You might also like

- Foundational Theories and Techniques for Risk Management, A Guide for Professional Risk Managers in Financial Services - Part II - Financial InstrumentsFrom EverandFoundational Theories and Techniques for Risk Management, A Guide for Professional Risk Managers in Financial Services - Part II - Financial InstrumentsNo ratings yet

- Solutions of Money, Banking and The Financial SystemDocument105 pagesSolutions of Money, Banking and The Financial Systemscribd50% (2)

- Multinational Business Finance 12th Edition Slides Chapter 07Document38 pagesMultinational Business Finance 12th Edition Slides Chapter 07Alli Tobba100% (1)

- Introducing ESPRIDocument16 pagesIntroducing ESPRImbfinalbluesNo ratings yet

- Bonds With Embedded OptionsDocument9 pagesBonds With Embedded OptionsSajib KarNo ratings yet

- FEDEX Swot AnalysisDocument10 pagesFEDEX Swot AnalysisSidra ShaukatNo ratings yet

- Example of A Representation LetterDocument8 pagesExample of A Representation LetterPradhikta RumbagaNo ratings yet

- Currency and Interest Rate Swaps: Chapter TenDocument22 pagesCurrency and Interest Rate Swaps: Chapter TenEvan SwagerNo ratings yet

- Swaps: Chapter SixDocument25 pagesSwaps: Chapter SixPavithra GowthamNo ratings yet

- Interest Rate and Currency SwapsDocument33 pagesInterest Rate and Currency SwapsMatt ToothacreNo ratings yet

- Unit 8 Currency SwapsDocument10 pagesUnit 8 Currency Swapsne002No ratings yet

- Multinational Business Finance 12th Edition Slides Chapter 06Document38 pagesMultinational Business Finance 12th Edition Slides Chapter 06Alli Tobba100% (1)

- Interest Rate SwapsDocument12 pagesInterest Rate SwapsChris Armour100% (1)

- Fixed Income (Debt) Securities: Source: CFA IF Chapter 9 (Coverage of CH 9 Is MUST For Students)Document17 pagesFixed Income (Debt) Securities: Source: CFA IF Chapter 9 (Coverage of CH 9 Is MUST For Students)Oona NiallNo ratings yet

- Section 3 - SwapsDocument49 pagesSection 3 - SwapsEric FahertyNo ratings yet

- Derivatives Individual AssignmentDocument24 pagesDerivatives Individual AssignmentCarine TeeNo ratings yet

- CH 07 Hull Fundamentals 8 The DDocument47 pagesCH 07 Hull Fundamentals 8 The DjlosamNo ratings yet

- CDS Presentation With References PDFDocument42 pagesCDS Presentation With References PDF2401824No ratings yet

- Duration PDFDocument8 pagesDuration PDFMohammad Khaled Saifullah CdcsNo ratings yet

- Week 3 - Ch8 - Interest Rate Risk - The Repricing ModelDocument12 pagesWeek 3 - Ch8 - Interest Rate Risk - The Repricing ModelAlana Cunningham100% (1)

- Bond Value - YieldDocument40 pagesBond Value - YieldSheeza AshrafNo ratings yet

- Stock ValuvationDocument30 pagesStock ValuvationmsumanraoNo ratings yet

- Equity Forward ContractDocument6 pagesEquity Forward Contractbloomberg1234No ratings yet

- DerivativesDocument19 pagesDerivativesSangram BhoiteNo ratings yet

- Chapter 3-Hedging Strategies Using Futures-29.01.2014Document26 pagesChapter 3-Hedging Strategies Using Futures-29.01.2014abaig2011No ratings yet

- Determination of Forward and Futures PricesDocument23 pagesDetermination of Forward and Futures PricesKira D. PortgasNo ratings yet

- Derivatives and Risk ManagementDocument30 pagesDerivatives and Risk Managementkashan khanNo ratings yet

- FRM SwapsDocument64 pagesFRM Swapsakhilyerawar7013No ratings yet

- Risk Management Using Derivative ProductsDocument48 pagesRisk Management Using Derivative ProductschandranilNo ratings yet

- 5.4.3 Term Structure Model and Interest Rate Trees: Example 5.12 BDT Tree CalibrationDocument5 pages5.4.3 Term Structure Model and Interest Rate Trees: Example 5.12 BDT Tree CalibrationmoritemNo ratings yet

- Exchange Rates ForecastingDocument25 pagesExchange Rates ForecastingBarrath RamakrishnanNo ratings yet

- FOREX MARKETS Part 2Document60 pagesFOREX MARKETS Part 2Parvesh AghiNo ratings yet

- CFA Level 1 - Economic AnalysisDocument3 pagesCFA Level 1 - Economic AnalysisWasim SajjadNo ratings yet

- Currency Exchange Rates: Determination and Forecasting: Presenter's Name Presenter's Title DD Month YyyyDocument39 pagesCurrency Exchange Rates: Determination and Forecasting: Presenter's Name Presenter's Title DD Month YyyybingoNo ratings yet

- Dual Range AccrualsDocument1 pageDual Range AccrualszdfgbsfdzcgbvdfcNo ratings yet

- TRS PresentationviewableDocument17 pagesTRS PresentationviewableAditya ShuklaNo ratings yet

- By Mahendra Singh SikarwarDocument21 pagesBy Mahendra Singh Sikarwarmss_singh_sikarwarNo ratings yet

- The Exponencial Yield Curve ModelDocument6 pagesThe Exponencial Yield Curve Modelleao414No ratings yet

- Capital Market Theory: An OverviewDocument38 pagesCapital Market Theory: An OverviewdevinamisraNo ratings yet

- Lecture Interest Rate ParityDocument10 pagesLecture Interest Rate ParityomeedjanNo ratings yet

- Libor Outlook - JPMorganDocument10 pagesLibor Outlook - JPMorganMichael A. McNicholasNo ratings yet

- Convertible WarrantDocument3 pagesConvertible WarrantrameshkumartNo ratings yet

- Exchange Rate Risk Assessment and Internal Techniques ofDocument19 pagesExchange Rate Risk Assessment and Internal Techniques ofSoumendra RoyNo ratings yet

- Interest Rate SwapsDocument19 pagesInterest Rate SwapsSubodh MayekarNo ratings yet

- Interest Rate DerivativesDocument58 pagesInterest Rate DerivativesIndia Forex100% (2)

- Derivative Securities MarketsDocument20 pagesDerivative Securities MarketsPatrick Earl T. PintacNo ratings yet

- Monetary and Financial Economics: Interest Rate and Currency SwapsDocument41 pagesMonetary and Financial Economics: Interest Rate and Currency SwapsIsmaîl TemsamaniNo ratings yet

- Derivatives MarketDocument71 pagesDerivatives MarketBalkrushna ShingareNo ratings yet

- Origin of All Derivatives: Risk Is The Only Constant, Uncertainty Is The Only CertaintyDocument36 pagesOrigin of All Derivatives: Risk Is The Only Constant, Uncertainty Is The Only CertaintyChinmay ShirsatNo ratings yet

- Modelling Cost at Risk - A Preliminary Approach - 0Document16 pagesModelling Cost at Risk - A Preliminary Approach - 0Uzair Ul HaqNo ratings yet

- Syndicated LoansDocument18 pagesSyndicated LoansmnlshethNo ratings yet

- Managing Transaction ExposureDocument34 pagesManaging Transaction Exposureg00028007No ratings yet

- DAIBB Foreign Exchange-2Document15 pagesDAIBB Foreign Exchange-2arman_2772762710% (1)

- Accumulator Option PDFDocument103 pagesAccumulator Option PDFsoumensahilNo ratings yet

- Measuring Exposure To Exchange Rate FluctuationsDocument38 pagesMeasuring Exposure To Exchange Rate FluctuationsImroz MahmudNo ratings yet

- Understanding Sovereign RiskDocument7 pagesUnderstanding Sovereign Risk1234567899525No ratings yet

- Value at Risk - Theory and IllustrationsDocument75 pagesValue at Risk - Theory and IllustrationsMohamed Amine ElmardiNo ratings yet

- EDHEC-Risk Publication Dynamic Risk Control ETFsDocument44 pagesEDHEC-Risk Publication Dynamic Risk Control ETFsAnindya Chakrabarty100% (1)

- Bonds CallableDocument52 pagesBonds CallablekalyanshreeNo ratings yet

- Capital Structure and LeverageDocument31 pagesCapital Structure and Leveragechandel08No ratings yet

- 14 Interest Rate and Currency SwapsDocument45 pages14 Interest Rate and Currency SwapsJogendra BeheraNo ratings yet

- 14 Interest Rate and Currency SwapsDocument28 pages14 Interest Rate and Currency SwapsRomi AlfikriNo ratings yet

- Studi Kasus LorealDocument3 pagesStudi Kasus LorealDesni0% (1)

- Colonialism and The Countryside: Exploring Official ArchivesDocument47 pagesColonialism and The Countryside: Exploring Official Archivesmonika singh100% (3)

- GD Steam TurbinesDocument1 pageGD Steam Turbinesmadhusudanan.asbNo ratings yet

- Labeling, Handling and Collection of Healthcare WasteDocument28 pagesLabeling, Handling and Collection of Healthcare WasteKanze AhiuNo ratings yet

- DCPD Editorial Ebook Till Sep 29, 19Document181 pagesDCPD Editorial Ebook Till Sep 29, 19segnumutraNo ratings yet

- Honda Case StudyDocument11 pagesHonda Case StudySarjodh SinghNo ratings yet

- The IMF Classification of Exchange Rate Regimes: Hard PegsDocument4 pagesThe IMF Classification of Exchange Rate Regimes: Hard PegsAnmol GrewalNo ratings yet

- Holiday Lighting Story With GraphicDocument2 pagesHoliday Lighting Story With GraphickourtneygeersNo ratings yet

- Country Report MyanmarDocument34 pagesCountry Report MyanmarAchit zaw tun myatNo ratings yet

- Shengen Visa DetailsDocument17 pagesShengen Visa DetailshugocorzoNo ratings yet

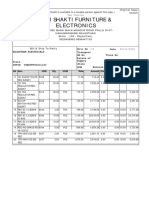

- Shri Shakti Furniture & Electronics: Credit OrginalDocument1 pageShri Shakti Furniture & Electronics: Credit OrginalRahul BansalNo ratings yet

- Industry Projections 2020: Australian Cattle - April UpdateDocument7 pagesIndustry Projections 2020: Australian Cattle - April UpdateMark RippetoeNo ratings yet

- There Were No Winners in This Govt Shutdown.Document4 pagesThere Were No Winners in This Govt Shutdown.My Brightest Star Park JisungNo ratings yet

- Usfda-Generic Drug User Fee Act - A Complete ReviewDocument15 pagesUsfda-Generic Drug User Fee Act - A Complete ReviewijsidonlineinfoNo ratings yet

- Samahan NG Manggagawa Sa Hanjin Shipyard V Hanjin Heavy IndustriesDocument3 pagesSamahan NG Manggagawa Sa Hanjin Shipyard V Hanjin Heavy IndustriesTippy Dos SantosNo ratings yet

- VP Director IT Professional Services in Detroit MI Resume Rick PaulDocument3 pagesVP Director IT Professional Services in Detroit MI Resume Rick PaulRickPaulNo ratings yet

- Overview of HR Shared ServicesDocument21 pagesOverview of HR Shared ServicesAyman ShetaNo ratings yet

- Use The Figure Below To Answer The Following QuestionsDocument5 pagesUse The Figure Below To Answer The Following QuestionsSlock TruNo ratings yet

- DAILYRATES ForexDocument1 pageDAILYRATES Forexjaydeekee jdkNo ratings yet

- The Australian EconomyDocument35 pagesThe Australian Economybiangbiang bangNo ratings yet

- Kotak Mahindra ProjectDocument79 pagesKotak Mahindra Project98108992% (24)

- GST TEST 1 by Vivek GabaDocument3 pagesGST TEST 1 by Vivek GabaAnkit KumarNo ratings yet

- Syracuse City School District Superintendent S Proposed 2011-2012 Budget Executive SummaryDocument29 pagesSyracuse City School District Superintendent S Proposed 2011-2012 Budget Executive SummaryTime Warner Cable NewsNo ratings yet

- BS en 288-4-1992Document30 pagesBS en 288-4-1992CocaCodaNo ratings yet

- JBC Travel and ToursDocument15 pagesJBC Travel and ToursArshier Ching0% (1)

- Special Power of AttorneyDocument2 pagesSpecial Power of AttorneyjustineNo ratings yet

- Project On VST TillersDocument7 pagesProject On VST TillersrajeshthumsiNo ratings yet