You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (120)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- KTT - CONTRACT - CDB - AMROCK PETROLEUM LTD - 500m-AaaDocument24 pagesKTT - CONTRACT - CDB - AMROCK PETROLEUM LTD - 500m-AaaRakibul Islam67% (3)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- SWOT Analysis of NIB BankDocument6 pagesSWOT Analysis of NIB BankAbdul Waheed83% (35)

- Plant Layout To Start A New Bank BranchDocument21 pagesPlant Layout To Start A New Bank Branchshraddha mehta0% (1)

- Financial and Accounting Procedures ManualDocument60 pagesFinancial and Accounting Procedures ManualjewelmirNo ratings yet

- Facebook 2Document9 pagesFacebook 2Niharika Satyadev JaiswalNo ratings yet

- Chapter Fifteen: Psychographics: Values, Personality, and LifestylesDocument16 pagesChapter Fifteen: Psychographics: Values, Personality, and LifestylesNiharika Satyadev JaiswalNo ratings yet

- Foreign Direct Investment and Foreign Institutional InvestorDocument11 pagesForeign Direct Investment and Foreign Institutional InvestorNiharika Satyadev JaiswalNo ratings yet

- PromotionDocument19 pagesPromotionNiharika Satyadev JaiswalNo ratings yet

- PricingDocument16 pagesPricingNiharika Satyadev JaiswalNo ratings yet

- PerceptionDocument10 pagesPerceptiongazala100% (1)

- New PerceptionDocument15 pagesNew PerceptionNiharika Satyadev JaiswalNo ratings yet

- Consumer Behavior LearningDocument15 pagesConsumer Behavior LearningNiharika Satyadev JaiswalNo ratings yet

- Assistant Professor Ajay Kumar Garg Institute of Management GhaziabadDocument21 pagesAssistant Professor Ajay Kumar Garg Institute of Management GhaziabadNiharika Satyadev JaiswalNo ratings yet

- ImplementationDocument32 pagesImplementationNiharika Satyadev JaiswalNo ratings yet

- Consumer Behavior LearningDocument15 pagesConsumer Behavior LearningNiharika Satyadev JaiswalNo ratings yet

- Communication CompetencyDocument12 pagesCommunication CompetencyNiharika Satyadev JaiswalNo ratings yet

- DistributionDocument13 pagesDistributionNiharika Satyadev JaiswalNo ratings yet

- Chap07 Establishing Objectives and Budgeting For The Promotional ProgramDocument27 pagesChap07 Establishing Objectives and Budgeting For The Promotional Programprat121100% (1)

- Brand PositioningDocument14 pagesBrand PositioningNiharika Satyadev JaiswalNo ratings yet

- Synopsis of ResearchDocument7 pagesSynopsis of ResearchNiharika Satyadev JaiswalNo ratings yet

- Training EvaluationDocument21 pagesTraining EvaluationNiharika Satyadev Jaiswal100% (1)

- The International Monetary SystemDocument25 pagesThe International Monetary SystemNiharika Satyadev JaiswalNo ratings yet

- Building An Organization Capable of Good Strategy ExecutionDocument67 pagesBuilding An Organization Capable of Good Strategy ExecutionNiharika Satyadev JaiswalNo ratings yet

- Theories of Exchange RateDocument11 pagesTheories of Exchange RateNiharika Satyadev Jaiswal100% (1)

- Top 10 CEO of IndiaDocument3 pagesTop 10 CEO of IndiaNiharika Satyadev JaiswalNo ratings yet

- Tanvi CV (New)Document2 pagesTanvi CV (New)Niharika Satyadev JaiswalNo ratings yet

- Sample SizeDocument13 pagesSample SizeNiharika Satyadev JaiswalNo ratings yet

- Syllabus MRDocument1 pageSyllabus MRNiharika Satyadev JaiswalNo ratings yet

- Porter SummaryDocument12 pagesPorter SummaryXianghuiNo ratings yet

- Ajay Kumar Garg Institute of Management GhaziabadDocument4 pagesAjay Kumar Garg Institute of Management GhaziabadNiharika Satyadev JaiswalNo ratings yet

- Post Purchase Behavior and Customer SatisfactionDocument7 pagesPost Purchase Behavior and Customer SatisfactionNiharika Satyadev JaiswalNo ratings yet

- Process of Strategic ManagementDocument16 pagesProcess of Strategic ManagementNiharika Satyadev Jaiswal100% (1)

- Ye Dooriyan LyricsDocument9 pagesYe Dooriyan LyricsNiharika Satyadev JaiswalNo ratings yet

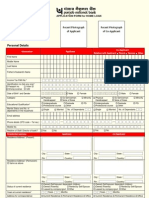

- 21-2012 PNB 1054 - Ann I - Application-Cum-Appraisal-Cum-Sanction For Housing LoanDocument9 pages21-2012 PNB 1054 - Ann I - Application-Cum-Appraisal-Cum-Sanction For Housing Loanrisk_j2546No ratings yet

- Assam BudgetDocument11 pagesAssam BudgetnazmulNo ratings yet

- InterimStmt 20231215-1Document9 pagesInterimStmt 20231215-1mitchellallie393No ratings yet

- C 202001161514442393Document43 pagesC 202001161514442393Anand RaiNo ratings yet

- Shareholder and Stakeholder Theory - After The Financial Crisis-1Document13 pagesShareholder and Stakeholder Theory - After The Financial Crisis-1Mohammed Elassad Elshazali100% (1)

- Leo Park Supporting Innovative SMEs in KoreaDocument33 pagesLeo Park Supporting Innovative SMEs in Koreamarcopolli764No ratings yet

- Money Market and Its InstrumentsDocument18 pagesMoney Market and Its InstrumentsSandip KarNo ratings yet

- BARCLAYS: Final Terms Dated 20 September 2022Document15 pagesBARCLAYS: Final Terms Dated 20 September 2022PiyushNo ratings yet

- Technology AnnualDocument84 pagesTechnology AnnualSecurities Lending TimesNo ratings yet

- International Finance Exam SolutionsDocument171 pagesInternational Finance Exam SolutionsCijaraNo ratings yet

- JW Sanitize Corporate Offer Rev 4.1Document6 pagesJW Sanitize Corporate Offer Rev 4.1Zaki YahayaNo ratings yet

- Bankstatenmmentfromfeb 24 Tomar 264562358 JHDocument6 pagesBankstatenmmentfromfeb 24 Tomar 264562358 JHJc RNo ratings yet

- Assignment No. 1 - Cash and Cash EquivalentsDocument5 pagesAssignment No. 1 - Cash and Cash EquivalentsVincent AbellaNo ratings yet

- Monetary Policy in CanadaDocument24 pagesMonetary Policy in Canadaapi-26315128No ratings yet

- Credit Process Leaflet v2Document2 pagesCredit Process Leaflet v2Shann KerrNo ratings yet

- Financial Report 2010Document125 pagesFinancial Report 2010Hải TạNo ratings yet

- Islamic FinanceDocument5 pagesIslamic Financeahsand123No ratings yet

- 20140108-PITEE-Press Release (OTP Is Hiding A Risk of 10bn EUR)Document2 pages20140108-PITEE-Press Release (OTP Is Hiding A Risk of 10bn EUR)pitee2008No ratings yet

- Textile Policy Govt of Maharashtra 2011-2017Document31 pagesTextile Policy Govt of Maharashtra 2011-2017Pradeep AhireNo ratings yet

- Ist Year Cash Book & BRS, RevenueDocument4 pagesIst Year Cash Book & BRS, RevenueiramanwarNo ratings yet

- Market Focus: Use of Derivatives in BrazilDocument20 pagesMarket Focus: Use of Derivatives in Brazildavy1980No ratings yet

- Tracing Missing ShareholdersDocument19 pagesTracing Missing Shareholdersmrpatel121152No ratings yet

- Deutsche For Infogs Page Final 1Document2 pagesDeutsche For Infogs Page Final 1jayNo ratings yet

- Problems CceDocument4 pagesProblems CceajkoywatanabeeexxNo ratings yet

- Indias Top 500 Companies 2018Document502 pagesIndias Top 500 Companies 2018ayush guptaNo ratings yet

- Islamic Economics and The Islamic Sub EconomyDocument18 pagesIslamic Economics and The Islamic Sub EconomyNoerma Madjid Riyadi100% (1)