You might also like

- Corporate Governance Practices in IndiaDocument16 pagesCorporate Governance Practices in IndiaNur sana KhatunNo ratings yet

- Introduction To Corporate GovernanceDocument12 pagesIntroduction To Corporate GovernanceArvind KushwahaNo ratings yet

- k5 Learning Reader Level RDocument91 pagesk5 Learning Reader Level RanurasNo ratings yet

- Chapter I:-: Corporate Governance:-An Introduction IntroductionDocument76 pagesChapter I:-: Corporate Governance:-An Introduction IntroductionrampunjaniNo ratings yet

- Assignment No. 5 - Case Digest - Legal CounselingDocument10 pagesAssignment No. 5 - Case Digest - Legal CounselingglennNo ratings yet

- Corporate Governance May Be Defined As FollowsDocument7 pagesCorporate Governance May Be Defined As Followsbarkha chandnaNo ratings yet

- Tugas SessionDocument4 pagesTugas SessionJoko Budiman100% (1)

- Corporate Governance Short NotesDocument8 pagesCorporate Governance Short NotesVivekNo ratings yet

- Trimble Precision IQ Application Manuel Utilisateur v2BDocument343 pagesTrimble Precision IQ Application Manuel Utilisateur v2BOlivier LequebinNo ratings yet

- Corporate Governance: - A Case Study of Satyam Computers Services LTDDocument10 pagesCorporate Governance: - A Case Study of Satyam Computers Services LTDShashikant YadavNo ratings yet

- Vocabulary + Grammar Unit 6 Test ADocument4 pagesVocabulary + Grammar Unit 6 Test ABe HajNo ratings yet

- Corporate Governance in IndiaDocument22 pagesCorporate Governance in Indiaaishwaryasamanta0% (1)

- Corporate Governance: Recommendations For Voluntary AdoptionDocument25 pagesCorporate Governance: Recommendations For Voluntary AdoptionVikas VickyNo ratings yet

- CORPORATE GOVERNANCE CommiteesDocument39 pagesCORPORATE GOVERNANCE Commiteeskush mandaliaNo ratings yet

- Becg Unit-4.Document12 pagesBecg Unit-4.Bhaskaran Balamurali100% (2)

- Module 2 Cg. 2022Document39 pagesModule 2 Cg. 2022Parikshit MishraNo ratings yet

- Corporate Law ProjectDocument11 pagesCorporate Law ProjectShurbhi YadavNo ratings yet

- Corporate Governance in IndiaDocument7 pagesCorporate Governance in Indiaayushsinghal124No ratings yet

- Business Ethics - Final HardDocument31 pagesBusiness Ethics - Final HardjinnymistNo ratings yet

- Corporate Governance in India: A Legal Analysis: Prabhash Dalei, Paridhi Tulsyan and Shikhar MaraviDocument3 pagesCorporate Governance in India: A Legal Analysis: Prabhash Dalei, Paridhi Tulsyan and Shikhar MaraviManoj DhamiNo ratings yet

- KumarmangalamDocument2 pagesKumarmangalamRahul VashishtNo ratings yet

- 4.Management-Legal Aspects of Corporate Governance For IT Companies in IndiaDocument8 pages4.Management-Legal Aspects of Corporate Governance For IT Companies in IndiaImpact JournalsNo ratings yet

- Corporate Governance-Revisiting EthicsDocument2 pagesCorporate Governance-Revisiting EthicsUsha NNo ratings yet

- Corporate Governance in BanksDocument9 pagesCorporate Governance in BanksVjNo ratings yet

- Corporate Governance Is Much Talked AboutDocument11 pagesCorporate Governance Is Much Talked AboutVaibhav GuptaNo ratings yet

- Corporate Governance FinalDocument63 pagesCorporate Governance Finalrampunjani100% (1)

- Corporate GovernanceDocument13 pagesCorporate GovernanceSahilNo ratings yet

- Answer Sheet Corporate Law 2 cl2Document15 pagesAnswer Sheet Corporate Law 2 cl2Muskan KhatriNo ratings yet

- Corporate Governance in India - Clause 49 of Listing AgreementDocument9 pagesCorporate Governance in India - Clause 49 of Listing AgreementSanjay DessaiNo ratings yet

- CG in IndiaDocument4 pagesCG in IndiagprasadatvuNo ratings yet

- FM 2 Group 7Document19 pagesFM 2 Group 7Payal PatelNo ratings yet

- Corporate GovernanceDocument10 pagesCorporate GovernancepriitiikuumariiNo ratings yet

- Audit AssignmentDocument3 pagesAudit AssignmentHiya BhandariBD21070No ratings yet

- What Is Corporate GovernanceDocument4 pagesWhat Is Corporate GovernanceKritika SinghNo ratings yet

- Corporate Govern Hardcopy - ComparisonDocument58 pagesCorporate Govern Hardcopy - ComparisonAnkit PandyaNo ratings yet

- Becg - MFC 4th SemDocument29 pagesBecg - MFC 4th SemDrRashmiranjan PanigrahiNo ratings yet

- Narayan Murthy ReportDocument3 pagesNarayan Murthy Reportvicky20008100% (1)

- B Vivek Sirohi 56 RelCommDocument4 pagesB Vivek Sirohi 56 RelCommVivek SirohiNo ratings yet

- Business Ethics Governance and RiskDocument9 pagesBusiness Ethics Governance and Riskasha sinhaNo ratings yet

- Corporate GovernanceDocument7 pagesCorporate GovernanceANJALI RAJNo ratings yet

- Corporate GovernanceDocument7 pagesCorporate GovernanceANJALI RAJNo ratings yet

- Unit 3.3 - Future of CGDocument17 pagesUnit 3.3 - Future of CGNithyasri MuthuNo ratings yet

- Unit 5 PDFDocument6 pagesUnit 5 PDFDarshni PriyaNo ratings yet

- Corporate Governance NotesDocument6 pagesCorporate Governance NotesSunayana GuptaNo ratings yet

- Corporate Governance InitiativesDocument23 pagesCorporate Governance Initiativessocioh companyNo ratings yet

- Determinants of Governance Parameters Towards Investor's Performance in Perspective of Regulatory and Legal FrameworkDocument24 pagesDeterminants of Governance Parameters Towards Investor's Performance in Perspective of Regulatory and Legal FrameworkNam Khánh TrầnNo ratings yet

- Symbiosis Law School, Pune: Corporate Governance and FinanceDocument9 pagesSymbiosis Law School, Pune: Corporate Governance and FinancebashiNo ratings yet

- Symbiosis Law School, Pune: Corporate Governance and FinanceDocument9 pagesSymbiosis Law School, Pune: Corporate Governance and FinancebashiNo ratings yet

- Corporate Governance and Combined CodeDocument9 pagesCorporate Governance and Combined CodeSiddharth NairNo ratings yet

- Principles, Relevance and Need For Urban Cooperative Banks: Corporate GovernanceDocument52 pagesPrinciples, Relevance and Need For Urban Cooperative Banks: Corporate GovernanceAmit MaisuriyaNo ratings yet

- Project Report - Corporate GovernanceDocument39 pagesProject Report - Corporate GovernanceShruti AgrawalNo ratings yet

- Hampel (Hampel Report, 1968)Document4 pagesHampel (Hampel Report, 1968)Dhruv JainNo ratings yet

- C G R: W ?: T B.b.a., Ll.b. (H .)Document14 pagesC G R: W ?: T B.b.a., Ll.b. (H .)souravNo ratings yet

- Corporate GovernanceDocument52 pagesCorporate GovernancePrathap MpNo ratings yet

- Mahindra & Mahindra Financial Services LTD.: Team 28Document8 pagesMahindra & Mahindra Financial Services LTD.: Team 28roller worldNo ratings yet

- Corporate Governance Issue in IndiaDocument5 pagesCorporate Governance Issue in IndiaVijaya Kumar100% (1)

- Corporate GovernanceDocument22 pagesCorporate GovernanceRajesh sharmaNo ratings yet

- Comparative Analysis of Best Practices of Corporate GovernanceDocument14 pagesComparative Analysis of Best Practices of Corporate Governancetathagata_bnrjNo ratings yet

- Project On Corporate GovernanceDocument28 pagesProject On Corporate GovernanceRashmiNo ratings yet

- Preface:: Kumar Mangalam Birla CommitteeDocument4 pagesPreface:: Kumar Mangalam Birla CommitteeShainaazKhanNo ratings yet

- Kumar Mangalam Birla: Committee Report On Corporate GovernanceDocument16 pagesKumar Mangalam Birla: Committee Report On Corporate GovernanceSiddharth SinghNo ratings yet

- Certificate Course On Corporate GovernanceDocument7 pagesCertificate Course On Corporate Governancedeepak singhalNo ratings yet

- Corporate Governance and Insider TradingDocument10 pagesCorporate Governance and Insider TradingSrijesh SinghNo ratings yet

- Corporate GovernanceDocument89 pagesCorporate GovernanceGaurav AroraNo ratings yet

- CALAMBA NegoSale Batch 47110 012023Document18 pagesCALAMBA NegoSale Batch 47110 012023Dodie PelausaNo ratings yet

- ChrisDocument5 pagesChrisDpNo ratings yet

- Herrera v. COMELEC, G.R. No. 131499, November 17, 1999Document2 pagesHerrera v. COMELEC, G.R. No. 131499, November 17, 1999Jay CruzNo ratings yet

- Adr - Long ExaminationDocument3 pagesAdr - Long ExaminationKris Angeli SaquilayanNo ratings yet

- Civil Procedure Reading AssignmentDocument1 pageCivil Procedure Reading AssignmentJacking1No ratings yet

- Difference Between General Offer and Specific OfferDocument4 pagesDifference Between General Offer and Specific Offerrafat bin sadikNo ratings yet

- Internship Offer LetterDocument7 pagesInternship Offer LetterVidit JainNo ratings yet

- Bersamin v. People - G.R. No. 239957Document6 pagesBersamin v. People - G.R. No. 239957Ash SatoshiNo ratings yet

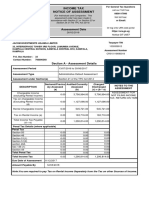

- Assessment Date: Income Tax Notice of AssessmentDocument2 pagesAssessment Date: Income Tax Notice of AssessmentBwana KuubwaNo ratings yet

- Moot Memorial Criminal LawDocument19 pagesMoot Memorial Criminal Lawshahbaz AkhtarNo ratings yet

- Detailed Summary Report Contributions and Expenditures: 1. Full Name ofDocument22 pagesDetailed Summary Report Contributions and Expenditures: 1. Full Name ofspydraNo ratings yet

- Exercises For Process AnalysisDocument2 pagesExercises For Process AnalysisYuenNo ratings yet

- Estacode 2019Document1,043 pagesEstacode 2019Abubakar Zubair100% (4)

- 10 - Jocson Vs CA, GR L-553322, February 16, 2006Document5 pages10 - Jocson Vs CA, GR L-553322, February 16, 2006romeo stodNo ratings yet

- Work Order: Add: IGST Add: SGST Add: CGST 0.00 5,022.00 5,022.00Document1 pageWork Order: Add: IGST Add: SGST Add: CGST 0.00 5,022.00 5,022.00VinodNo ratings yet

- Area / Perimeter Worksheet: Draw A Rectangle With An Area of 40 Square Units. Find The Area of This RectangleDocument2 pagesArea / Perimeter Worksheet: Draw A Rectangle With An Area of 40 Square Units. Find The Area of This RectangleAljun PorcinculaNo ratings yet

- University of Health Sciences, Lahore: Admission Form ForDocument2 pagesUniversity of Health Sciences, Lahore: Admission Form ForZahid SarfrazNo ratings yet

- Belgica vs. Ochoa Case DigestDocument2 pagesBelgica vs. Ochoa Case DigestTynny Roo BelduaNo ratings yet

- Legal Ethics Case DigestsssDocument13 pagesLegal Ethics Case Digestssswins lynNo ratings yet

- LLM (Labour Law) - II Sem - Ist AssignmentDocument26 pagesLLM (Labour Law) - II Sem - Ist AssignmentHitesh P KumarNo ratings yet

- pc13-04 Tss CrossingDocument4 pagespc13-04 Tss CrossingSanjiv KumarNo ratings yet

- 1st Year For Project Topics-1Document4 pages1st Year For Project Topics-1Clashin FashNo ratings yet

- Colombia Room Rental ContractDocument3 pagesColombia Room Rental ContractScribdTranslationsNo ratings yet

- Labour Rights and The Constitution: Law Academic Twice Winner of UCT Book PrizeDocument12 pagesLabour Rights and The Constitution: Law Academic Twice Winner of UCT Book PrizeXolani MpilaNo ratings yet

- Iqbal Ismail V State of MaharashtraDocument11 pagesIqbal Ismail V State of Maharashtrasagar jainNo ratings yet