You might also like

- Sec 7060Document17 pagesSec 7060Fallon LoboNo ratings yet

- Advance Auditing & Assurance (OnlineDocument15 pagesAdvance Auditing & Assurance (OnlineHaider BhaiNo ratings yet

- Audit Quiz ResultsDocument5 pagesAudit Quiz ResultsTiến Thành NguyễnNo ratings yet

- CasesDocument24 pagesCasesXuan LieuNo ratings yet

- Consolidated Balance Sheet Worksheet for Punto CompanyDocument21 pagesConsolidated Balance Sheet Worksheet for Punto CompanyDamy RoseNo ratings yet

- Chapter 01Document5 pagesChapter 01Alima Toon Noor Ridita 1612638630No ratings yet

- Chapter 1 - The Concept of Audit and Other Assurance EngagementsDocument5 pagesChapter 1 - The Concept of Audit and Other Assurance EngagementsSelva Bavani Selwadurai50% (2)

- Case Study Ep November 2012Document19 pagesCase Study Ep November 2012Sajjad Cheema100% (1)

- Multi Task Questions.Document8 pagesMulti Task Questions.wilbertNo ratings yet

- Acca f8 MockDocument8 pagesAcca f8 MockMuhammad Kamran Khan100% (3)

- Insurance PolicyDocument3 pagesInsurance PolicyGlenn GalvezNo ratings yet

- Collins TCPA Fee ContestDocument229 pagesCollins TCPA Fee ContestDaniel FisherNo ratings yet

- Critical Financial Review: Understanding Corporate Financial InformationFrom EverandCritical Financial Review: Understanding Corporate Financial InformationNo ratings yet

- All ISADocument30 pagesAll ISANTurin1435No ratings yet

- ATR Answers - 5Document43 pagesATR Answers - 5Christine Jane AbangNo ratings yet

- f1 Acca Lesson2Document8 pagesf1 Acca Lesson2Ganit SimonNo ratings yet

- International Standards on Auditing NotesDocument47 pagesInternational Standards on Auditing NotesMuhammad QamarNo ratings yet

- Auditing S2 - Chapter 5Document11 pagesAuditing S2 - Chapter 5p aloaNo ratings yet

- SMA QuizDocument76 pagesSMA QuizQuỳnh ChâuNo ratings yet

- f8 Learning Material Ahmed ShafiDocument23 pagesf8 Learning Material Ahmed ShafiMubashirNo ratings yet

- Audit and AssuranceDocument16 pagesAudit and AssuranceAmolaNo ratings yet

- International Standard of AuditingDocument4 pagesInternational Standard of AuditingSuvro AvroNo ratings yet

- ACCO 1152 Audit and Assurance Exam 1 - Exam Paper May 2015Document4 pagesACCO 1152 Audit and Assurance Exam 1 - Exam Paper May 2015kantarubanNo ratings yet

- Financial AuditDocument3 pagesFinancial AuditgalaxystarNo ratings yet

- Principles-Versus Rules-Based Accounting Standards: The FASB's Standard Setting StrategyDocument24 pagesPrinciples-Versus Rules-Based Accounting Standards: The FASB's Standard Setting StrategyEhab AgwaNo ratings yet

- Solutions Manual: 1st EditionDocument29 pagesSolutions Manual: 1st EditionJunior Waqairasari100% (3)

- Ch17 - Discounted CFDocument20 pagesCh17 - Discounted CFjklein2588No ratings yet

- Final Financials-Adam's Apple 2019Document26 pagesFinal Financials-Adam's Apple 2019tsere butsereNo ratings yet

- IFRS Chapter 1 SummaryDocument4 pagesIFRS Chapter 1 SummaryAsif AliNo ratings yet

- Auditing Theory Question BankDocument38 pagesAuditing Theory Question BankBapu FinuNo ratings yet

- MA ACCA Sunway Tes Chapter AssessmentDocument434 pagesMA ACCA Sunway Tes Chapter AssessmentFarahAin Fain100% (2)

- 8int 2006 Jun QDocument4 pages8int 2006 Jun Qapi-19836745No ratings yet

- Fma Past Paper 3 (F2)Document24 pagesFma Past Paper 3 (F2)Shereka EllisNo ratings yet

- Assignment # 1: Submitted FromDocument15 pagesAssignment # 1: Submitted FromAbdullah AliNo ratings yet

- Auditor Rights and ResponsibilitiesDocument16 pagesAuditor Rights and ResponsibilitiesSohel Rana100% (1)

- BodyDocument263 pagesBodyTiyas KurniaNo ratings yet

- F9 Past PapersDocument32 pagesF9 Past PapersBurhan MaqsoodNo ratings yet

- ACCA F7 Revision Mock June 2013 QUESTIONS Version 4 FINAL at 25 March 2013 PDFDocument11 pagesACCA F7 Revision Mock June 2013 QUESTIONS Version 4 FINAL at 25 March 2013 PDFPiyal HossainNo ratings yet

- Trimake Limited Makes Three Main Products Using Broadly The SameDocument2 pagesTrimake Limited Makes Three Main Products Using Broadly The SameAmit PandeyNo ratings yet

- SA 701 MCQsDocument2 pagesSA 701 MCQspreethesh kumarNo ratings yet

- Assurance Sample Paper 2016Document23 pagesAssurance Sample Paper 2016Lingeshwaren ChandramorganNo ratings yet

- CAS 520 Analytical ProceduresDocument8 pagesCAS 520 Analytical ProcedureszelcomeiaukNo ratings yet

- F20-AAUD Questions Dec08Document3 pagesF20-AAUD Questions Dec08irfanki0% (1)

- IMChap 006Document18 pagesIMChap 006Aaron HamiltonNo ratings yet

- Beams10e Ch01 Business CombinationsDocument39 pagesBeams10e Ch01 Business CombinationsmegaangginaNo ratings yet

- Chapter 3 Outline - Audit ReportsDocument11 pagesChapter 3 Outline - Audit Reportstjn8240100% (1)

- Cima C01 Samplequestions Mar2013Document28 pagesCima C01 Samplequestions Mar2013Abhiroop Roy100% (1)

- Chapter 1 - Updated-1 PDFDocument29 pagesChapter 1 - Updated-1 PDFj000diNo ratings yet

- AT1 - June 2002Document18 pagesAT1 - June 2002thusi1No ratings yet

- December 2002 ACCA Paper 2.5 QuestionsDocument11 pagesDecember 2002 ACCA Paper 2.5 QuestionsUlanda2No ratings yet

- Question Bank - App. Level - Audit & Assurance-Nov-Dec 2011 To May-June-2016Document41 pagesQuestion Bank - App. Level - Audit & Assurance-Nov-Dec 2011 To May-June-2016Sharif MahmudNo ratings yet

- Chapter 12 Suggestions For Case Analysis: Strategic Management & Business Policy, 13e (Wheelen/Hunger)Document21 pagesChapter 12 Suggestions For Case Analysis: Strategic Management & Business Policy, 13e (Wheelen/Hunger)Bayan HasanNo ratings yet

- Far Ifrs Sept 2020 PDFDocument6 pagesFar Ifrs Sept 2020 PDFhertzberg 1No ratings yet

- Arens Aud16 Inppt24Document48 pagesArens Aud16 Inppt24Bdour AlaliNo ratings yet

- Solution To Assignment 1 Winter 2017 ADM 4348Document19 pagesSolution To Assignment 1 Winter 2017 ADM 4348CodyzqzeaniLombNo ratings yet

- IPSAS Explained: A Summary of International Public Sector Accounting StandardsFrom EverandIPSAS Explained: A Summary of International Public Sector Accounting StandardsNo ratings yet

- Corporate Financial Analysis with Microsoft ExcelFrom EverandCorporate Financial Analysis with Microsoft ExcelRating: 5 out of 5 stars5/5 (1)

- Wiley Not-for-Profit GAAP 2017: Interpretation and Application of Generally Accepted Accounting PrinciplesFrom EverandWiley Not-for-Profit GAAP 2017: Interpretation and Application of Generally Accepted Accounting PrinciplesNo ratings yet

- Reading 37 Activo Fijo PreguntasDocument7 pagesReading 37 Activo Fijo PreguntasdidioserNo ratings yet

- The Statement of Cash Flows QuestionsDocument19 pagesThe Statement of Cash Flows Questionsdidioser0% (1)

- Preguntas TipoDocument52 pagesPreguntas TipodidioserNo ratings yet

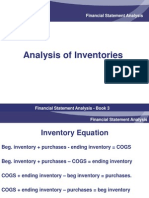

- Reading 35: Analysis of InventoriesDocument9 pagesReading 35: Analysis of InventoriesdidioserNo ratings yet

- Inventario Con PreguntasDocument61 pagesInventario Con PreguntasdidioserNo ratings yet

- Calculate cash flow from operations using indirect method financial dataDocument15 pagesCalculate cash flow from operations using indirect method financial datadidioserNo ratings yet

- CH 02Document74 pagesCH 02didioserNo ratings yet

- CH 03Document51 pagesCH 03Rizka YulianaNo ratings yet

- WJP Index Report 2012 The Most Corrupted CountriesDocument246 pagesWJP Index Report 2012 The Most Corrupted CountriesmaduradasNo ratings yet

- Activo Fijo Con PreguntasDocument67 pagesActivo Fijo Con PreguntashfiehfhejfhneifNo ratings yet

- CH 01Document32 pagesCH 01didioserNo ratings yet

- Management Control Systems: Class 2Document18 pagesManagement Control Systems: Class 2didioserNo ratings yet

- Class1 110812Document21 pagesClass1 110812didioserNo ratings yet

- Star WarsDocument143 pagesStar WarsdidioserNo ratings yet

- Sample Business Plan TemplateDocument19 pagesSample Business Plan TemplateHafidz Al Rusdy100% (1)

- Evaluating IT Outsourcing Risks and Cost SavingsDocument25 pagesEvaluating IT Outsourcing Risks and Cost SavingsPiyush JaainNo ratings yet

- Bba 301Document10 pagesBba 301rohanNo ratings yet

- Learning Module #3 Investment and Portfolio Management: Participating, and Cumulative and ParticipatingDocument6 pagesLearning Module #3 Investment and Portfolio Management: Participating, and Cumulative and ParticipatingAira AbigailNo ratings yet

- CAPITAL MARKET FRAUD EXPOSEDDocument7 pagesCAPITAL MARKET FRAUD EXPOSEDPratikchya BasnetNo ratings yet

- Forex Courses ListDocument9 pagesForex Courses ListTaKo TaKoNo ratings yet

- Assignment On Analysis of Annual Report ofDocument12 pagesAssignment On Analysis of Annual Report ofdevbreezeNo ratings yet

- AR29Document405 pagesAR29HarveyNo ratings yet

- MTN PitchbookDocument21 pagesMTN PitchbookGideon Antwi Boadi100% (1)

- Zurich Insurance Malaysia Investment-Linked Foreign Edge FundsDocument39 pagesZurich Insurance Malaysia Investment-Linked Foreign Edge Fundsnantah2299No ratings yet

- Continental CarriersDocument2 pagesContinental Carrierschch917100% (1)

- Advanced Accounting: Stock Investments - Investor Accounting and ReportingDocument30 pagesAdvanced Accounting: Stock Investments - Investor Accounting and ReportingNafilah Rahma100% (1)

- 2005 10 XBRL Progress ReportDocument18 pages2005 10 XBRL Progress ReportkjheiinNo ratings yet

- David SMCC16ge Ppt06Document52 pagesDavid SMCC16ge Ppt06JoannaGañaNo ratings yet

- GTP Investor Business PlanDocument28 pagesGTP Investor Business PlanPraksi Teodor VasoNo ratings yet

- Q9Document9 pagesQ9asastuffNo ratings yet

- Non-Deposit Taking NBFIs Business RulesDocument24 pagesNon-Deposit Taking NBFIs Business RulesPrince McGershonNo ratings yet

- Name - KEYDocument30 pagesName - KEYjhouvanNo ratings yet

- Republic Act No. 7652Document2 pagesRepublic Act No. 7652Ju BalajadiaNo ratings yet

- Fund Transfer Pricing in Banking Risk ManagementDocument20 pagesFund Transfer Pricing in Banking Risk ManagementNazmul H. PalashNo ratings yet

- Alterations to Listed Breakwater and Viaduct on Portland HarbourDocument18 pagesAlterations to Listed Breakwater and Viaduct on Portland HarbourAnonymous Lx3jPjHAVLNo ratings yet

- AVEVA CoW BrochureDocument8 pagesAVEVA CoW BrochureerikestrelaNo ratings yet

- Stated Objective: Dow Jones Stoxx Global 1800 IndexDocument2 pagesStated Objective: Dow Jones Stoxx Global 1800 IndexMutimbaNo ratings yet

- Capital StructureDocument7 pagesCapital StructurePrashanth MagadumNo ratings yet

- Flex STP LeafletDocument2 pagesFlex STP LeafletvinorpatilNo ratings yet

- A Comparative Study On Investment Policy of Nabil and Nepal Sbi Bank Ltd.Document111 pagesA Comparative Study On Investment Policy of Nabil and Nepal Sbi Bank Ltd.kabibhandariNo ratings yet

- APM Terminals Company PresentationDocument28 pagesAPM Terminals Company Presentationchuongnino123No ratings yet

- Square Root TheoryDocument2 pagesSquare Root Theoryabdi1100% (2)

- Success StoriesDocument255 pagesSuccess Storiesflaquitoquerio125100% (10)