document21 pages3-Supply Chain Decisions and Performance Metrics (A)eeman kNo ratings yet

- Foreign Exchange Activities of Exim Bank of Bangladesh LTDDocument40 pagesForeign Exchange Activities of Exim Bank of Bangladesh LTDNeamul Nis100% (1)

- Ankit Gupta Pgma2009 Asingment2Document39 pagesAnkit Gupta Pgma2009 Asingment2ANKIT GUPTANo ratings yet

- RCDC SWOT Analysis - Tech Manufacturing FirmsDocument6 pagesRCDC SWOT Analysis - Tech Manufacturing FirmsPaul Michael AngeloNo ratings yet

- KeppelT&T - 2010 Annual ReportDocument144 pagesKeppelT&T - 2010 Annual ReportDaxx83No ratings yet

- Factors Affecting Bank Profitability in IndonesiaDocument7 pagesFactors Affecting Bank Profitability in IndonesiaArdi GunardiNo ratings yet

- Radio AnalysisDocument100 pagesRadio Analysisabhayjain686No ratings yet

- Aquarium Services Business PlanDocument30 pagesAquarium Services Business PlanZuzani MathiyaNo ratings yet

- Chapter 4 Financial Statement AnalysisDocument54 pagesChapter 4 Financial Statement AnalysisDemelash Agegnhu BeleteNo ratings yet

- FABM Week 6 - Financial RatioDocument35 pagesFABM Week 6 - Financial Ratiovmin친구No ratings yet

- Ashok Leyland Valuation - ReportDocument17 pagesAshok Leyland Valuation - Reportbharath_ndNo ratings yet

- Quick RatioDocument15 pagesQuick RatioAin roseNo ratings yet

- My Trading StrategyDocument2 pagesMy Trading StrategypradeephdNo ratings yet

- CH03 TQ HW 7eDocument26 pagesCH03 TQ HW 7eAnbang Xiao100% (2)

- Forecasting Unbalanced Balance SheetsDocument8 pagesForecasting Unbalanced Balance SheetsSiddhu SaiNo ratings yet

- Fsa 2012 16Document190 pagesFsa 2012 16Muhammad Shahzad IjazNo ratings yet

- Fundamental Analysis of PNB Ltd.Document19 pagesFundamental Analysis of PNB Ltd.Ashutosh Gupta100% (1)

- FM Revision - MaterialDocument217 pagesFM Revision - MaterialSri HariniNo ratings yet

- Uts Manajemen KeuanganDocument8 pagesUts Manajemen KeuangantntAgstNo ratings yet

- Analysis of The Loan Provided by Citizen Bank Limited: A Project Work ReportDocument34 pagesAnalysis of The Loan Provided by Citizen Bank Limited: A Project Work ReportHem Raj JoshiNo ratings yet