You might also like

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Chapter 19 Homework SolutionDocument3 pagesChapter 19 Homework SolutionJack100% (1)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Sixteen Thirty Fund's 2022 Tax FormsDocument101 pagesSixteen Thirty Fund's 2022 Tax FormsJoeSchoffstallNo ratings yet

- Status Report Example 021606110036 Status Report-ExampleDocument5 pagesStatus Report Example 021606110036 Status Report-ExampleAhmed Mohamed Khattab100% (2)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Chapter 17 With NotesDocument42 pagesChapter 17 With NotesJack100% (1)

- Types of EntrepreneursDocument32 pagesTypes of EntrepreneursabbsheyNo ratings yet

- Chapter 21 HomeworkDocument5 pagesChapter 21 HomeworkJack100% (1)

- Tax 2 - Midterm ExamDocument2 pagesTax 2 - Midterm ExamMichelle MatubisNo ratings yet

- Annotated BibliographyDocument9 pagesAnnotated Bibliographyapi-309971310100% (2)

- Final Exam Macroeconomics Sep 10 2021 (Sumeet Madwaikar)Document10 pagesFinal Exam Macroeconomics Sep 10 2021 (Sumeet Madwaikar)Sumeet MadwaikarNo ratings yet

- Briefcase On Company Law Briefcase SeriesDocument180 pagesBriefcase On Company Law Briefcase SeriesAminath ShahulaNo ratings yet

- Portfolio Management 1Document28 pagesPortfolio Management 1Sattar Md AbdusNo ratings yet

- Chap 21-1Document15 pagesChap 21-1JackNo ratings yet

- Chap+21+corrected SlideDocument1 pageChap+21+corrected SlideJackNo ratings yet

- Chap 21-2Document8 pagesChap 21-2JackNo ratings yet

- Chap020 1Document16 pagesChap020 1JackNo ratings yet

- IPPTChap 019Document11 pagesIPPTChap 019JackNo ratings yet

- Chap 020Document15 pagesChap 020JackNo ratings yet

- Chapter 20 Homework SolutionDocument6 pagesChapter 20 Homework SolutionJackNo ratings yet

- Chap 020Document15 pagesChap 020JackNo ratings yet

- Updated NotesDocument3 pagesUpdated NotesJackNo ratings yet

- Chapter 20 Homework SolutionDocument6 pagesChapter 20 Homework SolutionJackNo ratings yet

- CH+19 2Document9 pagesCH+19 2JackNo ratings yet

- Chapter 18 Class NotesDocument9 pagesChapter 18 Class NotesJackNo ratings yet

- Chapter 18 Homework SolutionsDocument4 pagesChapter 18 Homework SolutionsJack100% (1)

- Chap 18Document41 pagesChap 18JackNo ratings yet

- Chapter 10 Homework SolutionsDocument6 pagesChapter 10 Homework SolutionsJackNo ratings yet

- CH19 3Document9 pagesCH19 3JackNo ratings yet

- Solution+ Quarterly+tax+paymentDocument1 pageSolution+ Quarterly+tax+paymentJackNo ratings yet

- Chapter 17 Homework SolutionsDocument4 pagesChapter 17 Homework SolutionsJackNo ratings yet

- Chapter 17 Homework SolutionsDocument4 pagesChapter 17 Homework SolutionsJackNo ratings yet

- Chapter+15+ Compatibility+ModeDocument29 pagesChapter+15+ Compatibility+ModeJackNo ratings yet

- Chapter 10 - With NotesDocument47 pagesChapter 10 - With NotesJackNo ratings yet

- Chapter 16 Homework SolutionsDocument6 pagesChapter 16 Homework SolutionsJackNo ratings yet

- Chapter 15 Homework SolutionsDocument2 pagesChapter 15 Homework SolutionsJackNo ratings yet

- Chapter+15+ Compatibility+ModeDocument29 pagesChapter+15+ Compatibility+ModeJackNo ratings yet

- Chapter 10Document6 pagesChapter 10JackNo ratings yet

- Depreciation Information SheetDocument4 pagesDepreciation Information SheetJackNo ratings yet

- Pt. Bank Rakyat Indonesia (Persero) Tbk. Banjar Branch (F.0162)Document2 pagesPt. Bank Rakyat Indonesia (Persero) Tbk. Banjar Branch (F.0162)LaiLi ImnidaNo ratings yet

- Dissertation Ulrich BobeDocument5 pagesDissertation Ulrich BobeBuyPapersForCollegeOnlineCanada100% (1)

- Ex 6 Duo - 2021 Open-Macroeconomics Basic Concepts: Part 1: Multple ChoicesDocument6 pagesEx 6 Duo - 2021 Open-Macroeconomics Basic Concepts: Part 1: Multple ChoicesTuyền Lý Thị LamNo ratings yet

- Lesson 2 Material Adidas To Make Shoes From Ocean GarbageDocument3 pagesLesson 2 Material Adidas To Make Shoes From Ocean GarbageashykynNo ratings yet

- Critique Paper BA211 12 NN HRM - DacumosDocument2 pagesCritique Paper BA211 12 NN HRM - DacumosCherBear A. DacumosNo ratings yet

- Chapter One - Part 1Document21 pagesChapter One - Part 1ephremNo ratings yet

- Signature Global Park 5 Apartment Details and Payment PlansDocument2 pagesSignature Global Park 5 Apartment Details and Payment Planssanyam ralliNo ratings yet

- 10th March: by Dr. Gaurav GargDocument2 pages10th March: by Dr. Gaurav GarganupamNo ratings yet

- Economics Syllabus NEPDocument59 pagesEconomics Syllabus NEPsaklainpasha76No ratings yet

- Directory of Cao 01042018Document154 pagesDirectory of Cao 01042018Shyam SNo ratings yet

- Chaotics KotlerDocument5 pagesChaotics KotlerAlina MarcuNo ratings yet

- Preparing The Philippines For The 4th Industrial Revo PIDS Report 2017-2018Document120 pagesPreparing The Philippines For The 4th Industrial Revo PIDS Report 2017-2018Rico EstarasNo ratings yet

- Solow Growth ModelDocument15 pagesSolow Growth ModelSamuel Elias KayamoNo ratings yet

- High Capacity Stacker-F1-G1-H1 Safety Guide en - USDocument14 pagesHigh Capacity Stacker-F1-G1-H1 Safety Guide en - UShenry lopezNo ratings yet

- K&N Case Group - 3Document41 pagesK&N Case Group - 3priya_pritika6561100% (1)

- Radical Culture Research Collective - Nicolas BourriaudDocument3 pagesRadical Culture Research Collective - Nicolas BourriaudGwyddion FlintNo ratings yet

- Use The Following Information in Answering Questions 130 and 131Document1 pageUse The Following Information in Answering Questions 130 and 131Joanne FernandezNo ratings yet

- Aqa Econ2 QP Jan13Document16 pagesAqa Econ2 QP Jan13api-247036342No ratings yet

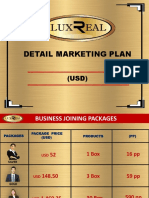

- Luxreal Detail Marketing Plan (2019) UsdDocument32 pagesLuxreal Detail Marketing Plan (2019) UsdTawanda Tirivangani100% (2)

- Economic Impact of Accelerating Permit Local Development and Govt RevenuesDocument6 pagesEconomic Impact of Accelerating Permit Local Development and Govt RevenuesQQuestorNo ratings yet

- Data Link Institute of Business and TechnologyDocument6 pagesData Link Institute of Business and TechnologySonal AgarwalNo ratings yet

- Perfect Substitutes and Perfect ComplementsDocument2 pagesPerfect Substitutes and Perfect ComplementsVijayalaxmi DhakaNo ratings yet