You might also like

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Database Resource ManagementDocument16 pagesDatabase Resource ManagementArtur100% (56)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Course Registration Case StudyDocument25 pagesCourse Registration Case StudyPalaniappan Naga Elanthirayan100% (2)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Modeling - UMLDocument3 pagesModeling - UMLPalaniappan Naga ElanthirayanNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Course Registration Case StudyDocument25 pagesCourse Registration Case StudyPalaniappan Naga Elanthirayan100% (2)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Chap 006Document37 pagesChap 006Palaniappan Naga ElanthirayanNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Enterprise Architecture Overview: Military Health SystemDocument6 pagesEnterprise Architecture Overview: Military Health SystemPalaniappan Naga ElanthirayanNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Flipkart CategoriesDocument15 pagesFlipkart Categoriesramanjaneya reddyNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Water: Use of Decision Tables To Simulate Management in SWAT+Document10 pagesWater: Use of Decision Tables To Simulate Management in SWAT+Hugo Lenin SanchezNo ratings yet

- DVR User Manual: For H.264 4/8/16-Channel Digital Video Recorder All Rights ReservedDocument73 pagesDVR User Manual: For H.264 4/8/16-Channel Digital Video Recorder All Rights ReservedchnkhrmnNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- A Business Case For SAP GIS IntegrationDocument7 pagesA Business Case For SAP GIS IntegrationCharles AshmanNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- FAA Safety Briefing Nov-Dec 2017 PDFDocument36 pagesFAA Safety Briefing Nov-Dec 2017 PDFAllison JacobsonNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- HiFi ROSEDocument1 pageHiFi ROSEjesusrhNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Electrical and Electronic EngineeringDocument34 pagesElectrical and Electronic EngineeringANo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Gri 418 Customer Privacy 2016 PDFDocument9 pagesGri 418 Customer Privacy 2016 PDFsharmilaNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Impulse Impedance and Effective Area of Grounding Grids: IEEE Transactions On Power Delivery June 2020Document11 pagesImpulse Impedance and Effective Area of Grounding Grids: IEEE Transactions On Power Delivery June 2020DejanNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Hamidavi Et Al 2020 - Towards Intelligent Structural Design of Buildings ADocument15 pagesHamidavi Et Al 2020 - Towards Intelligent Structural Design of Buildings ARober Waldir Quispe UlloaNo ratings yet

- Full Karding Tut 2020Document3 pagesFull Karding Tut 2020Hillson David100% (1)

- Report On Mango Cultivation ProjectDocument40 pagesReport On Mango Cultivation Projectkmilind007100% (1)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Symbol Master Multi-Pass Symbolic Disassembler Manual V2.0 (Feb 2 1986)Document68 pagesSymbol Master Multi-Pass Symbolic Disassembler Manual V2.0 (Feb 2 1986)weirdocolectorNo ratings yet

- Tommy Molina ResumeDocument2 pagesTommy Molina Resumeapi-266666163No ratings yet

- Controller, Asst - Controller, SR - Accountant, Accounting ManagerDocument3 pagesController, Asst - Controller, SR - Accountant, Accounting Managerapi-72678201No ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Class 8 Art BookDocument17 pagesClass 8 Art BookSrijanNo ratings yet

- Threat Analysis ReportDocument18 pagesThreat Analysis Reporttodo nothingNo ratings yet

- Slides Agile Impacting ChangeDocument20 pagesSlides Agile Impacting ChangeJayaraman Ramdas100% (1)

- SAC Training 01Document11 pagesSAC Training 01Harshal RathodNo ratings yet

- MIS AssignmentDocument3 pagesMIS Assignmentsparepaper7455No ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Equity Sentry ManualDocument3 pagesEquity Sentry ManualSheBrowniesNo ratings yet

- A New Method For Encryption Using Fuzzy Set TheoryDocument7 pagesA New Method For Encryption Using Fuzzy Set TheoryAgus S'toNo ratings yet

- CIS201 Chapter 1 Test Review: Indicate Whether The Statement Is True or FalseDocument5 pagesCIS201 Chapter 1 Test Review: Indicate Whether The Statement Is True or FalseBrian GeneralNo ratings yet

- Python BasicsDocument43 pagesPython BasicsbokbokreonalNo ratings yet

- Bharat Heavy Elelctricals Limited: Operation & Maintenance Manual of Bhelscan Flame Scanner System (Bn10)Document25 pagesBharat Heavy Elelctricals Limited: Operation & Maintenance Manual of Bhelscan Flame Scanner System (Bn10)MukeshKrNo ratings yet

- Pharmaceutical Distribution Management System - ERDiagramDocument1 pagePharmaceutical Distribution Management System - ERDiagram1000 ProjectsNo ratings yet

- Notebook Power System Introduction TroubleshootingDocument44 pagesNotebook Power System Introduction TroubleshootingDhruv Gonawala89% (9)

- "C:/Users/user1/Desktop/Practice" "C:/Users/user1/Desktop/Practice/HR - Comma - Sep - CSV" ','Document1 page"C:/Users/user1/Desktop/Practice" "C:/Users/user1/Desktop/Practice/HR - Comma - Sep - CSV" ','ShubhamJainNo ratings yet

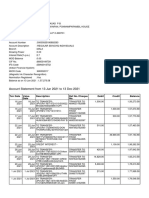

- Account Statement From 13 Jun 2021 To 13 Dec 2021Document10 pagesAccount Statement From 13 Jun 2021 To 13 Dec 2021Syamprasad P BNo ratings yet

- DigiTech GNX 2 Service ManualDocument12 pagesDigiTech GNX 2 Service ManualTOTOK ZULIANTONo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)