You might also like

- Testing Risk DocumentDocument15 pagesTesting Risk Documentapi-3831102No ratings yet

- ECI082206 (Short Circuit) Ver0000DDocument5 pagesECI082206 (Short Circuit) Ver0000Dyasararafat12010No ratings yet

- ECI082206 (Short Circuit) Ver0000DDocument5 pagesECI082206 (Short Circuit) Ver0000DElsayed Abdelmagid MohamedNo ratings yet

- EPCDocument31 pagesEPCSubash KumarNo ratings yet

- Integration of CCGT Plant and LNG TerminalDocument28 pagesIntegration of CCGT Plant and LNG Terminalcicko45100% (1)

- Eplc Risk Management LogDocument7 pagesEplc Risk Management LogChinh Lê ĐìnhNo ratings yet

- P1.T2.Jorion 97 102 127 133 v1 PDFDocument5 pagesP1.T2.Jorion 97 102 127 133 v1 PDFHasan SadozyeNo ratings yet

- Project Risk ManagementDocument96 pagesProject Risk ManagementYudikaWisnuPratomo0% (1)

- A Risk and Vulnerability Ontology For Construction Projects (İnşaat Projeleri Için Bir Risk Ve Risk Kırılganlığı Ontolojisi)Document132 pagesA Risk and Vulnerability Ontology For Construction Projects (İnşaat Projeleri Için Bir Risk Ve Risk Kırılganlığı Ontolojisi)Çağrı KARABİLLİOĞLU0% (1)

- Evaluation of Risk Assessment Techniques in The Project AnalysisDocument10 pagesEvaluation of Risk Assessment Techniques in The Project Analysisjahid.coolNo ratings yet

- Flow Chart Sewage TreatmentDocument2 pagesFlow Chart Sewage TreatmentapriNo ratings yet

- Basler Electric TCCDocument7 pagesBasler Electric TCCGalih Trisna NugrahaNo ratings yet

- University Departments: Anna University Chennai:: Chennai 600 025Document30 pagesUniversity Departments: Anna University Chennai:: Chennai 600 025Manju Satpo50% (2)

- AHP - TutorialDocument21 pagesAHP - TutorialBenhassineMedaliNo ratings yet

- Approved: Soumen Mitra Senior Mec Engineer 30-May-12Document2 pagesApproved: Soumen Mitra Senior Mec Engineer 30-May-12tvpham123No ratings yet

- Lanco 8.5 Mva GTP Rv.01Document14 pagesLanco 8.5 Mva GTP Rv.01Pankaj TiwariNo ratings yet

- Fat TLX Uk - 03,31 JPM 2012-11-16Document129 pagesFat TLX Uk - 03,31 JPM 2012-11-16gunmoula1No ratings yet

- Earned Value 0606Document4 pagesEarned Value 0606karna@No ratings yet

- Sizing Calculation of Generator Step Up Transformer in MVA As Per IEEEDocument3 pagesSizing Calculation of Generator Step Up Transformer in MVA As Per IEEEMadhabNo ratings yet

- Distribution System Reliability Analysis: Operation Technology, Inc. 1 Etap PowerstationDocument22 pagesDistribution System Reliability Analysis: Operation Technology, Inc. 1 Etap PowerstationAndres VergaraNo ratings yet

- Risk Management During Operation and Maintainance of Power ProjectDocument17 pagesRisk Management During Operation and Maintainance of Power Projectadzli maher100% (1)

- Risk Management at EnronDocument28 pagesRisk Management at Enronbim_durNo ratings yet

- Risk Management in EPC Contract - Risk Identification: Rahul Bali and Prof M.R ApteDocument6 pagesRisk Management in EPC Contract - Risk Identification: Rahul Bali and Prof M.R ApteAkhileshkumar PandeyNo ratings yet

- Gen-Spc-Elc-6102 - Rev. BDocument13 pagesGen-Spc-Elc-6102 - Rev. BAHMED AMIRANo ratings yet

- Hoja Datos Celda de MT-OutdoorDocument2 pagesHoja Datos Celda de MT-Outdoorjohn rangelNo ratings yet

- 4ac87a3d4b8cbCV Shrinwantu ChowdhuryDocument7 pages4ac87a3d4b8cbCV Shrinwantu ChowdhuryKamalraj SoundararajanNo ratings yet

- SENSITIVITY ANALYSIS Kk.Document11 pagesSENSITIVITY ANALYSIS Kk.Kunle OketoboNo ratings yet

- Aim PDFDocument6 pagesAim PDFSlim Ben SlimaneNo ratings yet

- Estimate Project Cost Contingency Using Monte Carlo SimulationDocument5 pagesEstimate Project Cost Contingency Using Monte Carlo SimulationPeterNo ratings yet

- Project Finance: Aditya Agarwal Sandeep KaulDocument96 pagesProject Finance: Aditya Agarwal Sandeep Kaulsguha123No ratings yet

- Engineering Economic AnalysisDocument16 pagesEngineering Economic AnalysisAnyela Yulissa100% (1)

- 01-08-2013 Issue For InformationDocument5 pages01-08-2013 Issue For Informationtvpham123No ratings yet

- Break EvenDocument36 pagesBreak EvenNila ChotaiNo ratings yet

- Ts 240 SQMM Cable JSPLDocument4 pagesTs 240 SQMM Cable JSPLAnonymous vcadX45TD7100% (1)

- Cable Sizing ToolDocument6 pagesCable Sizing ToolmipanosNo ratings yet

- IEC 61511 Implementation - The Execution ChallengeDocument7 pagesIEC 61511 Implementation - The Execution Challengehmatora72_905124701No ratings yet

- MV Switchgear CT Inspection and Test Procedure: October 2019Document6 pagesMV Switchgear CT Inspection and Test Procedure: October 2019sabamalar100% (1)

- Schedule Risk AnalysisDocument14 pagesSchedule Risk AnalysisPatricio Alejandro Vargas FuenzalidaNo ratings yet

- AMEC Technical Study Report 2009-08-27Document58 pagesAMEC Technical Study Report 2009-08-27Hannel TamayoNo ratings yet

- Session 1 - Project Risk ManagementDocument21 pagesSession 1 - Project Risk ManagementShahzad Sultan AliNo ratings yet

- TenderDocument165 pagesTenderAnkur AnilNo ratings yet

- AHP Lesson 2Document12 pagesAHP Lesson 2Kanav NarangNo ratings yet

- Battery Failure PredictionDocument10 pagesBattery Failure PredictionChris Baddeley100% (1)

- Project Finance: Valuing Unlevered ProjectsDocument41 pagesProject Finance: Valuing Unlevered ProjectsKelsey GaoNo ratings yet

- 8 LMS-Tutorial CFW PDFDocument6 pages8 LMS-Tutorial CFW PDFEnriko SagaNo ratings yet

- Session 3: Project Unlevered Cost of Capital: N. K. Chidambaran Corporate FinanceDocument25 pagesSession 3: Project Unlevered Cost of Capital: N. K. Chidambaran Corporate FinanceSaurabh GuptaNo ratings yet

- Aggregate Supply, Unemployment and InflationDocument103 pagesAggregate Supply, Unemployment and Inflationapi-3825580No ratings yet

- Risk Assessment Cover Sheet: Wayame 150kV ProjectDocument42 pagesRisk Assessment Cover Sheet: Wayame 150kV ProjectBaso Firdaus PannecceNo ratings yet

- AHP Lesson 1Document5 pagesAHP Lesson 1Konstantinos ParaskevopoulosNo ratings yet

- Risk Management in Construction-DrDocument14 pagesRisk Management in Construction-Dramr raghebNo ratings yet

- Risk Analysis in Capital BudgetingDocument30 pagesRisk Analysis in Capital BudgetingtecharupNo ratings yet

- Project Risk AnalysisDocument72 pagesProject Risk AnalysislizaNo ratings yet

- Risk Analysis in Investment AppraisalDocument33 pagesRisk Analysis in Investment Appraisalkevinlan100% (1)

- 4.risk ManagementDocument36 pages4.risk ManagementRahul M. DasNo ratings yet

- Risk and Uncertainity - Final (4) PPDocument43 pagesRisk and Uncertainity - Final (4) PPAnushka MadanNo ratings yet

- Risk Analysis in Capital BudgetingDocument40 pagesRisk Analysis in Capital BudgetingNicola LoveNo ratings yet

- Session - 4Document12 pagesSession - 4Amal SooriarachchiNo ratings yet

- Risk and Uncertainity - FinalDocument43 pagesRisk and Uncertainity - FinalAnushka MadanNo ratings yet

- Understanding Financial Management: A Practical Guide: Guideline Answers To The Concept Check QuestionsDocument9 pagesUnderstanding Financial Management: A Practical Guide: Guideline Answers To The Concept Check QuestionsManuel BoahenNo ratings yet

- Chapter 11 Project Risk AnalysisDocument43 pagesChapter 11 Project Risk AnalysisShrutit21No ratings yet

- The Business of Investment BankingDocument56 pagesThe Business of Investment BankingParas KumarNo ratings yet

- SubrotoDocument2 pagesSubrotoVaibhav BanjanNo ratings yet

- Intro and Currency HedgingDocument12 pagesIntro and Currency HedgingVaibhav BanjanNo ratings yet

- Commercial Appraisal JNIDBDocument67 pagesCommercial Appraisal JNIDBVaibhav BanjanNo ratings yet

- Commodity Market Forwarded To ClassDocument22 pagesCommodity Market Forwarded To ClassVaibhav BanjanNo ratings yet

- Capital Flow Into IndiaDocument19 pagesCapital Flow Into IndiaVaibhav BanjanNo ratings yet

- Leading Indicators in The Indian EconomyDocument43 pagesLeading Indicators in The Indian EconomyVaibhav BanjanNo ratings yet

- Debt Market Session 9Document37 pagesDebt Market Session 9Vaibhav BanjanNo ratings yet

- Fraud Taxonomies and ModelsDocument14 pagesFraud Taxonomies and ModelsVaibhav Banjan100% (1)

- 1 77Document50 pages1 77Vaibhav BanjanNo ratings yet

- Auditors LiabilityDocument36 pagesAuditors LiabilityVaibhav BanjanNo ratings yet

- Financing InfrastructureDocument22 pagesFinancing InfrastructuresatishfinanceNo ratings yet

- Offshore banking_ financial secrecy, tax havens_ evasion, asset protection, tax efficient corporate structure, illegal reinvoicing, fraud concealment, black money _ Sanjeev Sabhlok's revolutionary blog.pdfDocument23 pagesOffshore banking_ financial secrecy, tax havens_ evasion, asset protection, tax efficient corporate structure, illegal reinvoicing, fraud concealment, black money _ Sanjeev Sabhlok's revolutionary blog.pdfVaibhav BanjanNo ratings yet

- Inflation and Capital BudgetingDocument11 pagesInflation and Capital BudgetingVaibhav Banjan100% (1)

- BCom VI Analysis of Financial StatementsDocument3 pagesBCom VI Analysis of Financial StatementsVaibhav BanjanNo ratings yet

- Sales in The Course of ExportDocument6 pagesSales in The Course of ExportVaibhav BanjanNo ratings yet

- Mcs AuditDocument28 pagesMcs AuditVaibhav BanjanNo ratings yet

- Mutual Funds: Vishal Aggarwal MBA Class of 2007Document27 pagesMutual Funds: Vishal Aggarwal MBA Class of 2007suruchibhasinNo ratings yet

- Introduction To BKGDocument60 pagesIntroduction To BKGVaibhav BanjanNo ratings yet

- BFMS Course OutlineDocument5 pagesBFMS Course OutlineSaksham GoyalNo ratings yet

- Jade Group: Company ProfileDocument18 pagesJade Group: Company Profilesajd1No ratings yet

- Case 45 Jetblue ValuationDocument12 pagesCase 45 Jetblue Valuationshawnybiha100% (1)

- Harmonic Trader IntroDocument2 pagesHarmonic Trader IntroBiantoroKunartoNo ratings yet

- Worksheet 1 Financial MathDocument8 pagesWorksheet 1 Financial Mathcaroline_amideast8101No ratings yet

- Fibonacci Ratios & Harmonic PatternsDocument10 pagesFibonacci Ratios & Harmonic Patternsgunawan kertosonoNo ratings yet

- Summer Internship Project ReportDocument86 pagesSummer Internship Project ReportShalini Chatterjee100% (2)

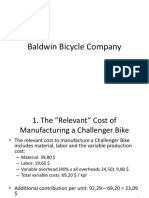

- Baldwin Bicycle Company EngDocument8 pagesBaldwin Bicycle Company EngChayan Kothari IDD,Biochem, IT-BHU, Varanasi (INDIA)No ratings yet

- Homework For Next ClassDocument3 pagesHomework For Next ClassSimo El Kettani20% (5)

- Micro-Cap Review Magazine Fall 2010Document80 pagesMicro-Cap Review Magazine Fall 2010Planet MicroCap Review MagazineNo ratings yet

- Spotless ProspectusDocument232 pagesSpotless Prospectusaovchar14No ratings yet

- Trichy Full PaperDocument13 pagesTrichy Full PaperSwetha Sree RajagopalNo ratings yet

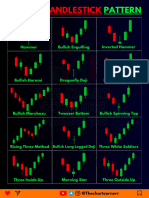

- Chart Pattern Cheat Sheet-1Document18 pagesChart Pattern Cheat Sheet-1YASHANK VISHWAKARMANo ratings yet

- Lesson 5Document48 pagesLesson 5Tony Del PieroNo ratings yet

- 'ContribDocument756 pages'ContribMatt DixonNo ratings yet

- Role of Government in The Indian EconomyDocument73 pagesRole of Government in The Indian Economyminisen1230% (2)

- An Introduction To Derivative Securities, Financial Markets, and Risk ManagementDocument66 pagesAn Introduction To Derivative Securities, Financial Markets, and Risk ManagementMuhammad AliNo ratings yet

- Government Securities MarketDocument35 pagesGovernment Securities MarketPriyanka DargadNo ratings yet

- Cross-Cultural Perspectives On Managing DiversityDocument29 pagesCross-Cultural Perspectives On Managing DiversityWade EtienneNo ratings yet

- SLVR White Paper FinalDocument16 pagesSLVR White Paper FinalTorVikNo ratings yet

- Modigliani and Miller (1958) - Assumptions: PerfectDocument27 pagesModigliani and Miller (1958) - Assumptions: PerfectCharlotte CaiNo ratings yet

- Accounting in IBDocument23 pagesAccounting in IBAbdur RajakNo ratings yet

- Does Academic Research Destroy Stock Return Predictability?Document44 pagesDoes Academic Research Destroy Stock Return Predictability?Kazi HasanNo ratings yet

- Latin Family OfficeDocument43 pagesLatin Family OfficeEduardo VianaNo ratings yet

- Daftar DisporaDocument10 pagesDaftar DisporaElena RosintaNo ratings yet

- Mplus FormDocument4 pagesMplus Formmohd fairusNo ratings yet

- Chapter 7 - : Valuation and Characteristics of BondsDocument54 pagesChapter 7 - : Valuation and Characteristics of BondsAndre SantosoNo ratings yet

- My MM TradingNotesDocument5 pagesMy MM TradingNotesnyagweyaNo ratings yet

- Negotiable Instruments Act PDFDocument30 pagesNegotiable Instruments Act PDFVishal sirsatNo ratings yet

- Form 32 Return by Management CompanyDocument2 pagesForm 32 Return by Management CompanyolingirlNo ratings yet